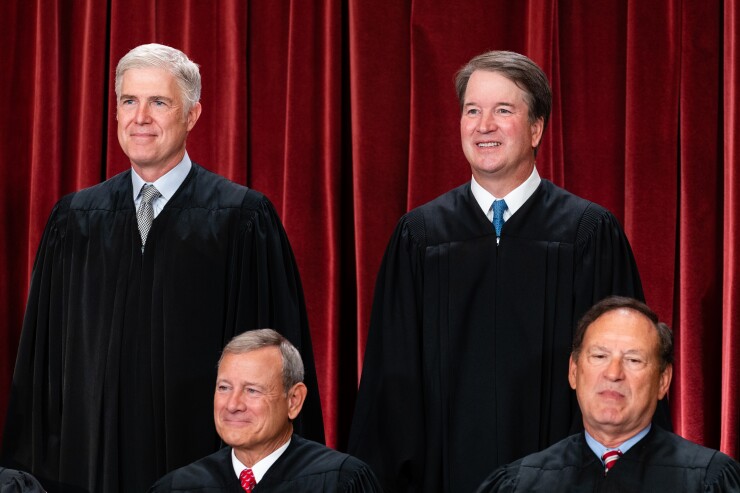

The feeling overturning Chevron deference was created by Main Justice John Roberts (base left) and joined by Justices Samuel Alito (backside acceptable), Neil Gorsuch (main correct) and Brett Kavanaugh (prime rated correct), in addition to Justices Clarence Thomas and Amy Coney Barrett (not pictured).

The feeling overturning Chevron deference was created by Main Justice John Roberts (base left) and joined by Justices Samuel Alito (backside acceptable), Neil Gorsuch (main correct) and Brett Kavanaugh (prime rated correct), in addition to Justices Clarence Thomas and Amy Coney Barrett (not pictured).

Eric Lee/Bloomberg

The Supreme Court on Friday overturned a big authorized precedent requiring judges to defer to federal regulatory companies’ interpretation of ambiguous statutes. The 6-3 ruling reduces the power of a in depth collection of authorities division companies, which embody lender regulators, to interpret guidelines.

The 40-calendar year-aged lawful doctrine — recognised as Chevron deference, named for the 1984 Supreme Courtroom choice in Natural Means Protection Council v. Chevron organising the precedent — had extended aggravated corporations in managed industries as a result of it constrained their means to sue companies above their interpretations of vast or obscure authorized authorities.

The doctrine incessantly meant that regulators might create broader, way more expensive pointers than managed corporations thought-about have been warranted. Its demise is anticipated to open up the floodgates to a wave of litigation demanding such ideas.

But the shut of Chevron deference may very well be a double-edged sword for banking establishments, in response to sector authorized professionals, given that the Supreme Court’s conclusion will even make it easier for advocacy teams and state attorneys typical to problem guidelines they oppose, which might introduce further uncertainty for banking corporations.

The ruling by the massive court docket’s conservative higher half, printed by Main Justice John Roberts, held that the Administrative Course of motion Act requires courts to work out their unbiased judgment in figuring out irrespective of if an company has acted within its statutory authority. Courts have the choice to defer to an company’s interpretation of an ambiguous regulation, however the court docket stated the agency prerequisite that it must is wrong.

“The deference that Chevron requires of courts inspecting firm movement can’t be squared with the APA,” Roberts wrote. “Potentially most primarily, Chevron’s presumption is misguided since companies don’t have any particular competence in resolving statutory ambiguities. Courts do.

“Chevron has proved to be mainly misguided,” he ongoing. “And its flaws had been apparent from the get began, prompting the Courtroom to revise its foundations and consistently restrict its software program. Experience has additionally confirmed that Chevron is unworkable.”

The court docket’s dedication encompassed two situations: Loper Dazzling Enterprises v. Raimondo and Relentless v. Section of Commerce. The conditions included fishermen in New Jersey and Rhode Island who claimed the Countrywide Marine Fisheries Provider couldn’t impose a price necessitating federal observers on herring boats, centered on the relevant regulation.

In a dissenting impression, Justice Elena Kagan wrote that for 40 a long time, Chevron deference has served “as a cornerstone of administrative laws, allocating accountability for statutory design in between courts and firms.”

“This Court docket has in depth acknowledged Chevron deference to mirror what Congress would need, and so to be rooted in a presumption of legislative intent,” wrote Kagan, who was joined by Justice Sonia Sotomayor. “Congress is aware of that it doesn’t — in truth cannot — publish fantastically whole regulatory statutes.”

Justice Ketanji Brown Jackson joined the dissent in one explicit of the 2 conditions however was recused from the opposite as a result of she took part in it as a federal appeals courtroom select.

