Finances 24-25: Modest gains amidst new spending | Australian Broker News

Information

Funds 24-25: Modest gains amidst new paying

Fiscal stability in 2024-25 price range, claims ANZ

As the 2024-25 Australian federal funds methods, Adam Boyton, head of Australian Economics at ANZ, forecasts a stability regarding modest surplus gains and substantial new investing.

“We assume a modest enchancment within the fiscal place,” Boyton claimed, highlighting a strategic economical administration tactic.

Forecasted surpluses and deficits

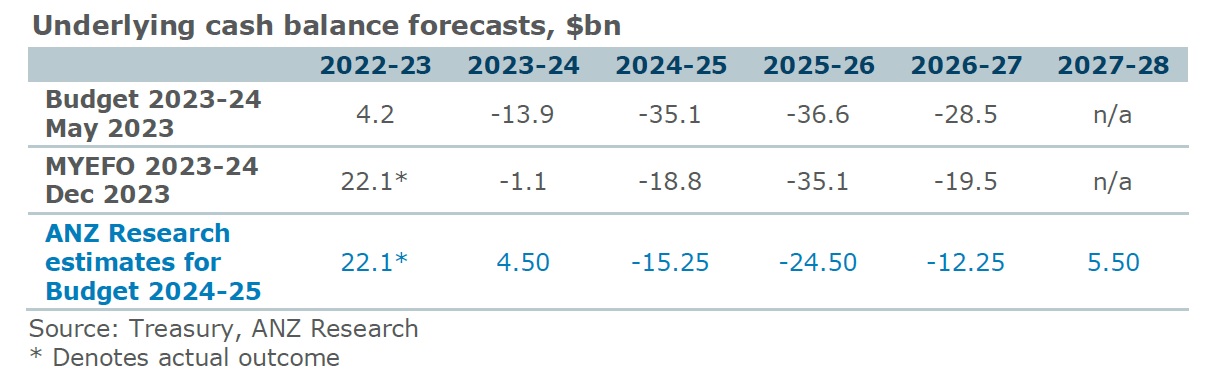

The future spending plan is predicted to reveal an elementary funds surplus of $4.5 billion for 2023-24, with a change to a projected deficit of $15.25bn in 2024-25. Continuing deficits are predicted for the next two yrs, with a return to surplus projected for 2027-28.

New expenditures and financial implications

ANZ anticipates new paying initiatives totaling roughly $2.5bn in 2023-24 and escalating to $10bn in 2024-25. These investments are poised to kind many sectors with out impacting growth, inflation, or curiosity cost forecasts drastically.

Boyton highlighted the possible impacts of those fiscal actions, stating, “Such a level of internet new paying is dependable with our test out that the spending price range would comprise a discretionary fiscal easing.”

Anticipating responses to tax cuts

A considerable a part of the price range’s achievement will hinge on client reactions, notably to the Phase 3 tax cuts.

“Of way more nice significance shall be how patrons react,” Boyton talked about. This response will present as an early indicator of the price range’s genuine-earth outcomes, influencing something from particular paying practices to broader financial traits.

Changes and expectations

Whilst the Treasury’s monetary forecasts are anticipated to maintain on being largely fixed with prior predictions, there are anticipated changes based on present information. Notably, nominal GDP development for 2024-25 is envisioned to outpace earlier estimates, probably boosting funds revenues.

“On main of a much better commencing place, it seems potential nominal GDP progress in 2024-25 shall be extra sturdy than predicted,” Boyton claimed.

ANZ on strategic fiscal administration for long run safety

As Australia navigates through many monetary pressures – from protection shelling out to social options – ANZ Exploration immediate that strategic fiscal administration shall be important.

“With structural pressures creating on the spending plan, among the measures within the funds might be centered to chop down medium-expression development in shelling out,” Boyton claimed, indicating a cautious nonetheless optimistic outlook for Australia’s fiscal foreseeable future.

Get the most popular and freshest mortgage mortgage information shipped proper into your inbox. Subscribe now to our FREE every day e-newsletter.

Hold up with the newest info and conditions

Be a part of our mailing listing, it’s no value!