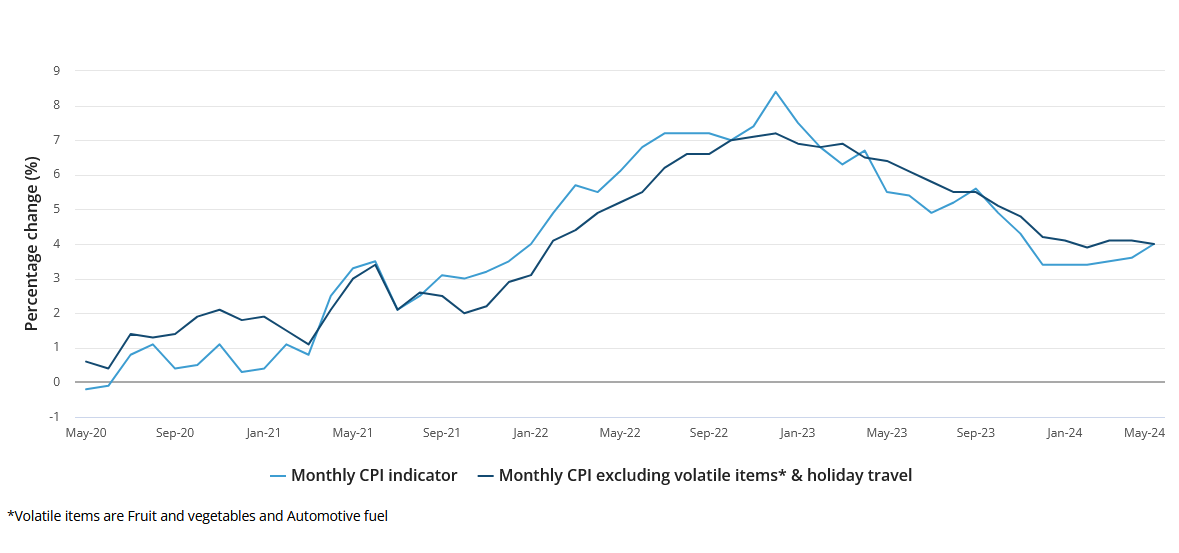

Recent indicators that inflation is easing has paved the way in which for the Federal Reserve to begin chopping rates of interest as quickly as this fall.

The shopper worth index, a key inflation gauge, dipped in June for the primary time in additional than 4 years, the Labor Department reported final week.

“With plentiful indicators of a cooling financial system, the patron worth index for June definitely constitutes the ‘extra good knowledge’ on inflation that Fed Chair Jerome Powell has stated we want to see earlier than the Fed can start chopping rates of interest,” stated Greg McBride, chief monetary analyst at Bankrate.com.

With a fall rate cut trying extra doubtless now, households could lastly get some aid from the sky-high borrowing prices that adopted the newest sequence of curiosity rate hikes, which took the Fed’s benchmark rate to the best degree in a long time.

More from Personal Finance:

High inflation is basically not Biden’s or Trump’s fault, economists say

Why housing inflation remains to be stubbornly excessive

More Americans are struggling at the same time as inflation cools

Fed officers signaled they count on to cut its benchmark rate as soon as in 2024 and 4 further occasions in 2025.

The federal funds rate, which is about by the U.S. central financial institution, is the curiosity rate at which banks borrow and lend to each other in a single day. Although that is not the rate shoppers pay, the Fed’s moves nonetheless have an effect on the charges they see every single day on issues resembling personal pupil loans and bank cards.

“If you might be a shopper, now’s the time to say, what does my spending appear to be? Where would my money develop essentially the most and what choices do I’ve?” stated Leslie Tayne, an lawyer specializing in debt aid at Tayne Law in New York and creator of “Life & Debt.”

Here are three key methods to contemplate:

1. Watch your variable-rate debt

With a rate cut, the prime rate lowers, too, and the rates of interest on variable-rate debt — resembling bank cards, adjustable-rate mortgages and a few personal pupil loans — are doubtless to observe, lowering your month-to-month funds.

For instance, credit score cardholders may see a discount of their annual proportion yield, or APR, inside a billing cycle or two. But even then, APRs will solely ease off extraordinarily excessive ranges.

Rather than look ahead to a small adjustment within the months ahead, debtors may swap now to a zero-interest stability switch bank card or consolidate and repay high-interest bank cards with a private mortgage, Tayne stated.

Olga Rolenko | Moment | Getty Images

Many householders with ARMs, that are pegged to a selection of indexes such because the prime rate, Libor or the eleventh District Cost of Funds, might even see their curiosity rate go down as properly — though not instantly as ARMs usually reset simply as soon as a yr.

In the meantime, there are fewer choices to present householders with further respiratory room. “Your higher transfer could also be ready to refinance,” McBride stated.

Private pupil loans additionally have a tendency to have a variable rate tied to the prime, Treasury invoice or one other rate index, which suggests as soon as the Fed begins chopping rates of interest, the rates of interest on these personal pupil loans will begin dropping.

Eventually, debtors with current variable-rate personal pupil loans may additionally have the opportunity to refinance into a cheaper fixed-rate mortgage, in accordance to larger training skilled Mark Kantrowitz.

Currently, the fastened charges on a personal refinance are as little as 5% and as excessive as 11%, Kantrowitz stated.

2. Lock in financial savings charges

While borrowing will turn into cheaper, these decrease rates of interest will harm savers.

Since charges on on-line financial savings accounts, money market accounts and certificates of deposit are all poised to go down, specialists say that is the time to lock in some of the best returns in a long time.

For now, top-yielding on-line financial savings accounts and one-year CDs are paying greater than 5% — properly above the rate of inflation.

The alternative to earn 5% yearly on these money investments could not final for much longer.

Howard Hook

wealth advisor with EKS Associates

“One factor it’s your decision to do is contemplate investing any idle money you will have into a higher-yielding money market fund,” stated licensed monetary planner Howard Hook, a senior wealth advisor with EKS Associates in Princeton, New Jersey.

“Money market brokerage accounts normally pay larger charges than money market or financial savings accounts at banks,” he stated in an emailed assertion. “If the Fed is certainly trying to scale back charges 5 occasions over the following eighteen months (as at present projected), then the chance to earn 5% yearly on these money investments could not final for much longer.”

3. Put off massive purchases

If you are planning a main buy, like a residence or automobile, then it might pay to wait, since decrease rates of interest may scale back the fee of financing down the street.

“Timing your buy to coincide with decrease charges can save money over the life of the mortgage,” Tayne stated.

Although mortgage charges are fastened and tied to Treasury yields and the financial system, they’ve already began to come down from latest highs, largely due to the prospect of a Fed-induced financial slowdown. The common rate for a 30-year, fixed-rate mortgage is now simply above 7%, in accordance to Bankrate.

However, decrease mortgage charges may additionally increase home-buying demand, which might push costs larger, McBride stated. “If decrease mortgage charges lead to a surge in costs, that is going to offset the affordability profit for would-be patrons.”

When it comes to auto loans, there isn’t any query inflation has hit financing prices — and car costs — onerous. The common rate on a five-year new automobile mortgage is now practically 8%, in accordance to Bankrate.

But on this case, “the financing is one variable, and it is frankly one of the smaller variables,” McBride stated. For instance, a quarter-percentage level discount in charges on a $35,000, five-year mortgage is $4 a month, he calculated.

In this case, and in lots of different conditions as properly, shoppers would profit extra from bettering their credit score scores, which may pave the way in which to even higher mortgage phrases, McBride stated.

Subscribe to CNBC on YouTube.

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator