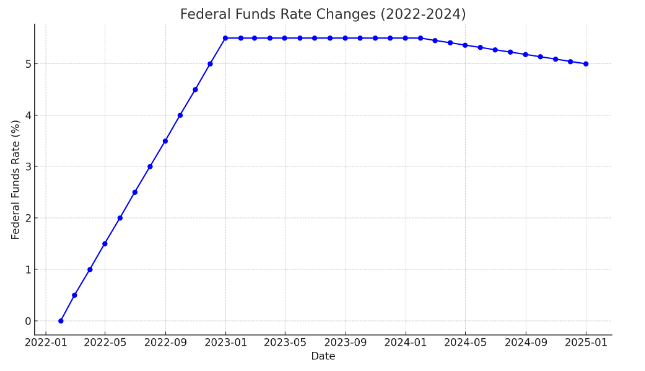

The Federal Reserve Wednesday permitted a 50 basis place enhance to its coverage fascination level in an work to cut back inflation, along side a plan to shrink its $9 trillion asset portfolio starting up coming thirty day interval, in accordance to Chairman Jerome Powell.

Through a information assembly subsequent the Fed’s committee meeting, Powell launched the enhance and outlined the Fed’s plan to begin “the method of appreciably minimizing the measurement of our stability sheet,” he talked about.

“It is important that we offer inflation down if we’re to have a sustained interval of strong labor present market issues that profit all,” Powell mentioned. “The latest {photograph} is obvious to see: The labor sector is extraordinarily restricted and inflation is way manner too massive. Against this backdrop, at the moment the FOMC elevated its plan curiosity price by a 50 percent share situation and anticipates that ongoing will increase within the concentrate on value for the federal sources fee shall be appropriate.”

Authorities say Wednesday’s go wasn’t a shock.

“This modify had been telegraphed clearly in new speeches,” claimed Mike Fratantoni, principal economist for the Mortgage Bankers Association. In the course of the announcement, Fratantoni additionally designed observe of Powell’s warning that the committee “anticipates that ongoing will enhance within the concentrate on selection shall be applicable.”

“In different phrases and phrases, we’re considerably from carried out at this position,” claimed Fratantoni. “MBA forecasts that the Fed money concentrate on will attain 2.5%, the impartial cost, by the end of 2022.”

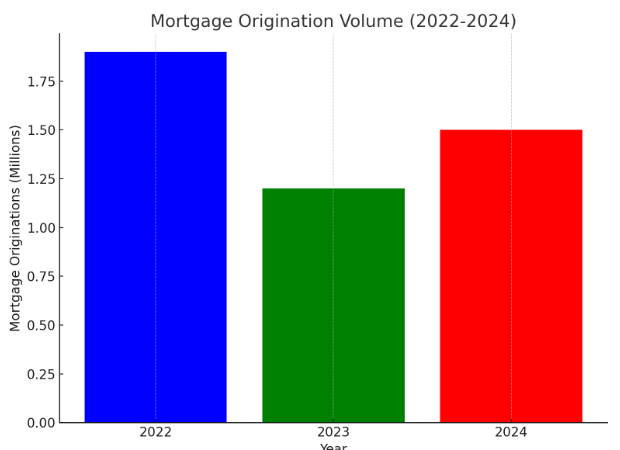

(*50*) the the most recent price hike from the Federal Reserve, the continuing warfare in Ukraine and ongoing financial restoration pursuing the pandemic, mortgage mortgage lenders throughout the state are taking care of a unstable housing market. Understand how updating your own home finance mortgage know-how stack can help you get prematurely in at present’s unpredictable lending environment

Introduced by: Polly

As data of the Fed’s closing resolution circulated, the S&P 500, Dow and Nasdaq all rose and extended positive factors when Realtors, private mortgage officers, property finance mortgage brokers and different subject business specialists deemed the quick ramifications on the housing sector.

Danielle Hale, chief economist for Realtor.com, talked about the 2 go hand in hand.

“Mortgage charges are an very important channel by means of which Fed coverage has an impact on the true economic system. In different textual content, the Fed’s selections impact household budgets, steadiness sheets, and expending choices by means of their results on interest charges like residence finance mortgage premiums. With residence finance mortgage premiums climbing, up 2 share elements previously 4 months, the financial circumstances dealing with residence shoppers have shifted in a important manner,” Hale outlined.

She additionally noticed inflation is “working on the highest fee in 40-as nicely as yrs, placing it at a life span excessive for most millennials and younger generations.” But, she concluded, Wednesday’s “vote by itself will not be more likely to spark a new surge in home mortgage charges.”

Fratantoni defined MBA expects home mortgage charges will plateau in shut proximity to present ranges.

