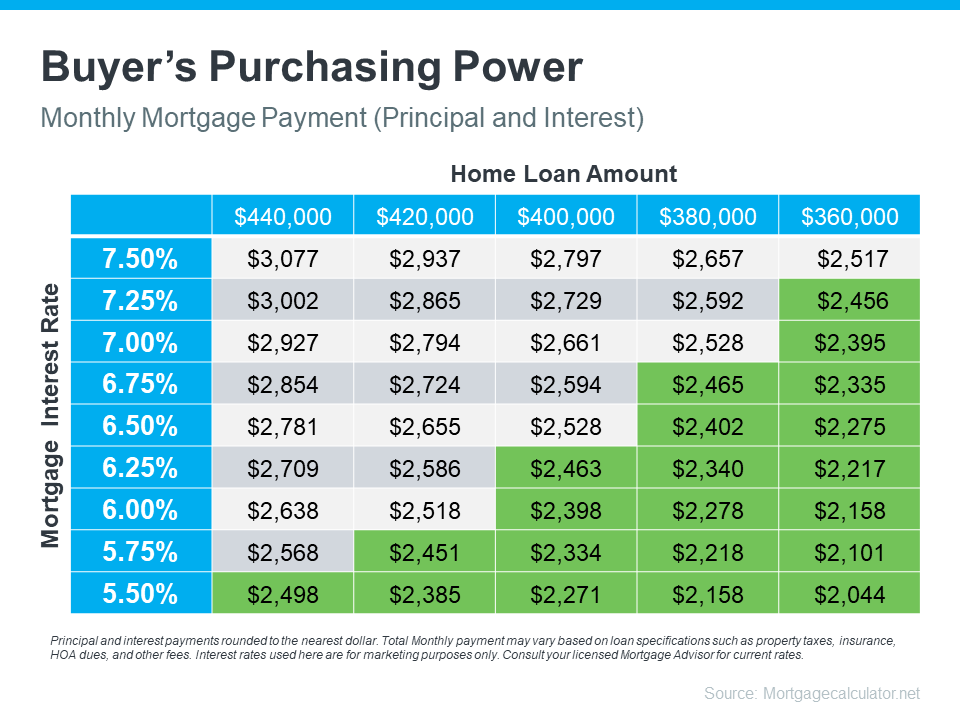

Knowing the impression of property finance loan charges in your household-acquiring energy is necessary, particularly if you happen to could be considering a partnership with Evergreen Home Financial loans. Recently, the premiums for 30-yr fastened mortgages have discovered a serious reduce. This lower is a constructive sign for alternative homebuyers.

This sample incorporates a breath of contemporary air for customers. As a contemporary Bankrate article highlights, this drop in costs fairly eases the housing affordability squeeze. Further extra emphasizing this stage, Edward Seiler, AVP of Housing Economics and Govt Director of the Analysis Institute for Housing The usa on the House loan Bankers Affiliation, notes that the MBA anticipates continued enchancment in affordability problems as mortgage charges drop.

The Impression of Home finance loan Charges on Your Dwelling Search

Greedy how mortgage loan costs have an effect in your month-to-month dwelling cost is important in your journey in course of homeownership. For event, in case your value vary is within the $2,400 to $2,500 common cost selection, even slight value fluctuations can considerably impression your spending plan and the mortgage quantity you possibly can pay for.

Seek Guidance from Evergreen Residence Loans Specialists

When considering a dwelling acquire, it is important to hunt the recommendation of with skilled specialists. At Evergreen House Financial loans, our group is totally able to tutorial you thru a number of home loan prospects, serving to you totally grasp the variables influencing home loan premiums and the way these fluctuations results your paying for electrical energy.

By analyzing current particulars and altering your methodology to align with current day premiums, you could be improved equipped and confident in your homebuying journey.

For these making ready to get a home, the current downward improvement in property finance loan costs is encouraging information. Companion with Evergreen Residence Loans, and let’s strategically program your subsequent strategies within the homebuying course of. Speak to your native Evergreen Loan Officer for a completely free seek the advice of with today!

