Anyone out looking for a home in the present day is aware of there’s still valuable little on the market.

The housing market is simply starting to come back out of its leanest few years in historical past. Inventory of each new and current houses is lastly rising, however there’s something instantly unusual within the numbers: The provide of newly constructed houses seems to be manner too excessive.

The numbers, nonetheless, are deceiving as a result of unprecedented dynamics of in the present day’s housing market, which will be traced again 20 years to a different unprecedented time in housing, the subprime mortgage growth.

All of it’s exactly why home prices, which normally cool off when provide is excessive, simply proceed to rise.

The provide situation

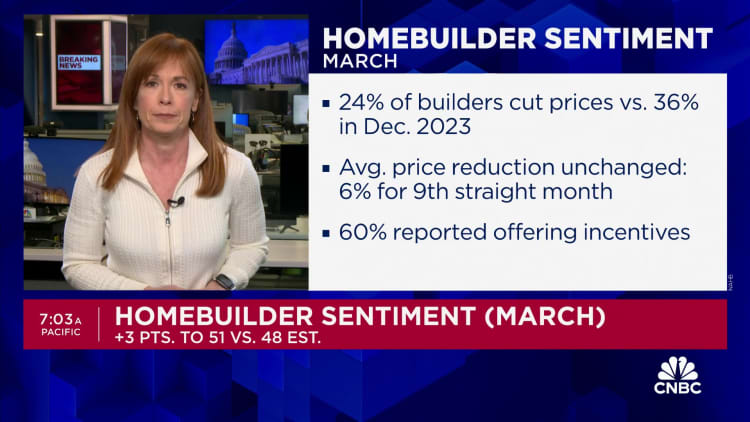

There is at the moment a 4.4-month provide of each new and current houses on the market, based on the National Association of Home Builders, or NAHB. Months’ provide is a typical calculation used out there to measure how lengthy it will take to promote all of the houses accessible on the present gross sales tempo. A six-month provide is taken into account a balanced market between a purchaser and a vendor.

Supply was already low initially of this decade, however pandemic-driven demand pushed it to a document low by the beginning of 2021 at simply two-months’ provide. That scarcity of houses on the market, mixed with robust demand, pushed home prices up greater than 40% from pre-pandemic ranges.

Now provide is lastly starting to climb again, however the good points are principally within the new home market, not on the present facet. In reality, there’s now a nine-month provide of newly constructed houses on the market, almost 3 times that of current houses. New and outdated home months’ provide normally monitor fairly carefully. New development now makes up 30% of whole inventory, about twice its historic share, based on the NAHB.

Single-family houses in a residential neighborhood in San Marcos, Texas.

Jordan Vonderhaar | Bloomberg | Getty Images

“June 2022 recorded the biggest ever lead of latest home months’ provide (9.9) over current single-family home months’ provide (2.9),” wrote Robert Dietz, chief economist for the NAHB. “This separation makes it clear that an analysis of present market inventory can’t merely look at both the present or the brand new home inventory in isolation.”

This uncommon dynamic has been pushed by each current swings in mortgage charges and an unprecedented catastrophe within the housing market that started 20 years in the past.

The basis of in the present day’s tough numbers

This housing market is in contrast to every other due to financial forces in contrast to every other. First, in 2005, there was a large runup in home gross sales, homebuilding and home prices fueled by a surge in subprime mortgage lending and a frenzy of buying and selling in new monetary merchandise backed by these mortgages.

That all got here crashing down shortly, leading to one of many worst foreclosures crises because the Great Depression and inflicting the following Great Recession. Single-family housing begins plummeted from a excessive of 1.7 million models in 2005 to simply 430,000 in 2011. By 2012, new houses made up simply 6% of the overall for-sale provide and, even by 2020, housing begins had but to recuperate to their historic common of about 1.1 million models. They sat at 990,000.

Then got here the Covid-19 pandemic and through that point, shopper demand surged and mortgage charges set greater than a dozen document lows, so builders responded. Housing begins shot as much as 1.1 million in 2021. The Federal Reserve was bailing out the economic system, making homebuying less expensive, and the brand new work-from-home tradition had Americans shifting like by no means earlier than. Suddenly, provide was sucked right into a twister of demand.

Mortgage charge mayhem

The present unusual divide in provide between newly constructed and current houses can be as a result of roller-coaster mortgage charges, dropping to historic lows initially of the pandemic after which spiking to 20-year highs simply two years later. Millions of debtors refinanced on the lows and now don’t have any need to maneuver as a result of they must commerce a 3% or 4% charge on their loans to the present charge, which is round 7%. This lock-in impact precipitated new listings to dry up.

It additionally put builders within the driver’s seat. Homebuilders had already ramped up manufacturing within the first years of the pandemic, with single-family houses surging to greater than 1.1 million in 2021, based on the U.S. census, earlier than dropping again once more when mortgage charges shot up. Builders have been in a position to purchase down mortgage charges to maintain gross sales increased, however as of this May, they are constructing at an annualized tempo of 992,000.

Resale listings improved barely this spring, as mortgage charges fell again barely, and by June, lively listings had been 16.5% increased than they had been the yr earlier than, based on Redfin. Some of that elevated provide, nonetheless, was as a result of listings sitting in the marketplace longer.

“The share of houses sitting in the marketplace for at the very least one month has been growing yr over yr since March, when progress in new listings accelerated, however demand from patrons remained tepid, as it has been since mortgage charges began rising in 2022,” based on a Redfin report.

A home accessible on the market is proven in Austin, Texas, on May 22, 2024.

Brandon Bell | Getty Images

Growth on the low finish

On the resale market, the availability is lowest within the $100,000 to $500,000 value tier, based on the National Association of Realtors. That is the place the majority of in the present day’s patrons are. Higher mortgage charges have them searching for cheaper houses.

Interestingly, nonetheless, whereas provide is growing throughout all value tiers, it’s growing most in that very same lower-end value tier, that means it’s merely not sufficient. As quick as the houses are coming in the marketplace, they are going underneath contract.

For instance, there’s only a 2.7-month provide of houses on the market between $100,000 and $250,000, however provide is up 19% from a yr in the past. Meanwhile, there’s a 4.2-month provide of houses priced upward of $1 million, however provide is up simply 5% from a yr in the past.

This explains why home prices stay stubbornly excessive, even with enhancing provide. Prices in May, the newest studying, had been 4.9% increased than May 2023, based on CoreLogic. The good points have begun to shrink barely, however not all over the place.

“Persistently stronger home value good points this spring proceed in markets the place inventory is effectively under pre-pandemic ranges, such as these within the Northeast,” mentioned Selma Hepp, chief economist for CoreLogic.

“Also, markets that are comparatively extra inexpensive, such as these within the Midwest, have seen wholesome value progress this spring.”

Hepp notes that Florida and Texas, which are seeing comparatively bigger progress within the provide of houses on the market, are now seeing prices under the place they had been a yr in the past.

While analysts have anticipated prices to ease and mortgage charges to come back down within the second half of this yr, it stays to be seen if charges will really come down and if the supply-demand imbalance will enable prices to chill. If mortgage charges do come down, demand will certainly surge, placing even extra stress on provide and protecting prices elevated.

“Yes, inventory is rising and can proceed to rise, significantly as the mortgage charge lock-in impact diminishes within the quarters forward. But present inventory ranges proceed to assist, on a nationwide foundation, new development and a few value progress,” Dietz added.