Aussies’ retirement designs proceed being steady | Australian Broker Information

Information

Aussies’ retirement choices proceed to be regular

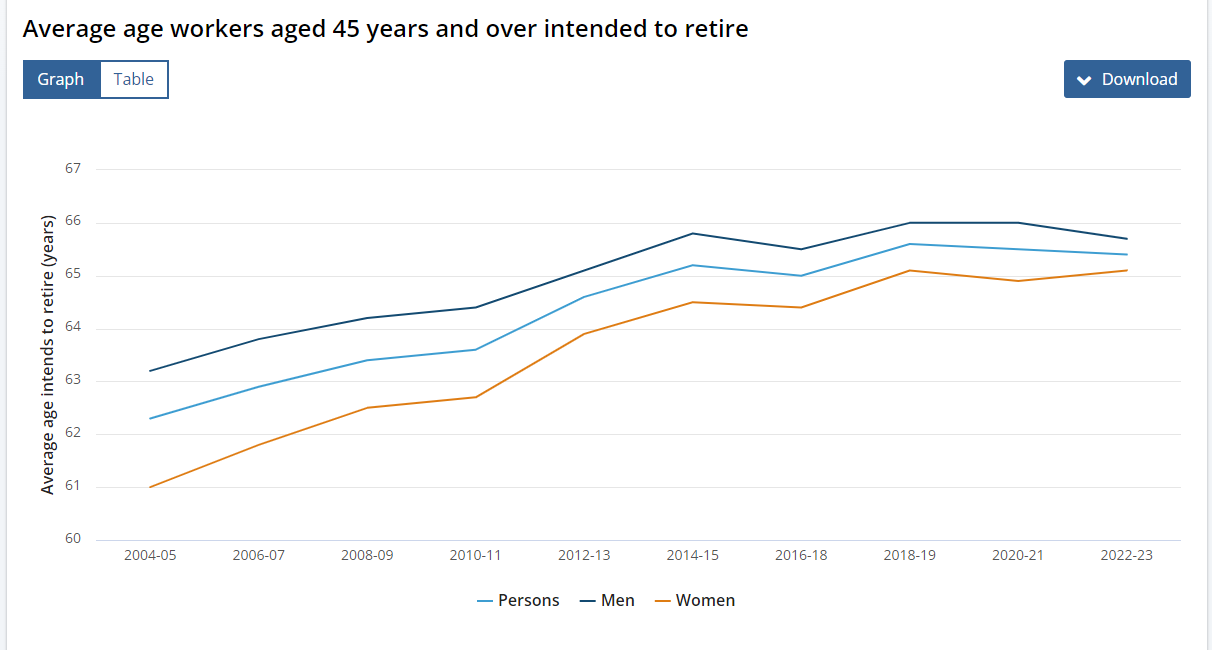

Retirement age proceed to amongst 65-66

Australians are nonetheless meaning to retire in between 65 and 66, in accordance to contemporary new figures from Ab muscle tissue.

“While the typical age that folks as we speak intend to retire has risen above time, it hasn’t adjusted a lot within the earlier 10 a few years,” reported Bjorn Jarvis (pictured above), Ab muscle tissue head of labour research. “This bizarre has been amongst 65 many years and 65.6 a few years for shut to a ten years, contemplating that 2014-15.”

Gender dissimilarities narrowing

Adult males generally tend to retire barely afterward than females, however the gap is closing.

“In 2022-23, there was round 50 % a calendar yr variation amongst guys and girls, in distinction to a yr huge distinction a decade in the past, and a two-calendar yr variance all-around 10 a number of years simply earlier than that.” Jarvis defined in a media launch.