Propertyology reveals Australia’s biggest belongings sector | Australian Broker News

News

Propertyology reveals Australia’s absolute best residence market

Shock market chief

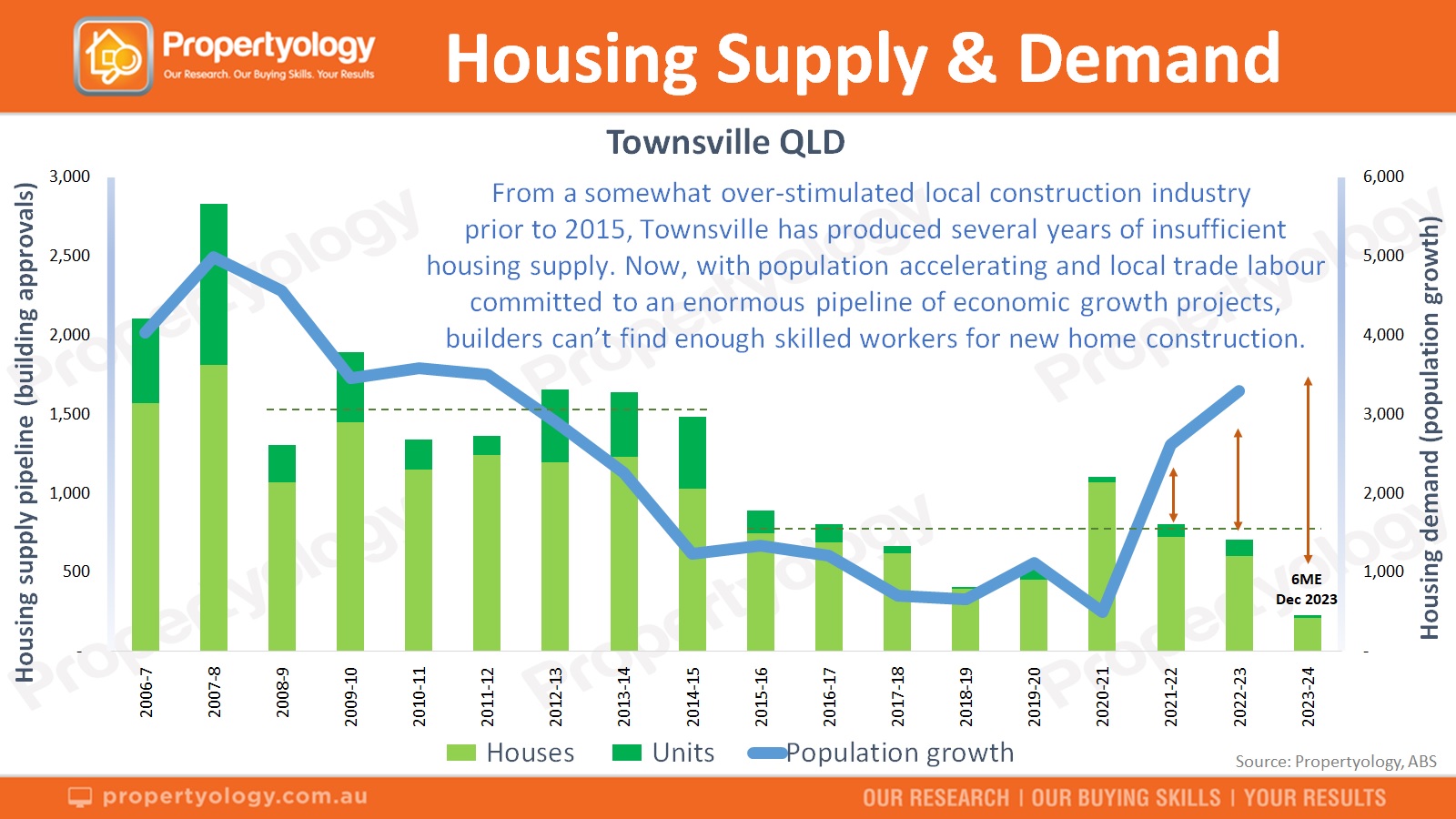

Australia’s perfect residence market place can be Townsville, predicted Simon Pressley (pictured earlier talked about), Propertyology’s head of analysis.

Townsville: Exceptional efficiency envisioned

After analysing necessary metrics for property markets in further than 400 Australian cities and cities, Propertyology ranked Townsville’s capital enlargement stage potential as the very best in Australia for the next three a very long time.

Remarkable progress projections

Propertyology duties that true property values in Townsville will enhance by someplace round 50% in extra of the just a few a very long time ending in 2026.

“Existing homeowners in Townsville now have a wonderful platform to reinforce to a nicer and even bigger property,” Pressley reported. “There will completely on no account be a much more economical chance for to start out with-home clients to get their first foot on the belongings ladder.”

Economic progress drives development

Townsville has witnessed a 21.5% maximize in careers over the earlier 5 years, considerably exceeding the nationwide typical of 11.8% and Sydney’s 5.6%.

With $12 billion actually price of dedicated duties, Townsville options an unparalleled pipeline of key initiatives.

