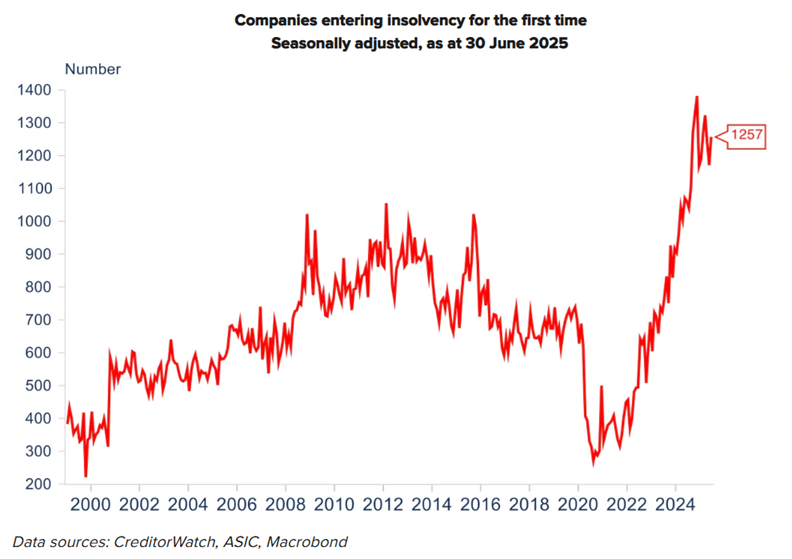

Data from the Australian Securities and Investments Commission (ASIC) for June confirmed insolvencies holding at ranges about 10% beneath the highs seen in November 2024. CreditorWatch attributed the stabilisation to a number of elements, together with mid-2024 revenue tax cuts, authorities cost-of-living assist, a steadier price of recent corporations with tax defaults, and slower value development in latest months.

The Reserve Bank of Australia’s first rate of interest minimize this yr could also be beginning to have an impact, although CreditorWatch famous it’s too quickly for the May discount to have a big influence. A broadly anticipated price minimize in July didn’t materialise, however one other discount is anticipated in August after higher-than-expected unemployment knowledge for June.

“The decline in CreditorWatch trade payment defaults is a promising sign that enterprise money move pressures could also be easing, however with insolvencies nonetheless working 33% above FY24 ranges, and significantly elevated in hospitality and development, I’m not getting too excited simply but,” stated Patrick Coghlan (pictured), chief government officer at CreditorWatch.

“The sharp rise in closures throughout sectors historically seen as extra steady – like healthcare and schooling – underlines the breadth of the financial pressure. We’ll proceed to observe for early indicators of sustained restoration, however the subsequent six months will likely be vital for figuring out whether or not insolvency charges start to fall or stay stubbornly excessive.”