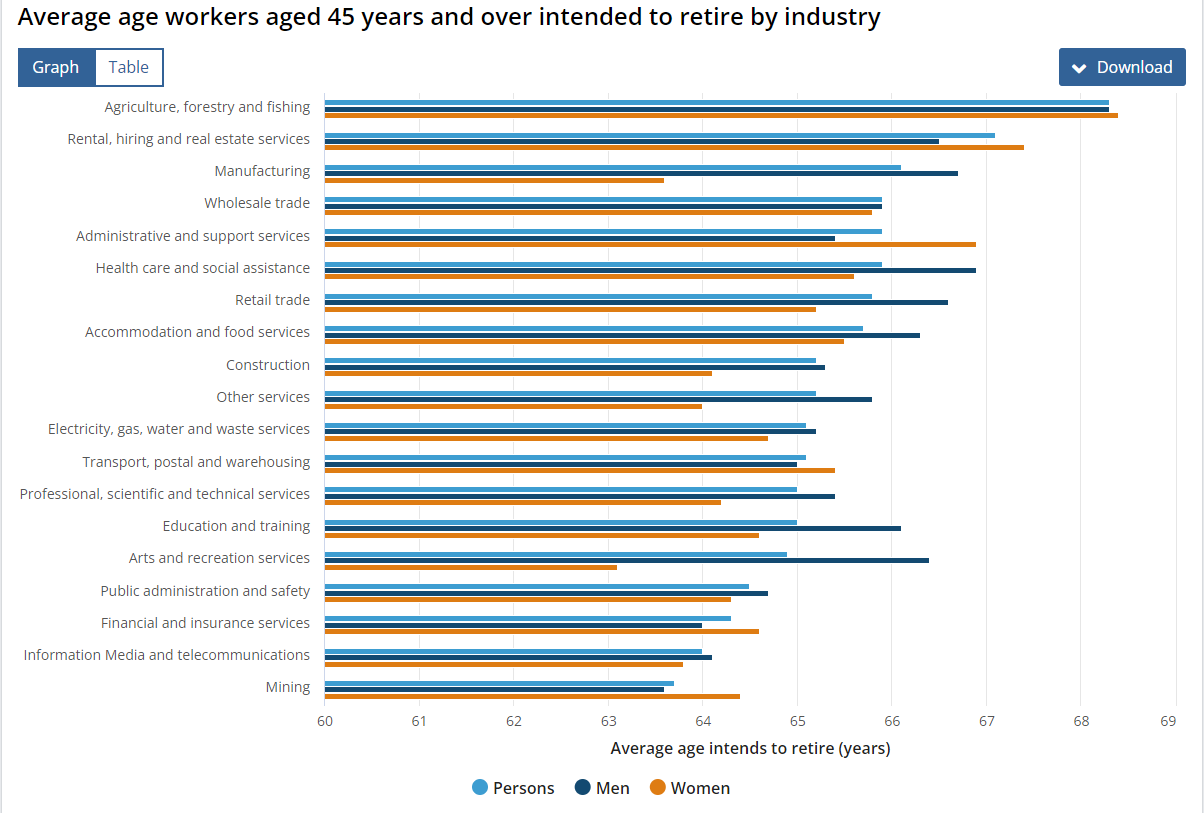

Sector-specific tendencies

Folks in agriculture, forestry, and fishing intend to retire at 68.3 years, the utmost common, despite the fact that people in mining method to retire at 63.7 years, the least costly.

Age at retirement

The Stomach muscle tissue data additionally confirmed the true age when retirees stopped working, with folks retiring afterwards on common.

“In 2022-23, folks as we speak who retired within the earlier 20 many years did so, on typical, at 61.4 yrs,” Jarvis reported. “This common has risen from 58.5 a very long time in 2014-15 and 57.4 a few years in 2004-05.

Retirees from the humanities and recreation services and products enterprise retired afterwards than all these in some other enterprise, at 64.4 a few years. The youngest frequent retirement age was in lodging and meals objects providers, at 58.5 years.

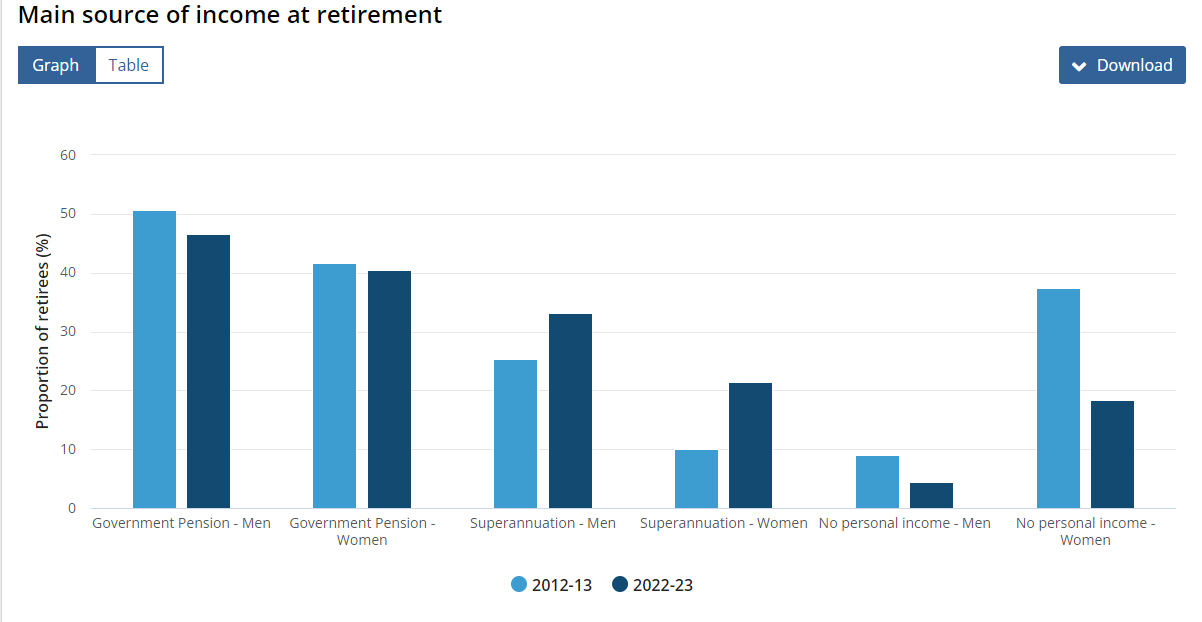

Retirement income sources

Govt pensions carry on being the first income useful resource for 43% of retirees, adopted by superannuation at 27%, Abdominal muscle tissue described.

The amount of individuals as we speak with no non-public money circulation at retirement has fallen from 25% in 2012-13 to 12% in 2022-23.

“In particular person, the share of ladies reporting no particular person money circulation has dropped considerably, down from 37% to 18%,” Jarvis claimed.

“The amount of ladies who relied on their companion’s revenue as their key useful resource of money for assembly residing expenditures at retirement has fallen by excess of 10 share particulars in regards to the 10 years, dropping from 44% in 2012-13 to 31 for every cent in 2022-23.”

Things influencing retirement

Financial security (36%) and particular person well being (22%) are probably the most frequent variables influencing retirement picks. One specific in 8 retirees cited reaching the eligibility age for a pension as a vital issue, Ab muscle tissue claimed.

Get the most effective and freshest mortgage mortgage data shipped supreme into your inbox. Subscribe now to our FREE day-after-day e-newsletter.

Similar Tales

Hold up with the latest data and events

Join our mailing record, it’s cost-free!