Winter lull hits home listings | Australian Broker News

News

Winter lull hits home listings

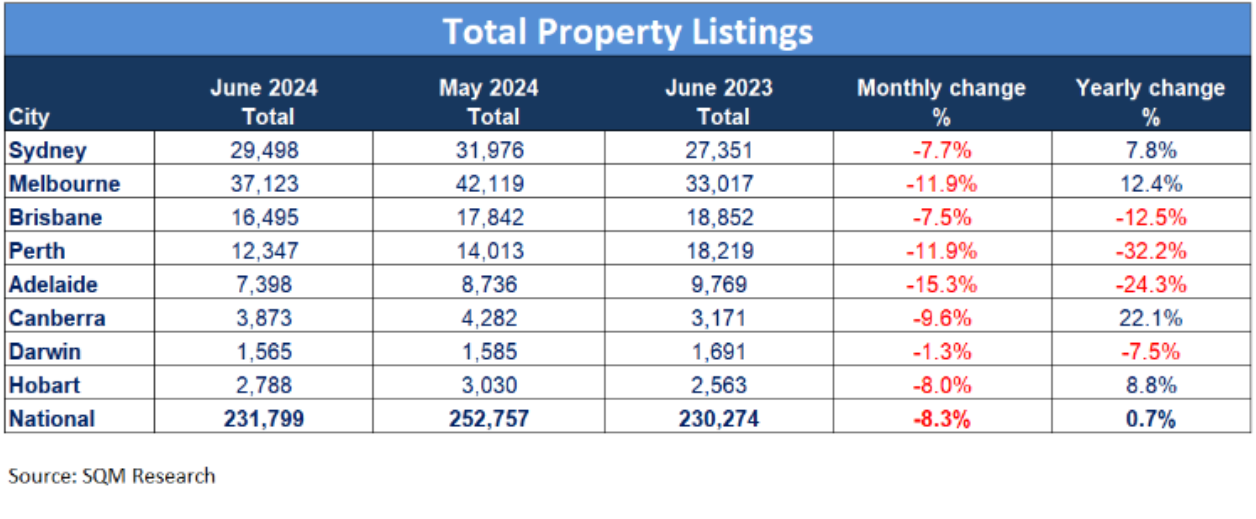

Total listings plummet in June

SQM Research reported a notable 8.3% drop in nationwide residential property listings in June, with the full reducing to 231,799 from 252,757 in May.

Adelaide noticed the biggest drop at 15.4%, adopted by Melbourne and Perth at 11.9%.

Darwin had the smallest decline at 1.3%.

Over the 12 months, complete listings elevated by 0.7%, with Sydney and Melbourne seeing rises, however Adelaide and Perth experiencing vital drops.

See LinkedIn publish right here.

See LinkedIn publish right here.

New and outdated listings decline

New property listings (lower than 30 days) fell by 13.3% in June, totaling 65,190 properties. Compared to June 2023, there was a 3.1% improve.

Sydney, Melbourne, Brisbane, and Canberra confirmed annual will increase, whereas Perth, Adelaide, and Darwin noticed declines. Hobart had probably the most vital annual progress at 25.5%.

Older property listings (over 180 days) decreased by 6.6% in June, with notable reductions in Brisbane, Canberra, and Sydney.

Perth confirmed a dramatic 58.1% annual lower. Despite these drops, there was a slight 3.5% improve in older listings nationwide over the previous 12 months, with vital rises in Hobart, Canberra, and Darwin.

Distressed listings rise

Distressed property listings in Australia barely elevated to five,111 in June, marking a 0.2% rise from the earlier month.

NSW noticed a lower, whereas Victoria, SA, and NT recorded will increase.

Annually, NSW and Victoria had vital will increase, whereas Queensland, WA, and SA noticed declines.

“This is the usual winter lull impact we see within the Australian housing market right now of 12 months so no nice shock in these numbers,” stated Louis Christopher (pictured above), managing director of SQM Research.

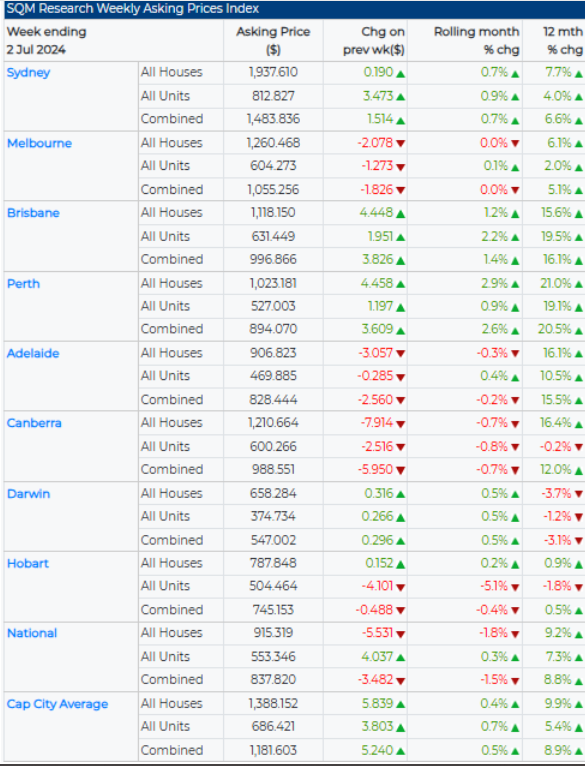

Asking costs fluctuate

The nationwide mixed dwelling asking worth fell by 1.5%, recording a median of $837,820, in keeping with SQM Research. However, capital cities noticed a 0.5% improve.

Brisbane and Perth skilled vital month-to-month will increase, whereas Darwin and Hobart noticed declines or stability.

Canberra recorded a sturdy annual rise of 13.0%.

“While the housing market could also be slowing in Sydney and Melbourne, the identical can’t be stated for these three cities,” Christopher stated.

Get the most popular and freshest mortgage information delivered proper into your inbox. Subscribe now to our FREE every day publication.

Related Stories

Keep up with the newest information and occasions

Join our mailing listing, it’s free!

Rider College in New Jersey requested bondholders to approve supplemental borrowing to fund a cash turnaround plan.

Rider College in New Jersey requested bondholders to approve supplemental borrowing to fund a cash turnaround plan.