Overview – Florida Empowered DPA Plan

The Florida Empowered DPA System is a brand new utility for homebuyers designed to produce substantially-needed down cost help. Additional out there than most plans, it options helpful help for buying a principal residence.

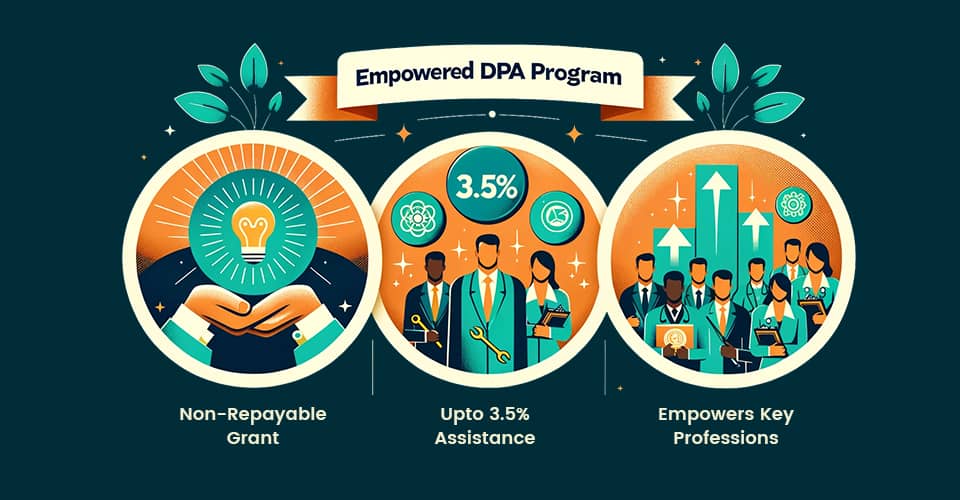

In distinction to many different down cost assist (DPA) packages, the Florida Empowered DPA Program stands out by providing as much as 3.5% of the property’s value.

This grant is not a financial institution mortgage that must be repaid however as a substitute a considerable supporting hand for homebuyers.

What It Delivers

Up to three.5% down cost assist grant.

Covers the whole down cost for an FHA monetary mortgage.

Grant is forgiven in the event you preserve the mortgage for at minimal six months.

Who Qualifies

To begin with-time homebuyers.

Military employees, 1st responders, educators, healthcare business consultants, governing administration staff.

Income earners as much as 140% of the space’s median earnings.

Consumers in underserved census tracts.

Method Necessities

Minimum 620 credit score historical past score.

Main house order solely.

Credit card debt-to-income ratio beneath 48.99%.

Authorized home types include one-spouse and youngsters properties, duplexes, produced houses, FHA-accepted condos, and PUDs.

Completion of accepted homeownership education course.

How to Implement

Contact a licensed home mortgage dealer like MakeFloridaYourHome.

Eligibility Demands for the Florida Empowered DPA Method

Homebuyers ought to meet positive necessities to fulfill eligibility for the Florida Empowered DPA Plan. These stipulations fluctuate from earnings restrictions to credit standing thresholds and sure situations related to the house.

Should be a initial-time homebuyer or not owned a house in the final three a number of years. OR at the second or beforehand a portion of the armed forces, preliminary responder, educator, medical specialist, or close by or federal govt worker.

Income should be 140% or considerably much less of the space’s median revenue.

The credit score rating rating ought to be a minimal of 620.

The dwelling ought to be for a significant house.

Credit card debt-to-income ratio not exceeding 48.99%.

Assets sorts contain one-spouse and youngsters houses, duplexes, made properties, FHA-authorized condos, and PUDs.

Completion of an authorised homeownership instruction research course is compulsory.

Benefits of the Florida Empowered DPA Method

Thanks to the Empowered DPA system, securing a property has by no means been easier.

Built for homebuyers in Florida, this method makes a path to homeownership by lowering monetary limitations and incomes residence-buying additional fairly priced.

Supplies as much as 3.5% down cost help on the house’s purchased worth.

Gives a non-repayable grant that may assist protected an FHA mortgage simply.

Maintains broader requirements, constructing the software program out there to a broad number of homebuyers.

Empowers important professions like military personnel, educators, and first responders with homeownership alternatives.

Facilitates homebuyers whose earnings is 140% or fewer of the regional median income.

Supports homebuyers intending to acquire property in underserved census tracts.

How Does the Florida Empowered DPA Method Get the job accomplished?

The Florida Empowered DPA System follows a clear-cut process to help homebuyers. Listed listed below are the methods:

Prequalification – Start out by deciding in the event you fulfill the program’s eligibility requirements.

Uncover an permitted lender – Function with a monetary establishment affiliated with the software program to make the most of for the DPA.

Application – Submit your software program to the technique.

Closing – At the time authorised, full the required strategies to close your house.