“No locale in Australia’s funds city or regional township has a extra wonderful pipeline of main jobs than the northern cash of this nation,” Pressley defined.

Army and migration have an effect on

An influx of internal migrants, which embody 500 army companies personnel and their households relocating to Townsville in 2025, will further increase the housing market.

“A myriad of labor prospects, housing affordability, and necessary monetary dedication in life-style facilities make Townsville a first-rate desired vacation spot,” Pressley defined.

Tight housing industry

The present-day present of properties in Townsville is by now 40% decrease than 5 yrs again.

“Three important housing supply metrics affirm Townsville’s property sector to now be as restricted as a mouse in a matchbox,” Pressley reported.

Analysis shows that Townsville’s housing design pipeline is lagging driving want, indicating potential for even elevated upcoming shortages.

Financial and way of life selection

Townsville’s economic system is strong and diverse, with vital sectors together with nicely being, education, producing, agriculture, renewable vitality, treasured metals, and tourism.

The metropolis’s amenities and life-style choices, this sort of because the picturesque Strand and a $300m environment-course sports activities actions stadium, have reworked Townsville into an stunning locale for residents and travellers alike, Propertyology documented.

“The newest investments in lifestyle and liveability, mixed with Townsville’s newest media family promoting worth of $450,000, are explicit to enchantment to the discover of the rising amount of Australians who relocate absent from large, congested, excessive priced cities,” Pressley reported.

To browse the Propertyology examination in complete, which incorporates the file of great jobs in Townsville, click on on proper right here.

Get the most well liked and freshest home finance mortgage data delivered correct into your inbox. Subscribe now to our FREE day-after-day e-newsletter.

Today noticed the common customary 30yr set price rise ever so a bit for prime tier eventualities. Most lenders are however quoting these individuals eventualities just under 7%. Based on the distinctive information of any provided circumstance, charges array from the mid 6’s all the best way up to the mid 7’s.

Unlike each single of the sooner two days, there weren’t any main flashpoints for the bonds that underlie property finance loan value motion at present. There have been being a number of monetary tales, however neither had a big effect on the trade. All in all: a fairly serene and boring working day–particularly in contrast to virtually another working day provided that previous Friday.

From beneath, the sector will wait round for the next large ticket monetary report: Tuesday’s Retail Income. There are a smattering of different research subsequent week, punctuated by a trip closure on Wednesday for Juneteenth. The main, most sizeable movement possible even now depends upon the monetary research that we simply noticed and isn’t going to see as soon as extra for nearly a thirty day interval. It would not be a shock to see a additional sideways, barely uneven growth involving from time to time.

West One Financial loans has employed Helen Merrey as regional account supervisor.

Merrey joins with 25 a long time of encounter in fiscal companies and earlier labored as an organization progress supervisor (BDM) for Scottish Creating Modern society.

Just earlier than this, she held comparable roles at Furness Making Culture, Leeds Creating Society and Virgin Revenue.

In her new job, Merrey will look instantly after the North East, Yorkshire and Scotland. Just one among her duties can be to develop the lender’s presence in Scotland following its begin into the place in March.

The loan supplier has additionally promoted Kayleigh Tuvey, beforehand a phone BDM for get-to-enable (BTL) and bridging, to the a part of cellphone firm development gross sales supervisor for family.

The lender states it choices to announce quite a few different hires and standards modifications by way of the following 50 % of the 12 months.

West Just one Financial loans head of middleman revenue and distribution Paul Huxter says: “Helen has a wealth of working expertise within the middleman present market and is a person who has the strategies and id to make a genuine large distinction to our firm appropriate from the off. So, we’re delighted to have her on board.”

“I’m additionally thrilled for Kayleigh, who has demonstrated that she has the know-how, willpower and expertise to make the section as much as internal earnings supervisor. I’ve no query she can be distinctive in her new objective.”

The Monetary Perform Authority has pushed again the publication of its overview into the therapy methodology of politically uncovered individuals till lastly after the usual election.

The outcomes from the analysis ended up as a result of of to be launched in keeping with the end of June deadline in accordance with the Money Companies and Marketplaces Act.

But this is able to have seem forward of the 4 July nationwide ballot.

Having stated that, the FCA claims it could not be “acceptable” to publish the consider within the pre-election interval of time and can now be posted afterwards in July when Parliament has returned.

The critique was launched final calendar yr subsequent a row between populist ideal-wing politician (now chief of the Reform celebration) Nigel Farage and NatWest’s Coutts arm across the closure of his account by the loan firm.

