Written on 23 October 2024 by Ray Boulger

The FCA is asking for views by thirty first October on how to refine its retail conduct guidelines, with out decreasing help and safety for customers. It particularly says it desires to simplify its retail conduct guidelines and “tackle potential areas of complexity, duplication, confusion, or over-prescription, which create regulatory prices with restricted or no shopper profit.”

In respect of the mortgage market my principal suggestion could be to abolish the requirement to quote an APRC, or every other type of APR.

An APR is useful in evaluating the price of some sorts of borrowing, comparable to unsecured loans, the place the rate of interest is often mounted for time period and any charges are recognized up entrance. However, for mortgages, besides maybe for mounted for life mortgages, together with Lifetime Mortgages, the APRC is just not solely not useful, however positively deceptive.

One technical consequence of the APRC being deceptive is that it renders all ESIS and mortgage presents non-compliant because the FCA requires all communications to be “truthful, clear and never deceptive.”!

The primary downside with the APRC after all is that’s makes assumptions which everybody, together with the regulator, is aware of will likely be flawed. If debtors typically merely reverted to a lender’s SVR for the rest of the time period after an preliminary deal the APR might be a helpful approach of highlighting a excessive revert to fee.

In the true world even the small proportion of debtors who haven’t traditionally chosen a product switch or remortgage on the finish of their preliminary deal (or to transfer house) is probably going to be even smaller in a Consumer Duty world, the place lenders have a regulatory requirement to ship good outcomes for retail prospects at each stage of the client journey.

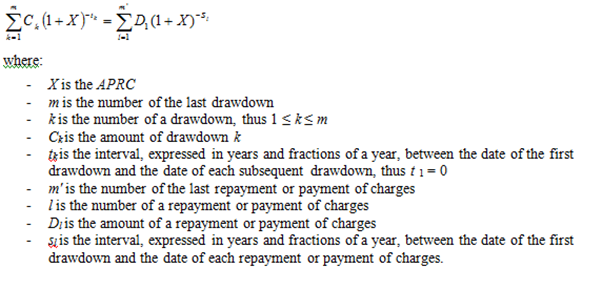

Despite the APRC changing into a compulsory requirement over 8 years in the past I counsel that few mortgage market contributors, not to mention debtors, might clarify precisely how it’s calculated. However, MCOB helpfully gives an equation to calculate the APRC, which for the good thing about any nerds studying that is as follows:

So, it’s good to know that’s clear, though I have to confess my information of algebra is relatively much less now than once I left faculty!

Even if one believes APRCs have some worth the premise of calculation has different defects as well as to the rate of interest assumptions. For instance, while prices are rightly factored into the calculation cashbacks are ignored, as are refunds of any charges. Why?

In June 2023 the FCA mentioned in an announcement that “we think about that, basically, an APRC calculated on incorrect assumptions is unlikely by itself to deprive debtors of the flexibility to make knowledgeable decisions.”

I fully concur with this sensible evaluation by the FCA. Advisers usually want to clarify to purchasers that though the FCA requires an APRC to be acknowledged it’s deceptive and might be ignored until the borrower intends retaining the identical mortgage till maturity. The want for such a proof doesn’t improve the FCA’s repute in shopper eyes!

The APRC was launched, changing the APR, on account of the EU Mortgage Credit Directive. Now we’ve got left the EU and mortgage laws might be designed to go well with simply the UK, the APRC, or any by-product of it, needs to be consigned to regulatory historical past.

Consumers will profit by not risking being misled by an irrelevant determine; advisers will profit by having the ability to focus their recommendation on what actually issues, relying on particular person purchasers’ necessities and preferences; and lenders will profit by not needing to produce meaningless figures.

As a big majority of debtors select one other deal when their preliminary mortgage deal ends, and almost all have the choice to, the FCA might mandate an alternate to the APRC primarily based on the speed and time period of the preliminary fee (assuming no fee adjustments if a tracker fee), plus recognized charges and factoring in the good thing about any cashbacks and/or price refunds.

Category:Ray Boulger