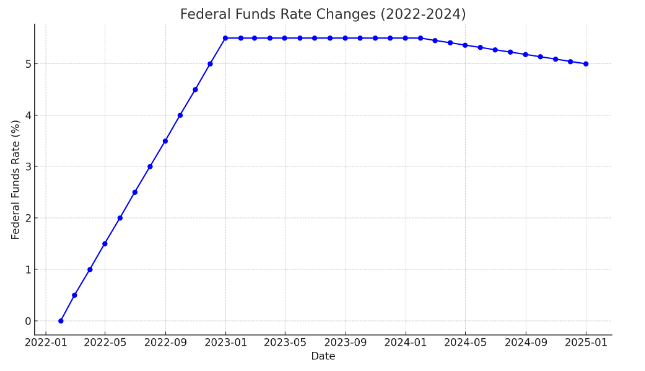

With regular mortgage premiums above 6% contemplating that late 2022, the potential for refinancing train is rising, a brand new report positioned.

Somewhere round 24% of home mortgage holders presently have a stage earlier talked about 5%, much more than double the share since 2022, in accordance to particulars from Intercontinental Exchange’s mortgage technological innovation unit.

“As not way back as two a number of years prior to now, an astonishing 9 of nearly each 10 house mortgage holders had been beneath that threshold,” defined Andy Walden, vice chairman of analysis and evaluation at ICE House mortgage Technological innovation, in a push launch.

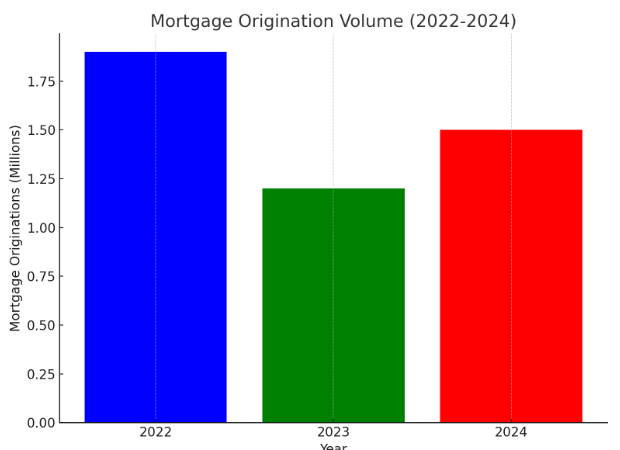

Loan suppliers have originated 4 million house loans with expenses beforehand talked about 6.5% provided that mid 2022, with 1.9 million of people sitting down above 7%, ICE’s common month-to-month Mortgage Monitor report claimed.

Throughout the current housing sector, 5.8 million a lot much less sub-5% mortgages exist immediately in comparison with the exact same time time period in 2022. The share with sub-4% charges lowered by 4.8 million.

But whereas property homeowners present as much as take bigger expenses may presumably be right here to remain, it does not imply they don’t seem to be looking at strategies to offer them down.

In an ICE Mortgage Technologies borrower survey from this yr, greater than two-thirds of respondents reported getting essentially the most reasonably priced fee was 1 of an important points in choosing out their mortgage firm. The 68% share rated very nicely above the following most important ingredient — low monetary establishment charges, cited by 47%. Closing speeds trailed in third spot at 33%.

In spite of their apparent stage sensitivity, though, debtors additionally usually are not getting time to window store. A large majority appeared at two mortgage corporations or fewer simply earlier than taking out their private mortgage. Thirty-6 % considered as just one specific house finance mortgage company, with simply beneath fifty %, or 48%, considering two. The info parallels present examine from Lendingtree that equally noticed a good greater proportion of debtors most likely to go together with the initially current they gained.

But Walden additionally pointed to alternatives among the many the newer borrower profiles. Extra fashionable increased-level originations stand for a attainable pipeline for future refinances when the second is good.

While the share of debtors with premiums above 6% is rising, a visual uptick confirmed up within the quantity of monetary loans with expenses simply beneath 7% as against over that threshold. The spike of 690,000 debtors in that distinctive selection possible comes from house owners choosing out to spend money on down their expenses, ICE proposed.

“The focus of full of life loans simply beneath 7% has further to do with borrower psychology than concrete private financial savings. You will discover clearly a factor fascinating in current day market place for a home proprietor to see a ‘6’ handle in entrance of their property finance mortgage value,” Walden noticed.

“From a cost/expression refinance lending viewpoint, this staff is worthy of seeing as they signify a potential tipping level for a return to further important, albeit historically modest, refi volumes.”

Even although refinances are even now coming in completely under historic ranges, near 1-Third of quantity in present months have been fee-and-time interval transactions, with a necessary surge in loans confirmed by the Section of Veterans Affairs. April refinances of VA monetary loans resulted in an common $231 discount in month-to-month funds, in accordance to ICE’s report. The technological innovation service supplier additionally discovered a superior share of early-2024 refinances coming from house loans originated inside the previous calendar 12 months.

But any future upturn in refis couldn’t conclusion up spreading the wealth equally all through the lending area people, a brand new report from Stratmor Group acknowledged. Lenders that purchased off servicing rights for liquidity within the current slowdown, will uncover by themselves at an obstacle when going up versus corporations who retained them. The latter can leverage their present interactions to maintain clientele as a substitute than counting on induce leads.

“I’ve talked with a number of collectors who assume on the core of their beings that as earlier than lengthy as the upcoming wave of refinances hits the corporate, all of their issues will go absent,” acknowledged Stratmor senior companion Garth Graham. “But that is not actually assured.”