The Federal Housing Administration (FHA) is shifting to extend its COVID-19 reduction mitigation “waterfall” by introducing a 40-year mortgage modification choice and is inquiring the mortgage loan market for enter.

The proposed rule, printed by the Department of Housing and Urban Development late final week, would change compensation provisions for FHA debtors, enabling collectors to recast a borrower’s entire unpaid mortgage for an additional 120 months. HUD stated that this option may shield in opposition to “a number of thousand debtors a yr from foreclosures.”

By prolonging the period of the recast home loan from 360 months to 480 months, debtors may have further sustainable common month-to-month funds, the part said. The proposed rule well-known that a lower month-to-month fee will allow present a borrower’s home loan latest, cease imminent re-default, and naturally, help debtors retain their home.

The proposed rule will completely be efficient for FHA debtors who not too way back exited governing administration-mandated forbearance however are having difficulties to make their home loan funds since of COVID-19 linked economical hardships.

Along with of benefitting debtors, the rule would additionally decrease losses to FHA’s Mutual Home finance loan Insurance Fund as a lot much less attributes could be purchased at a loss in foreclosures or out of FHA’s real property owned stock, HUD said.

A latest report revealed by the FHA unveiled that as of December 2021, 7.28% of FHA monetary loans had been considerably delinquent, down from a seasonally modified important of 12.04% in March 2021. Nevertheless, the extent remains to be elevated in comparison with pre-pandemic occasions.

What will servicing look like in 2022?

Conversation, borrower schooling and studying and coaching of consumer-dealing with employees are all vital points to make sure your servicing process is correctly geared as much as support debtors as they exit forbearance concepts.

Presented by: Selene Finance

HUD further that debtors who go for a 40-yr personal loan modification could be subject material to slower fairness accumulation and supplemental fascination funds, however that the helpful results of a borrower staying succesful to retain their residence should outweigh any negatives.

If executed, the rule will align the FHA with different governing administration entities, equivalent to Fannie Mae, Freddie Mac, and the United States Office of Agriculture, which beforehand provide a 40-calendar yr mortgage modification expression answer.

Remarks from the mortgage loan market are due to by May maybe 31.

FHA’s 40-year personal loan modification option has been within the works for quite a while.

In June 2021, Ginnie Mae introduced that it was established to introduce a 40-calendar yr residence loan phrase for its issuers, however that the phrases and extent of use of the brand new pool selection could be in the end determined by the FHA.

3 months afterwards, the FHA posted a draft home loan letter proposing a 40-yr monetary loan modification mixed with a partial declare.

On the opposite hand, market stakeholders, just like the Housing Coverage Council and the Mortgage Bankers Association, sought a lot extra time to alter to the modify. HPC and the MBA requested the FHA to carry off the using of the brand new time period till the very first quarter of 2022. They additionally requested the govt. company for a 90-day window to start out presenting the financial institution loan modification.

“The want on servicers to place into motion a big range of coverage adjustments across the last a number of months has been sophisticated and we count on this to maintain on completely into the first quarter of 2022,” they stated in a letter to FHA.

In early February, Julienne Joseph, deputy assistant secretary within the Business of Solitary-Loved ones Housing for FHA, said that the federal government company is “nearly there” and “getting hotter” in presenting the answer to debtors.

“Of coaching course, we sense time is of the essence, particularly given that the countrywide surprising emergency has been prolonged,” she reported on the MBA’s Servicing Answers Convention & Expo 2022 in Orlando, Florida. On Feb. 18, President Biden prolonged the countrywide disaster declaration for the COVID-19 pandemic past March 1.

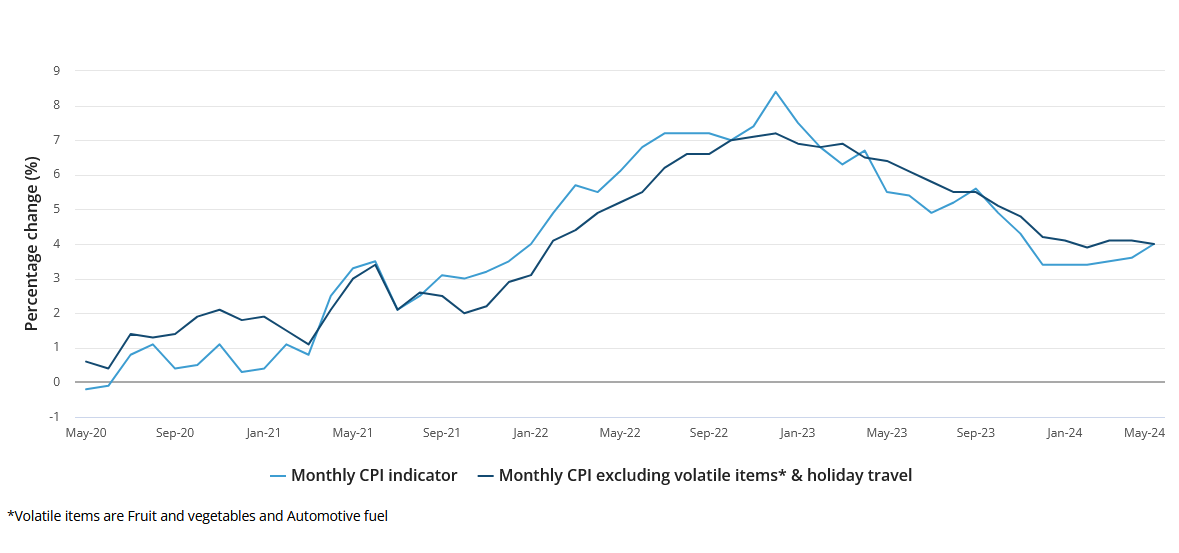

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator