Canstar on most recent home mortgage worth variations | Australian Broker Information

News

Canstar on most up-to-date home private mortgage degree alterations

Charge variations affect debtors

New actions in dwelling mortgage costs, as documented by Canstar, confirmed fluctuations throughout every variable and mounted charges for owner-occupiers and merchants.

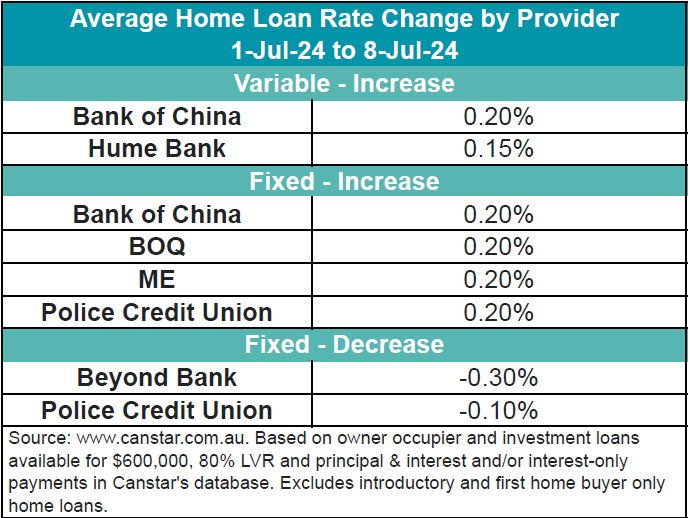

Two lenders elevated six proprietor-occupier and dealer variable premiums by an unusual of .17%.

In addition, 4 mortgage firms raised 76 proprietor-occupier and dealer preset prices by an common of .20%, when two lenders scale back eight owner-occupier and dealer mounted charges by an regular of .15%.

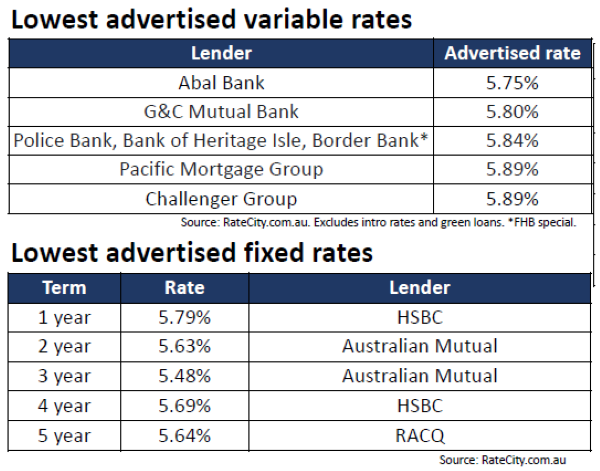

Existing variable price overview

The regular variable curiosity price for operator-occupiers shelling out principal and fascination is now 6.88%. The most reasonably priced variable quantity for any mortgage-to-worth ratio (LVR) is 5.89%, made obtainable by Pacific Mortgage Group and The Mutual Bank. Notably, there are 23 charges beneath 5.75% on Canstar’s database.

Canstar’s insights on fee enhancements

Steve Mickenbecker (pictured earlier talked about), Canstar’s group govt of economical professional providers and important commentator, equipped insights into the value variations and the broader financial context.

“The Reserve Financial establishment minutes that arrived out final week have achieved little or no to allay debtors’ issues that the expectation of fee cuts this 12 months are fading absent,” Mickenbecker claimed.

Influence of dwelling charges and inflation

Mickenbecker highlighted the continued improve in home expenses and protracted inflation as vital variables influencing the Reserve Bank’s stance on want charges.

“House fee will increase proceed and are usually not going to provide the Reserve Financial establishment any encouragement to attenuate early, however it’s sticky inflation that’s executing the harm,” he talked about.

Rate boosts for loans and bank cards

Reflecting on the quantity raises, Mickenbecker stated, “Unfortunately the expectations of great charges for prolonged have mirrored in will increase to a handful of dwelling monetary loans and credit score historical past playing cards throughout the week. At this stage it’s not an explosion, additional a creep, however the magnitude is disturbing, with the cardboard purchase quantity raises averaging 1.15%.”

Favourable info for savers

Amidst the speed hikes, there’s some useful info for savers.

“There is a few superior info for savers, with 4 banking establishments lifting financial savings account prices by an lovely frequent of .31% and eight boosting time interval deposits by an fascinating common of .62%,” Mickenbecker acknowledged.

Get the hottest and freshest property finance mortgage info shipped proper into your inbox. Subscribe now to our FREE every day publication.

Related Tales

Maintain up with the most recent information and actions

Be a part of our mailing record, it’s no price!