“The monetary markets have tried to price within the impression of Fed actions over this cycle, and they’re doubtless additionally pricing within the monetary slowdown that will consequence,” Fratantoni acknowledged. “Once we’re earlier this value spike and concerned volatility, MBA expects that alternative homebuyers might be way more keen to re-enter {the marketplace}. Provided how a nice deal elevated charges will carry on being greater than the sooner 20 years, we don’t expect refinance want to extend any time shortly.”

Despite delivering higher-stage, nuanced particulars on the Fed’s strategy, Powell first made distinct the announcement wasn’t geared toward such sector specialists. He began his sort out by indicating he wished to converse proper to the American group.

“Inflation is way as nicely substantial. We perceive the hardship it’s resulting in and we’re shifting expeditiously to offer it again once more down,” Powell talked about all via the information conference. “We have equally the instruments we have to have and the clear up that it is going to purchase to revive worth stability on behalf of American households and enterprises.”

“Our overarching goal is using our sources to ship inflation once more all the way down to our 2% purpose. With regard to our stability sheet, we additionally issued our exact designs for chopping down our securities holdings. Dependable with the ideas we issued in January, we intend to drastically decrease the scale of our equilibrium sheet greater than time in a predictable technique,” Powell acknowledged. “We’ll be prepared to control any of the main points of our technique in gentle of financial and cash developments.”

Powell defined “after increasing at a sturdy 5.5% tempo final yr, over-all financial motion edged down within the very first quarter.” But, he reported the labor market has ongoing to strengthen, inspite of inflation remaining “nicely earlier talked about our lengthier function purpose of 2%.”

“In March the unemployment quantity strike a write-up-pandemic and in shut proximity to-five-10 years very low of 3.6%,” Powell reported, touting the nation’s improvement.

After speaking about how Russia’s invasion of Ukraine is influencing world large problems, Powell defined: “Our job is to take a look at the implications for the U.S. monetary state — which proceed to be very not sure.”

The ongoing invasion is anticipated to restrain financial exercise overseas and can proceed to have an impact on the worldwide provide chain, he mentioned.

“Our coverage has been adapting and it’ll proceed to take action,” Powell reported.

Supplemental 50 bps will enhance “must be on the desk on the subsequent pair of conferences,” he claimed.

Powell additionally outlined “the financial system usually evolves in sudden strategies,” and famous that inflation has “clearly shocked” some all via the sooner yr. Powell then warned, “additional surprises might be in retailer.”

But that does not necessarily mean all of the issues is unpredictable.

Skylar Olsen, the principal economist at Tomo, additionally claimed the switch was “already anticipated by the present market, however (it was) nonetheless the key enhance in a few years. The coming week will carry with it interest cost volatility, however early indicators of {the marketplace} response have charges slipping, not capturing up,” she talked about.

No matter, Powell mentioned the Fed’s focus stays the have an effect on that this kind of choices have on frequent Individuals.

“We subsequently will wish to be nimble … and we’ll try to forestall introducing uncertainty to what’s beforehand an an terribly tough and unsure time,” he reported.

“The Fed’s financial protection actions are guided by our mandate to promote highest employment and safe prices for the American people,” Powell claimed. “We acknowledge that our actions impact communities, households and companies throughout the nation. Anything we do is in help to our group mission. We on the Fed will do every thing we are able to to achieve our optimum work and worth steadiness goals.”

HousingWire Direct Analyst Logan Mohtashami extra outlined what the fascination level hike may suggest for residence finance mortgage costs. “The Fed lifted prices and talked about bringing inflation down, and after the press convention, bond yields fell. Why? I think about that a lot of Fed value hikes have been priced, getting the 10-yr produce in direction of 3.%. If bond yields maintain rising we have now further space to get in direction of 6.% on mortgage premiums. Even so, if financial data fades and yields are coming down, residence finance mortgage prices will go down with it.

“Right now, we’re in a tug of warfare regarding two camps. An individual group thinks that the Fed cannot enhance charges that considerably primarily as a result of it is going to result in a financial downturn, and an extra group thinks the Fed wishes to develop a recession to wrestle inflation,” Mohtashami mentioned.

“Since Europe’s financial system is slowing down, China’s financial system is in a mess, Japan wants further tourism nonetheless, and Russia is in a financial downturn, there are restrictions to how significantly further worldwide bond yields can head elevated and our yields and home mortgage charges. We should select the monetary data only one 7 days at a time as a result of truth we do see some cracks within the inflation details and improvement.

“However, the Russian invasion of Ukraine and China’s lockdown have put pressure on inflation data. It goes to be an epic tug of warfare for the comfort of the calendar yr. For now, the 10-yr generate has held across the 3.% diploma with out the necessity of a breakout. The peak generate on the 10-yr produce was 3.25% in 2018 when mortgage mortgage charges purchased to five.% again then. Charges are actually elevated nowadays because the mortgage mortgage cost pricing is even worse.”

This story was present with enterprise response proper after authentic publication.