Canstar research worth modifications | Australian Broker News

Information

Canstar experiences price modifications

Info reveals shifts in variable and mounted prices

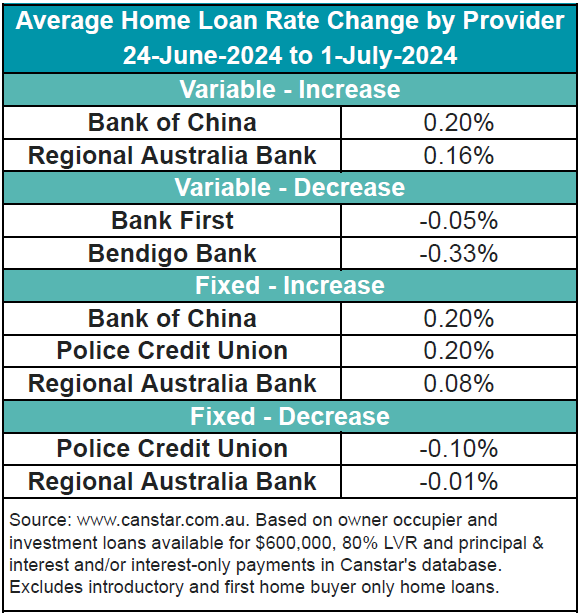

Canstar’s particulars found shifts in each of these variable and mounted costs all through the market place over the sooner week.

Level hikes and cuts

New variations in dwelling monetary mortgage premiums noticed two mortgage suppliers escalating 12 operator-occupier and dealer variable charges by a median of .17%, when 3 lenders raised 66 mounted charges by an regular of .12%.

Conversely, two collectors reduce 11 variable premiums by an abnormal of .10%, and two lenders lessened eight fastened charges by an regular of .08%.

Least costly variable premiums

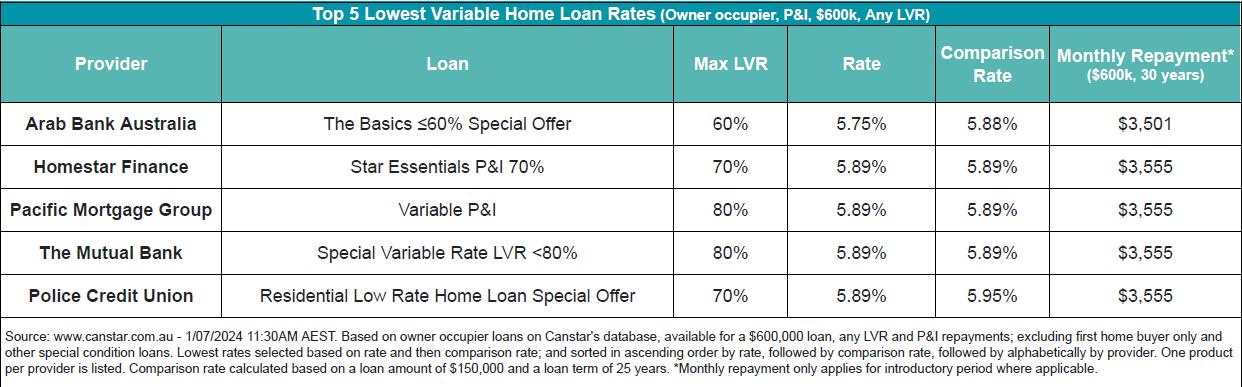

The lowest variable cost for any LVR is 5.75%, provided by Arab Bank Australia. Currently, there are 23 charges down beneath 5.75% in Canstar’s database, a slight lower from former weeks. These charges are obtainable at Australian Mutual Bank, Bank Australia, Horizon Bank, LCU, People’s Choice, Queensland Country Financial establishment, RACQ Lender, The Mac, and Unity Lender.

Financial concerns and predictions

Steve Mickenbecker (pictured earlier talked about), Canstar’s staff authorities for monetary corporations and chief commentator, commented on the the most recent financial indicators and degree actions.

“The enhance of the Might CPI Indicator to 4.1% may have upset the Reserve Financial establishment and debtors alike,” Mickenbecker mentioned. “National Australia Lender has instantly confirmed debtors’ fears and pushed out its expectation for the preliminary need worth slice from November 2024 to May properly upcoming 12 months.”

Borrower points

Mickenbecker acknowledged the fears of debtors battling extended greater charges.

“At least the financial institution is just not chatting up an curiosity cost enhance in 2024, however the very lengthy interval earlier than any need quantity discount will fret beforehand pressured debtors, who’re questioning when and wherever they uncover some pleasure,” he acknowledged.

Mickenbecker inspired debtors to actively discover better prices.

“Eleven months is as properly in depth to attend for a worth slice and any borrower in audio economical situation must be looking for for their very own scale back,” Mickenbecker acknowledged.

Discounts choices

Highlighting probably monetary financial savings, Mickenbecker defined, “Canstar lists 23 monetary loans beneath 5.75%, which is a preserving of round .6% for the standard borrower. A whole lot of debtors have now negotiated a reduce worth with their financial institution, however a second chunk of that cherry is most certainly even now potential even when it signifies shifting banking establishments.”

Favourable information for savers

There is a few good info for savers, with expression deposit premiums at present being lifted by 6 banking corporations for a nutritious widespread enhance of .78 %, Canstar famous.

Get the most well liked and freshest mortgage information despatched correct into your inbox. Subscribe now to our FREE day-to-day publication.

Linked Stories

Preserve up with the latest info and capabilities

Sign up for our mailing itemizing, it’s completely free!