Electronic banking on the rise | Australian Broker News

News

Digital banking on the increase

Digital banking interactions surge in 2024

Australians are main a digital revolution, embracing technological progress in banking at unparalleled expenses, in accordance with a brand new report commissioned by the Australian Banking Affiliation (ABA) and equipped by Accenture.

“Customers are persevering with to shift to handy digital banking channels,” ABA CEO Anna Bligh (pictured earlier talked about) said.

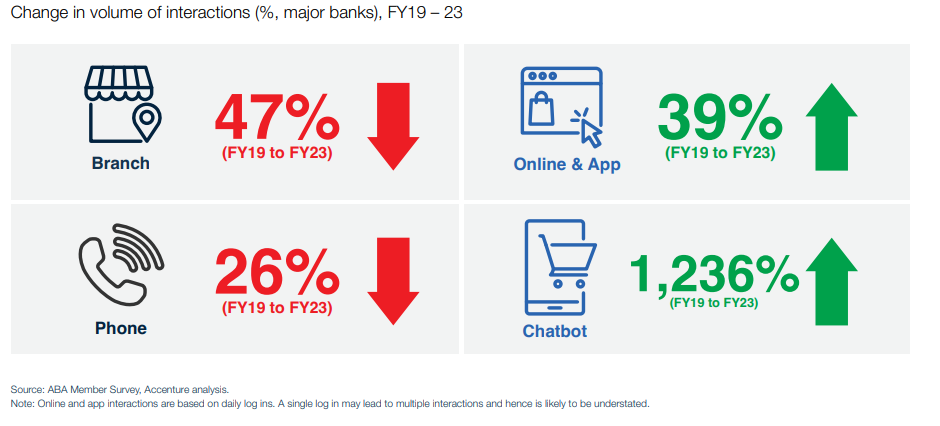

In between 2019 and 2023, banking interactions grew by 37%, pushed by increasing on the web and utility use.

Rise of digital funds

Electronic funds have surged, with principal financial institution prospects constructing $126 billion in funds by way of mobile wallets in the final 12 months—a 35% improve from the earlier 12 months.

For the initially time, mobile pockets funds have overtaken general ATM cash withdrawals.

“The booming digital financial system presents quite a few prospects, however it doesn’t happen with out the want of threats,” Bligh claimed.

Advancement in digital interactions

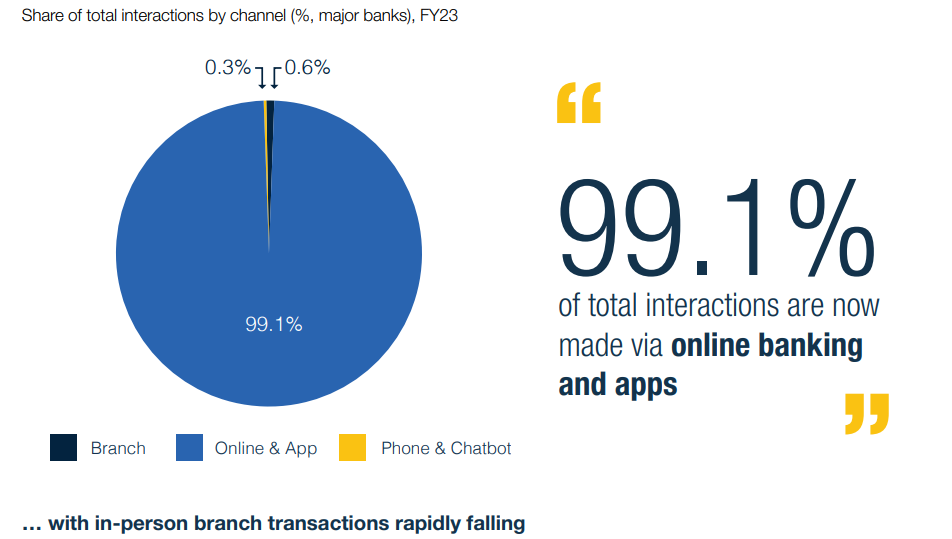

Digital banking interactions now account for in extra of 99% of all buyer interactions, with a 37% development on condition that 2019.

“Australians are interacting with banking establishments much more than at any time forward of,” Bligh mentioned.

Addressing hazards and ripoffs

Banks are proactively preserving prospects from cons by interventions comparable to the National Anti-Scam Centre and steps to limit transactions to substantial-chance cryptocurrency exchanges.

Month-to-month rip-off losses are trending downwards, demonstrating the success of those steps.

“The digital revolution has enhanced choices for ripoffs, however govt and monetary establishment interventions have noticed a reversal of the upwards growth,” Bligh talked about.

Economic resilience and enterprise lending

Irrespective of elevated curiosity costs, Australia’s financial system exhibits resilience.

Overall skilled lending grew by 6.5% amongst April 2023 and 2024, with smaller and medium companies accounting for 50 % of the full small enterprise lending.

Lending to the development area consists of 33% of enterprise lending.

Addressing financial commitments

Even with greater house finance mortgage repayments, further than 98% of mortgage mortgage holders maintain on to spend on time. Nonetheless, 1 in 20 properties report problems convention payments.

“Banks proceed to be alert as some women and men find it troublesome to take care of up with their monetary commitments,” Bligh said.

Supporting buyers in hardship

Most Australians deal with to fulfill their charges no matter economical pressures. Nonetheless, monetary establishments are fully able to help these experiencing points, with better hardship help in early 2024.

“Banks will proceed to speculate the place their customers will want them,” Bligh reported.

Branch density and alternate choices

Australia maintains a better department density in comparison with worldwide buddies, with 19 financial institution branches for every 100,000 grownups. For regional buyers, Lender@Post presents above 3,400 encounter-to-confront banking accessibility factors.

Consumer Data Proper (CDR) adoption

Even with substantial investments, uptake of the Buyer Knowledge Suitable continues to be decrease, with a lot lower than 1% of shoppers sharing their knowledge.

“Government and enterprise have designed main investments in CDR,” Bligh claimed.

Decrease in cash and cheque use

Hard money use has declined considerably, with a ~10% 12 months-on-yr discount as a result of 2007. Cheque utilization has additionally fallen, with a 37% drop in the vary of cheques drawn in the final calendar 12 months.

“The use of revenue for real transactions is predicted to maintain on to say no,” Bligh reported.

Get the hottest and freshest house mortgage information shipped superb into your inbox. Subscribe now to our FREE day-to-day publication.

Related Tales

Preserve up with the most present information and actions

Be a part of our mailing checklist, it’s no value!