Will Florida House loan Premiums Go Down In May probably?

Florida mortgage premiums in May 2024 are predicted to remain near newest levels or see a slight lower. Financial data, particularly inflation critiques, will influence how lots expenses switch, and the Federal Reserve’s actions could maybe additionally take part in a task.

Wanting forward to May probably, most trade specialists imagine that home loan expenses in Florida is not going to go down considerably. They think about the charges will proceed to be near the higher 6% vary.

This is as a result of truth the Federal Reserve is remaining fairly watchful about decreasing prices owing to ongoing excessive inflation, which impacts prices for points we buy.

Any variations in house finance loan charges subsequent month will most likely rely on new data and info about inflation and work. If these stories present inflation is nonetheless important or way more folks right this moment are having work alternatives, property finance loan expenses would possibly proceed to be the very same or enhance a bit.

Typically, we must always not rely on large drops in property finance loan charges any time shortly.

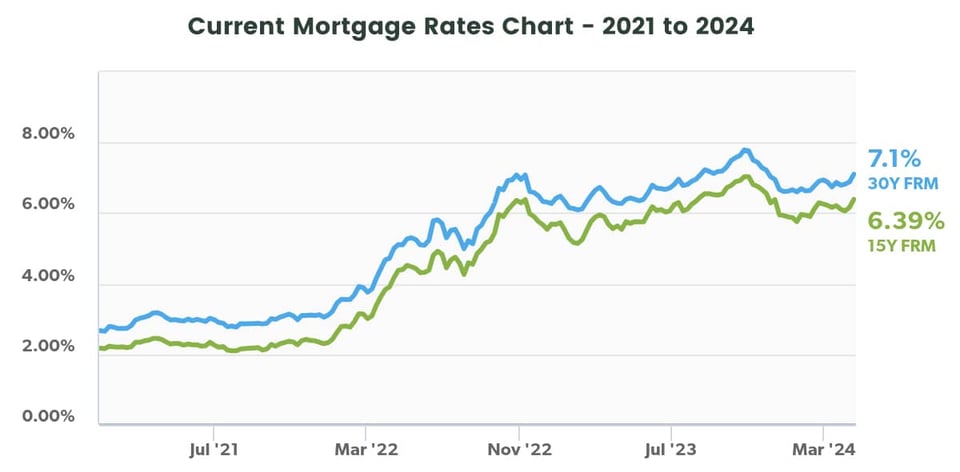

Chart signifies U.S. weekly abnormal house finance loan premiums for 2021-24 as of April 18, 2024.

Information Resource from Freddie Mac’s Key House loan Marketplace Survey®.

2024 Florida Desire Level Forecast

Underneath, we forecast the probably house finance loan charges for every remaining thirty day interval in 2024. Professionals at MakeFloridaYourHome utilised information from the federal mortgage loan company Freddie Mac to make our projection.

Month

Projected Curiosity Fee (%)

Could 2024

7.13

June 2024

7.16

July 2024

7.20

August 2024

7.24

September 2024

7.28

Oct 2024

7.31

November 2024

7.35

December 2024

7.39

Right listed here are some essential insights from analyzing this data:

Consistent Growing Craze

Starting up from a decrease level in April 2023 with prices at 6.34%, house loan expenses have continuously improved, attaining 7.62% in Oct 2023.

The charges for the comfort of 2024 are anticipated to maintain rising every particular person month, hitting 7.39% by December. This demonstrates a continuing increase above 20 months, pointing to rising costs for debtors.

Stabilization Higher than 7%

Right after some ups and downs in early 2023, house loan expenses have stayed larger than 7% contemplating that August 2023 and are anticipated to proceed to be over this degree all via 2024.

This implies that the scale back prices in the beginning out of 2023 could probably not return shortly.

Gradual Raise Predicted

The premiums forecasted for 2024 show a modest and regular rise nearly each thirty day interval, from about .03% to .04%.

This gradual and common climb signifies a safe monetary environment. It presents women and men trying to get properties a definite technique of what to rely on and assists them put together their funds improved.

The Ideal Loan Varieties For a Higher-Fascination Amount Ecosystem

In a higher-interest-rate environment, choosing the suitable type of monetary loan is crucial to dealing with charges correctly. Here are a number of the best financial institution loan types to ponder:

Fastened-Fee Mortgages

This type of monetary loan locks within the curiosity worth for the entire time period of the house finance loan, which might be 15, 20, or 30 a few years. Opting for a set-amount mortgage loan in a higher-fascination worth setting might be useful because it safeguards you from long term quantity will improve.

Though the unique fee could probably be larger, it presents safety and predictability in your funds, and you may refinance on the time charges go down.

FHA Financial loans

The Federal Housing Administration insures these monetary loans and usually offers lower charges than commonplace monetary loans. They additionally demand a decreased down fee and are further accessible to debtors with decrease credit score rating scores.

In a significant-curiosity-amount setting, an FHA loan could make homeownership further attainable.

VA Loans

VA loans are an distinctive risk if you’re a veteran or lively army member. Backed by the Department of Veterans Affairs, they provide aggressive prices and don’t name for a down fee or private mortgage insurance coverage insurance policies (PMI).