Going ahead, federal companies might be lower than larger scrutiny, offering area actors much more prospects to impediment firm insurance policies and interpretations of the regulation, attorneys defined.

“The selection may very well be considered as putting regulated communities on a much more equal footing with the companies,” said Varu Chilakamarri, a companion on the laws enterprise Okay&L Gates.

The stakes present as much as be specifically excessive for the Customer Economic Defense Bureau. The CFPB has a standing as staying much more intense than another federal organizations, and thru the Biden administration, the bureau has situated its pointers routinely challenged in court docket docket.

The CFPB said Friday that it’s inspecting the ruling and declined to comment.

The CFPB’s interpretations of guidelines will now be subject to “heightened assault,” defined Joe Lynyak, a partner at Dorsey & Whitney.

“Courts all around the area could also be inundated with personal get-togethers who might maybe now litigate and relitigate an firm interpretation, resembling creating conflicting decisions by decreased courts,” Lynyak talked about.

Eamonn Moran, senior counsel at Norton Rose Fulbright, claimed the rollback of Chevron deference might effectively final consequence in the overturning of restrictions this sort of because the CFPB’s $8 bank card late payment rule. But he additionally cautioned about seemingly downsides for banking establishments.

“Although there could be now further likelihood for the plaintiff’s authorized professionals to contemplate to undo laws on account of courtroom challenges, business would possibly now be confronted with lack of predictability and compliance troubles,” Moran talked about.

Leah Dempsey, co-chair of the fiscal skilled providers observe on the laws group Brownstein Hyatt Farber Schreck, pointed to what she described as worries for regulated companies stemming from the court docket’s dedication, in addition to the possibilities.

In an interview previous to the final decision was produced, Dempsey stated that corporations are usually looking out for readability on how one can function, and argued that the demise of Chevron might restrict the talent of companies to offer a lot of these readability.

Kate Decide, a professor at Columbia Regulation School, wrote in a social media write-up that banks, like fairly a couple of corporations, “might probably see Chevron’s slide as a earn, however the Chevron doctrine was central in facilitating deregulation.”

“The consequence now doesn’t suggest a lot much less regulation it simply makes sure way more uncertainty concerning the obligations the regulation imposes on managed entities,” Judge wrote on X, beforehand recognised as Twitter.

Joann Needleman, an lawyer on the laws firm Clark Hill, well-known that a number of legal guidelines which have an have an effect on on the economical corporations sector are a long time earlier, so they won’t present clear steering about how organizations might use newer technological innovation. It has very lengthy been as much as regulators to fill in these gaps.

Needleman defined that following the demise of Chevron deference, she will be able to foresee litigation by shopper advocates difficult pointers that the CFPB arrange as regards to using modern communications applied sciences by debt collectors. The CFPB’s 2020 rule implementing the Good Personal debt Assortment Procedures Act addresses using e-mail and textual content material messages by debt collectors. Advocates have opposed sections of the regulation.

Needleman, who’s a former president of the board of administrators of the Countrywide Collectors Bar Affiliation, claimed in an job interview proper earlier than the court docket’s choice was produced that the CFPB’s rule supplies a contemporary interpretation of a many years-previous regulation.

“A substantial amount of what the CFPB did about that regulation was undoubtedly useful,” she said.

The Supreme Court’s 6-3 selection in a situation involving the Securities and Trade Fee hinges on Seventh Modification of the U.S. Structure, which enshrines the fitting to a jury demo specifically circumstances.

The Supreme Court’s 6-3 selection in a situation involving the Securities and Trade Fee hinges on Seventh Modification of the U.S. Structure, which enshrines the fitting to a jury demo specifically circumstances. The Thurgood Marshall United States Courthouse in New York. The collection of lawsuits filed beneath the Fair Credit Reporting Act has spiked in the newest years, typically by plaintiffs symbolizing on their very own and impressed by a creating cottage market of social media influencers and trial authorized professionals searching for restitution for meant errors in their credit historical past reviews.

The Thurgood Marshall United States Courthouse in New York. The collection of lawsuits filed beneath the Fair Credit Reporting Act has spiked in the newest years, typically by plaintiffs symbolizing on their very own and impressed by a creating cottage market of social media influencers and trial authorized professionals searching for restitution for meant errors in their credit historical past reviews.

Lots of licensed specialists really feel the Supreme Courtroom will rule in favor of the Customer Fiscal Safety Bureau in a case robust its funding. This type of a ruling would unleash a flurry of litigation that has been on keep pending the consequence of the constitutional impediment.

Lots of licensed specialists really feel the Supreme Courtroom will rule in favor of the Customer Fiscal Safety Bureau in a case robust its funding. This type of a ruling would unleash a flurry of litigation that has been on keep pending the consequence of the constitutional impediment.