Article-purchase support – Acquire ongoing help and steering instantly after getting your residence.

The Florida Empowered DPA Software simplifies house shopping for by furnishing a structured action-by-phase answer. This makes it quite a bit simpler for attainable house owners to navigate and protected a home.

What are the Key Functions of the Florida Empowered DPA System?

The Florida Empowered DPA Method helps with down funds, lowers rates of interest, options versatile mortgage choices, and presents education for to start out with-time homebuyers.

It additionally addresses fairly just a few kinds of properties. This plan does additional than the regular mortgage, producing it a lot simpler for additional individuals to buy homes.

Down Payment Guidance

The Florida Empowered DPA System assists homebuyers with the unique cost desired to spend money on a property. It delivers as much as 3.5% of the house’s buy promoting value, which might take care of the complete down cost if you’re getting an FHA mortgage.

This could make it a lot simpler for quite a few folks right now to purchase their very first dwelling, as developing with the down cost is usually the hardest part.

Interest Amount Reduction

The program additionally lessens the curiosity charge on house loans, which lowers common funds. This discount might help you save homebuyers a complete lot of income greater than time, creating households extra cheap.

It is particularly helpful for these individuals who must have to carry their common month-to-month prices down.

Adaptable Bank mortgage Terms

The Florida Empowered DPA Application presents versatile situations for your own home mortgage. This suggests you possibly can regulate your mortgage to suit your monetary downside improved.

Whether you need decrease month-to-month funds or a singular private mortgage length, this utility helps make it achievable. It’s constructed to make buying a residence significantly much less demanding and extra out there to totally different purchasers.

To begin with-Time Homebuyer Education and studying

If you’re acquiring your 1st residence, this program consists of an instruction class that teaches you about the property-getting method.

You will discover out essential elements like mortgage mortgage primary ideas and how you can funds for your new residence. This instruction permits you make educated conclusions and prepares you for homeownership.

Assets Eligibility

The system is not actually simply for solitary-household houses it additionally consists of duplexes, made residences, FHA-authorized condos, and Planned Device Developments (PUDs).

This range permits much more potential consumers to acquire residences that match their necessities, whether or not or not they’re wanting for an inexpensive selection or a family that may additionally create rental income.

Empowered DPA Software FAQs

Here we have now answered 10 routinely requested inquiries about the Florida Empowered DPA Program.

What is the Florida Empowered DPA Software?

The Florida Empowered DPA Program is a down cost help initiative developed to assist first-time homebuyers and appropriate specialists reminiscent of army personnel and educators protected financing for their primary residences in Florida.

Who qualifies for the Florida Empowered DPA Software?

Eligibility is prolonged to initial-time homebuyers, navy employees, 1st responders, educators, health-related business consultants, and federal authorities personnel.

Applicants will need to have incomes not more than 140% of their space’s median cash and be buying in chosen underserved locations.

What economical assist does the Florida Empowered DPA Application present?

The system delivers as much as 3.5% in down cost help as a non-repayable grant, masking the full down cost for an FHA private mortgage, supplied the borrower retains the house for at the very least six months.

What are the credit standing requirements to qualify for the software program?

Applicants must have a least credit standing score of 620 to qualify for the Florida Empowered DPA Software.

What varieties of homes are eligible for the program?

Suitable homes contain solitary-household households, duplexes, made houses, FHA-approved condos, and Prepared Device Developments (PUDs).

Is there an educational requirement for the technique?

Sure, candidates are anticipated to complete an permitted homeownership education class to qualify for the down cost help out there by the Florida Empowered DPA Software.

What is the biggest debt-to-earnings ratio permitted beneath the program?

The technique permits for a bank card debt-to-cash movement ratio of as much as 48.99% for certified candidates.

How does 1 apply for the Florida Empowered DPA Program?

Opportunity candidates ought to talk to an accepted home mortgage dealer, this type of as MakeFloridaYourHome, to start out off the utility system for the Florida Empowered DPA Method.

How very lengthy must I maintain the dwelling to not repay the grant?

The down cost help introduced by the utility is forgivable after 6 months of retaining the financial institution mortgage and property.

Can the down cost assist be blended with different economical assist?

Certainly, the down cost help from the Florida Empowered DPA Method can usually be put along with different varieties of cash help, nevertheless candidates should validate distinctive info with their mortgage supplier.

Speak to MakeFloridaYourHome these days to see how considerably funds you possibly can protect with Empowered DPA. Satisfied homebuying!

With over 50 yrs of property finance mortgage sector expertise, we’re right here that can assist you attain the American aspiration of proudly proudly owning a house. We attempt to give the splendid schooling and studying proper earlier than, for the length of, and shortly after you buy a dwelling. Our recommendation is primarily based totally on experience with Phil Ganz and Group closing above A particular person billion {dollars} and aiding many households.