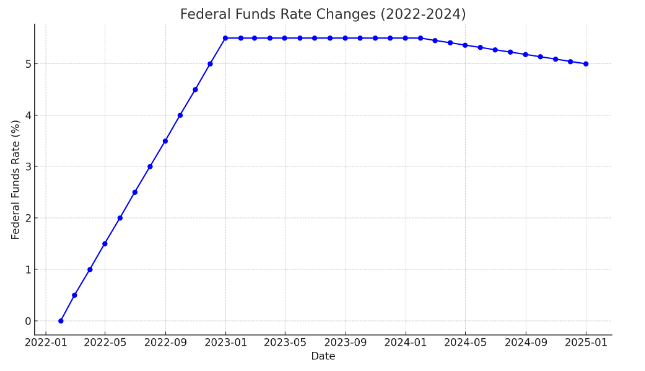

In a necessary go that impacts each equally the housing market place and property private mortgage institutions like Evergreen House Financial loans, the Federal Open Markets Committee (FOMC) has introduced the upkeep of its brief-term protection curiosity value involving 5.25% and 5.5%. This closing choice, declared on Wednesday, marks the fourth time in 2023 that the FOMC has paused value hikes, subsequent 11 raises as a result of March 2022.

Federal Reserve Chairman Jerome Powell, addressing the current financial native local weather, indicated an expectation of some 25 basis stage reductions in prices all via 2024. This strategic change indicators the cease of price hikes and a brand new interval in financial protection, doubtlessly bolstering expenditure confidence.

Responding to this improvement, the bond market place noticed a drop in the 10-calendar 12 months Treasury produce to 4.%, a decrease as a result of late July. Specialists, together with Mike Fratantoni from the Mortgage Bankers Association, interpret this as an cease to conversations about extra degree hikes, concentrating in its place on the speed discount tempo. This is anticipated to positively have an effect on housing and home mortgage marketplaces, doubtlessly main to reduce mortgage expenses and spurring modest development in residence product gross sales for 2024.

Evergreen Residence Loans, a crucial participant in the home mortgage sector, has been intently monitoring these developments. “The Fed’s conclusion aligns with our anticipations and bodes completely for homebuyers and the all spherical housing market place,” states a spokesperson from Evergreen Property Financial loans. “We foresee an uptick in house finance mortgage routines, together with refinancing, as charges flip into rather more favorable.”

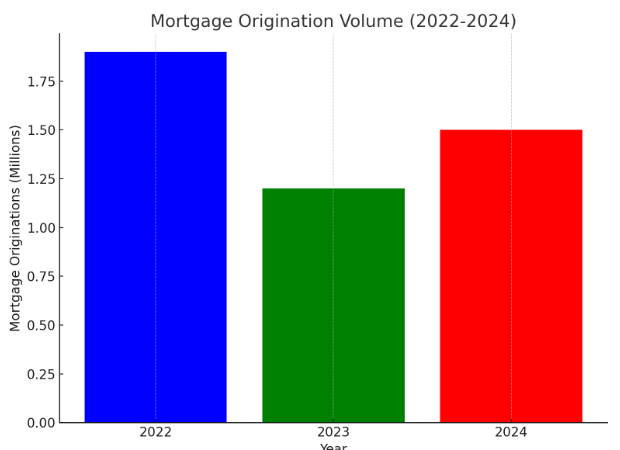

All over 2023, the Fed’s price hikes impacted a number of sectors, with the mortgage mortgage discipline staying notably impacted. TransUnion tales a 37% yr-over-calendar 12 months decrease in home mortgage originations. Evergreen Residence Loans, nonetheless, has navigated these difficulties by concentrating on customer-centric choices and anticipates a additional favorable atmosphere in 2024.

Selma Hepp, chief economist at CoreLogic, notes that even with a strong November positions report, indications of economic cooling are obvious. This options slower place development and modest rises in unemployment charges, hinting at a extra restrained financial outlook for the up coming calendar 12 months.

Searching in advance, the anticipation of value cuts in 2024 delivers a optimistic outlook. The Key House mortgage Market Study index by Freddie Mac, which stood simply greater than 7% not way back, is predicted to say no additional extra, providing aid to fee-sensitive homebuyers.

Evergreen Residence Financial loans echoes the sentiment of Realtor.com Chief Economist Danielle Hale, anticipating mortgage mortgage charges to fall to throughout 6.5% by calendar year-close 2024. This cut back would tremendously profit individuals with current large-charge mortgages, opening up potentialities for refinancing and higher affordability.

Michele Raneri, VP of U.S. analysis and consulting at TransUnion, highlights the potential value financial savings for homeowners with a degree fall to five.5%. This may counsel sizeable month to month value financial savings, liberating up property in a excessive price-of-residing environment.

In abstract, the Fed’s regular strategy and long run price cuts are discovered as a constructive improvement by Evergreen Household Financial loans and different sector avid gamers, paving the way in which for a much more vibrant housing market place in 2024.

Supply: HousingWire