The aftermath of the affair led to the resignation of NatWest important authorities Alison Rose earlier July, then essentially the most spectacular feminine in Uk banking, quickly after she admitted speaking about Farage’s relationship with the monetary establishment to the media.

NatWest confirmed Paul Thwaite as its up coming full-time important govt in February.

Mortgage costs moved modestly elevated to start the brand new 7 days. With the frequent prime tier 30yr set charge just under 7% on Friday, this meant a shift to simply above 7% now.

As all the time, proceed to hold in mind {that a} property finance loan stage index is best used to seize the working day to day motion in charges as opposed to outright ranges. The latter can vary drastically relying on credit standing ranking, equity, occupancy, low price factors, and loan supplier margins.

There weren’t any intriguing or persuasive developments driving at present’s bond market motion (bonds dictate mortgage price momentum). It was an uninspired, uninteresting Monday with none substantial monetary data or bond trade quantity.

Issues have to be extra fascinating tomorrow, for larger and even worse, thanks to the launch of the Retail Income information at 8:30am ET. When this is not actually in the exact same league because the work report or the Purchaser Cost Index, when Retail Income happen in significantly higher or decreased than forecast, there’s typically a obvious response in costs.

Just Home loans has promoted Gareth Lowndes to product sales director for shopper options.

Lowndes’ new job will see him set up the buyer suppliers reserving workers and interact with advisers all through the enterprise, checking enterprise gross sales targets and driving equally revenue and safety income growth.

He can even help recruit, set up and preserve advisers together with guaranteeing regulatory duties and best strategies are adhered to.

Centered in South Wales, Lowndes joined the Just Home loans group in 2011 working in several roles together with mortgage loan and protection adviser, to divisional revenue director and on to fiscal options director.

Commenting on his appointment Lowndes says: “I’m fairly enthusiastic to be taking over this new perform and to be a part of the yr on yr progress in Just Mortgages.

Just Home loans and Spicerhaart chief govt officer John Phillips gives: “With his experience, know-how and dealing expertise, Gareth is the proper particular person for the work to guarantee we’re maximising every alternative, discovering the correct expertise and often providing that five-star service.”

Audrey Melicine, 39, signed as much as our cash train programme Sofa to £5k to find how to make enhancements to her placement and use her £4,000 value savings to get began creating a residence deposit. She is conscious that she calls for to deal with the impulse paying out related to her consciousness deficit hyperactivity ailment (ADHD) if she is to fulfil her aspiration of buying her very personal home.

The data analytics director, who’s a higher stage taxpayer, says: “Despite persistently having pay rises across the previous 8 a number of years I have the same issues. Even if I earned £100,000 I consider I’d proceed to battle.”

Investigate means that neurodiverse people are extra in all probability to be in personal debt than neurotypical individuals and sense considerably much less assured about operating their income.

“My triggers are boredom,” she admits. “I want a entire lot of stimulation. So when I proceed to be residence I proceed to commit.”

In this put up, we handle:

Read way more: A tutorial to purchasing your 1st dwelling

What may she do?

Audrey lives by itself, has a automobile and a doggy, so her dwelling prices are important: her lease by itself is £1,500 a thirty day interval.

Other prices these kinds of as council tax, automobile insurance coverage plan and broadband are already getting minimised: Audrey statements the 25% solitary man or lady discounted for her council tax, for illustration, drives with a black field to ensure she is receiving the most effective protection attainable and not too long ago haggled down her web bills following her deal was set to double.

On paper, instantly in any case her outgoings, and permitting for a social lifetime, Audrey may make it easier to save about £1,000 a thirty day interval. So there isn’t a getting away from how her impulse paying out is draining her account. “Eating out and takeaways are costing me £500 a thirty day interval,” she admits.

Audrey skilled now began off implementing some methods to assist and he or she has managed that can assist you save simply above £3,000 in a few months: “I now put my items into the Amazon cart after which go away them for a couple occasions, chopping my spending from £500 to £200 this manner. And I made friction by taking away my card particulars from JustEat and Deliveroo – it undoubtedly labored.”

Consider our 20 money saving suggestions you need to use each day.

How does ADHD influences individuals’s investing routines?

To take into account issues extra, Funmi Olufunwa, founder of cash training provider Hoops Finance, suggests Audrey ought to actually objective to remove as considerably determination-making from her day-to-day existence as achievable.

“Planning is genuinely robust for Audrey owing to her ADHD: she may be hyper-concentrated however then battle to focus. The commonplace methods like batch cooking to protect cash on meals, for example, are usually not so possible to perform for her.”