This can considerably scale back the month-to-month worth, even in a higher-interest-rate environment.

USDA Financial loans

Aimed at patrons in rural areas, USDA monetary loans current small-interest prices and no down fee necessity, making them an lovely choice for certified debtors in designated rural locations.

Selecting the proper mortgage selection is significant for controlling your mortgage prices proficiently, specifically in a tricky monetary climate.

Best 5 Grants for Florida Homebuyers

Florida homebuyer grants may help offset bills in a superior-fascination-amount setting, creating it much more reasonably priced to amass a property.

Below are the prime 5 grants accessible for very first-time homebuyers in Florida as of 2024, every particular person offering sizeable financial help for down funds and shutting bills.

Florida Hometown Heroes Method

Offers as much as $35,000 for down funds and shutting charges.

Specifically created for professionals serving their regional communities.

No common mortgage loan insurance coverage plan is demanded for FHA monetary loans.

Miami-Dade Advocacy Believe in Grant

Gives as much as $28,500 as a forgivable private loan following 20 a number of years.

Demands candidates to guide their cash.

Must protected a mortgage loan via an authorised loan supplier in Miami-Dade County.

Hallandale Seaside Neighborhood Grant

Assists with as much as $100,000 for down fee and shutting expenses.

Supplied as a no-desire private loan, forgivable proper after ten a few years if the belongings stays the primary house.

Available fully to inhabitants of Hallandale Beach.

Own a Dwelling Opportunity Grant Software

Extends as much as 5% of the entire financial institution loan amount to be used in path of down fee or closing expenses.

Requires a minimal credit standing of 640.

Out there throughout many Florida counties.

Dare to Very personal the Aspiration

Delivers as much as $40,000 in Tampa for down fee and shutting expenditures.

Shipped as a deferred-payment loan, completely forgiven instantly after 10 a number of years.

Aimed to help homebuyers in Tampa.

Florida Home finance loan Amount Forecast FAQ

Here is a guidebook to generally requested inquiries about home loan expenses, solely tailored for Florida inhabitants looking out to grasp the neighborhood market developments:

What are the current typical house loan premiums in Florida?

As of mid-April 2024, the abnormal payment for a 30-yr fastened-rate home loan in Florida is 7.1%, though the 15-year fixed-amount typical is 6.39%.

Will house loan prices in Florida scale back in May probably 2024?

Whilst home loan prices have been unstable, the present monetary indicators and professional predictions advise that prices in Florida are potential to stay steady or sensible expertise solely small fluctuations in May probably 2024.

Are mortgage expenses anticipated to extend all via 2024 in Florida?

Provided the latest tendencies and financial parts, these sorts of as ongoing inflation and a sturdy job market place, mortgage loan charges in Florida would possibly proceed to see upward rigidity by 2024 until in fact appreciable monetary shifts occur.

What issues are driving the current property finance loan prices in Florida?

Quite a lot of points influence current mortgage prices in Florida, which embody Federal Reserve insurance coverage insurance policies, inflation concentrations, and over-all financial issues, these kinds of as the duty market and purchaser spending.

How do property finance loan charges change by monetary loan type in Florida?

In Florida, home loan prices can change noticeably primarily based on the kind of mortgage. For working example, VA loans generally give decreased costs attributable to governing administration backing, whereas jumbo monetary loans could have higher prices due to to the improved hazard linked with bigger sized private loan portions.

What ought to Florida folks take a look at when figuring out to lock in a home loan payment?

Florida inhabitants selecting when to lock in a mortgage worth actually ought to ponder their financial circumstance, market tendencies, and personalised menace tolerance. It is de facto usually a good suggestion to lock in a worth when you could have a purchase order association and have in comparison fairly just a few loan supplier options.

Is now a implausible time to refinance a house finance loan in Florida?

Refinancing might benefit Florida house owners if they’ll protected a decreased quantity than their present-day mortgage, which might information to appreciable financial savings on month to month funds and total want charges.

What is the bottom mortgage loan fee at any time recorded in Florida?

While distinctive state paperwork could probably range, the least costly recorded 30-calendar yr mortgage loan quantity nationally was 2.65%, reflecting historic lows in Florida, in accordance to Freddie Mac.

Should Florida residents refinance if costs drop by 1%?

For Florida house owners, refinancing for a 1% decrease in your house loan worth might be worthwhile, because it generally success in substantial month to month and lengthy-term private financial savings however makes certain the closing expenses don’t outweigh the constructive points.

How can Florida residents get the best house finance loan cost?

To protected the perfect house loan degree, Florida residents should assess provides from many lenders, think about numerous private loan varieties primarily based totally on their fiscal circumstance, and enhance their credit standing score and down fee to qualify for essentially the most reasonably priced charges doable.

Get Help Locating The Most reasonably priced Price

Getting the suitable house loan in a high-interest environment can appear to be overpowering, however you you shouldn’t must cope with it by itself.

At MakeFloridaYourHome, our regional specialists are dedicated to aiding you get the most affordable possible property finance loan prices. We additionally guideline you by way of the quite a few grants on the market in Florida for which you may probably qualify.

Whether or not paying on your 1st family or looking to make a change, we’re on this article that can assist you make the best fiscal selections.