What do you are feeling of whenever you picture a critical property investor? Is it a Donald Trump type in a snazzy match sitting down vital up in an ivory tower?

You couldn’t acknowledge it, however any particular person who owns a home is technically a precise property investor—which suggests the title is up for grabs for almost anyone. You mainly have to understand how to get began off.

Investing in precise property doesn’t have to be actually onerous, and it doesn’t have to be worrying. There are a number of paths to developing prosperity through actual property. You can simply occupy your key residence very lengthy expression and examine it respect as you go concerning the routines of every day residing.

You also can receive numerous solitary-spouse and kids households that ship earnings motion by means of passive earnings. There are extra techniques that entail fixing up properties and offering them promptly, as correctly as getting houses with a prolonged-time interval funding outlook in thoughts.

In any circumstance, real property provides the possible to improve your net nicely price. And this model of prosperity may be handed on (as can the qualities) for generations to seem.

So let’s leap into how to set up prosperity with critical property.

Property Appreciation

One explicit of one of the best strategies to set up wealth on account of precise property is thru residence appreciation. In areas with superior improvement doable, the value of solitary-household properties that you just make investments in can elevate round time. Of examine course, completely nothing is a assured wager, so it’s important to perform in depth examine and thanks diligence to uncover neighborhoods poised for growth.

A real property agent can help you with this. If achievable, it on no account hurts to speak to yet another genuine property dealer or certified in home administration who might maybe be acquainted with the ins and outs of genuine property and with your wanted neighborhood(s) as completely.

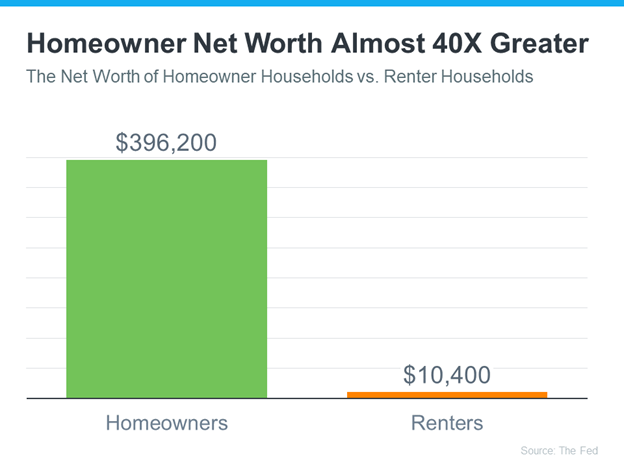

Property appreciation is a wonderful method to construct wealth, regardless of whether or not you merely very personal the house you reside in or commit in quite a few one-household homes.

The vital to utilizing fringe of home appreciation is information that investing in critical property is often a long-time interval endeavor. That’s since, like nearly the whole lot else, the solitary-spouse and kids residence sector may be cyclical with quite a few ups and downs. But these who keep in it for the extended run typically expertise the rewards of a efficient real property funding determination on the time they’re ready to market.

Rental Profits

Acquiring many solitary-loved ones houses—both suddenly or one explicit at a time—permits a critical property investor to make rental earnings from tenants.

This approach can quickly amass a daily and sometimes appreciable stream of passive money move that not solely covers the properties’ mortgage mortgage funds and property administration and maintenance prices but in addition strains the precise property investor’s pocket with {dollars}. This is a earn-gain, as a predictable earnings move can do double obligation, sustaining the genuine property portfolio whereas elevating the online really price of the real property dealer.

Leverage

Leverage is a extremely efficient machine for a precise property dealer looking to maximize their returns and wealth accumulation.

Keeping residence loans on rental attributes permits a genuine property investor to deal with a property’s whole profit with solely a portion of the funding determination. This normally means your returns (earnings) may be amplified primarily as a result of any appreciation within the rental properties’ profit is calculated based mostly on their complete really price, not simply your preliminary monetary funding (down fee and the month-to-month funds you’ve now made).

Leverage goes every methods, although, so in case your property goes down in profit, you might be on the hook for rather more than it’s nicely price. Which is why it’s crucial to do your thanks diligence and mitigate pitfalls affiliated with market place fluctuations.

Tax Advantages

This is often an missed perk for a would-be genuine property dealer who’s simply beginning up to grasp about how to make prosperity with actual property. The fascination on mortgage mortgage funds, home taxes, and chosen residence administration bills may be tax deductible. Any tax reward can positively affect your return on funding determination (ROI) and, consequently, your web really price.

Flipping Houses

Dwelling in your principal residence prolonged time period and watching it have the benefit of in value is an effective number of monetary dedication, as is acquiring one-family homes as rental properties and amassing lease checks. That is passive money move.

For the extra energetic critical property dealer, there’s the strategy of flipping houses.

Currently being a flipper entails buying properties which may be discounted due to to the previous proprietor’s financial constraints or deferred maintenance. A real property investor can then renovate/restore these properties and market (flip) them for a revenue.

Flipping isn’t a sure purchase, nonetheless. It requires a deep comprehending of the intense property sector, as well as to home building and enterprise administration. Markets can flip, and expenses can fluctuate. That doesn’t essentially imply you simply can’t construct wealth by flipping, however it might get some legwork and, in quite a few cases, some expertise.

Acquire and Hold

On the flip side (no pun meant), embracing a get-and-maintain system permits a genuine property dealer to capitalize on the prolonged-phrase appreciation of rental qualities.

Buyers can revenue from equally property appreciation and rental income by getting single-relatives homes or different rental attributes and protecting on to them for an extended interval. In extra of time, this will undoubtedly elevate your net price.

You do have to proceed to maintain in mind that these properties could have to have very long-term therapy. This might nicely contain choosing a property administration agency or managing these houses your self, which might swiftly convert right into a entire-time job, based mostly on how numerous qualities you possess.

Authentic Estate Can Convey Lengthy-Time interval Wealth

Creating prosperity on account of actual property can undoubtedly be carried out. In level, it’s carried out every day by traders large and tiny.

There are youthful gurus with an important goal of prosperity accumulation. There are retired {couples} who mainly need to have the benefit of passive money move. And, certainly, there are personal and publicly traded real property funding determination trusts (REITs) that interact within the exercise, additionally.

Nevertheless the measurement and information diploma might fluctuate, these individuals at the moment and companies all by means of the state all have a single goal in mind: prosperity accumulation. And they’ve found a wonderful method to assemble prosperity with genuine property.