Audrey agrees. “If I have a prolonged working working day I overlook lunch just because sometimes I am within the zone, so halting to cook dinner is tough and unrealistic – which is when I purchase takeaway a lot later when I’m immediately ravenous.”

Funmi suggests Audrey adhere to the very same elements she likes to eat for breakfast and lunch, and as a end result remove some choice-creating about meals.

She additionally signifies Audrey seems to be like at her shelling out calls for for lesser segments of time: so the week prematurely somewhat than the thirty day interval forward. “Again, this can prohibit decision-earning and suggest paying considerably much less time on it as an exercise,” clarifies Funmi.

Audrey has requested a buddy to examine in with her on a common foundation and provides her pep talks if wanted: “I will have to be accountable as to how I’m conserving.”

What she’ll do: how may a Life span Isa help?

As Audrey is hoping to acquire her preliminary property, a Lifetime Isa can help her do that.

Anyone lower than 40 can open the tax-free of cost savings services or products, make it easier to save as much as £4,000 nearly each tax 12 months and purchase a 25% reward – as much as £1,000 – from the authorities. This can go in the direction of a deposit in your initially dwelling, as prolonged because the property bills £450,000 or a lot much less.

Audrey necessities to promptly open an account with Moneybox as her fortieth birthday is approaching. “I wish to have greater than sufficient value savings by the conclude of the tax 12 months on April 5 so as to add the best £4,000 in order that I receive the whole federal authorities reward. I’ll then promptly begin preserving my upcoming £4,000.”

Audrey has noticed houses on-line that attractiveness to her and value about £350,000. A ten% deposit means she would might want to protect £35,000. It would purchase her shut to a few a long time if she will save £10,000 to £12,000 a yr.

Following chatting to Funmi, she thinks she may should have a four- or five-year put together of conserving about £1,000 a month. “Possibly way more if I enhance my wage – which might signify as much as £60,000 in full: £50,000 for a deposit and £10,000 for related prices.”

See our easiest Lifetime Isas for a property deposit or pension

What is the £1,000 investing allowance?

All individuals has a buying and selling allowance of £1,000 so if Audrey sells factors she no prolonged necessities in the midst of the 12 months on eBay, Depop and Vinted she may make £1,000 tax-totally free.

“I had by no means listened to of this previous to however I have so quite a few clothes I may present,” she claims.

Examine extra: What is one of the best ways to offer my issues? Like how to advertise on eBay, Facebook Market, Depop, Vinted, Gumtree and Etsy

(*39*) conserving for Audrey: £10,000

Where did the personal savings arrive from?

Tackling paying out on takeaways and taking in out = will save £3,000 a yr

Place the £4,000 she now has into a Lisa simply earlier than April 5 = to get the £1,000 authorities bonus

Preserve a further £4,000 quickly after April to extend to the Lisa = £5,000 which incorporates federal authorities reward

Sell undesirable possessions = £1,000

Final phrase from Audrey’s expert adviser Funmi Olufunwa

“Audrey can eliminate the anxiousness she has throughout money by scheduling for modest segments of time, regardless of if which is meals stuff arranging or budgeting for evenings out.

“The Life span Isa is these a glorious thought – as prolonged as she is real looking with her personal savings targets as a substitute than sticking rigidly to set targets. Permit for these events when you’ve got a great deal of weddings or social gatherings.”

Go by way of further: “I’ve nonetheless left London however I’m even now struggling to acquire a home.”

Important information

Some of the merchandise promoted are from our affiliate associates from whom we obtain fee. When we objective to side among the most interesting options available, we can’t evaluation nearly each services or products on the present market.

Giving your home a makeover may be costly, which could make you wonder if it’s price borrowing cash to cowl the prices.

Many owners remortgage to fund home enhancements as a result of the rates of interest have a tendency to be decrease than on private loans or bank cards. But is that this the precise method for you?

In this text we clarify:

Read extra: Remortgaging: the whole lot you want to know

Is it a good suggestion to remortgage for home enhancements?

When you remortgage, you repay your outdated mortgage by taking out a brand new one on the identical property.

There are quite a few the reason why owners may do that. You might want to change to a less expensive rate of interest or to achieve the flexibleness to overpay the mortgage and scale back your debt.

But one more reason is to borrow more cash to fund large home enhancements.

In the primary eight months of 2021, the variety of remortgage purposes from DIY-mad property homeowners soared by 174% in contrast to the identical interval in 2019 earlier than the pandemic, in accordance to dealer Mojo Mortgages.

Meanwhile, the typical quantity launched by owners for financing home renovations has elevated from a mean of £52,000 to simply over £65,000.

However, there’s tons to take into considerationearlier than deciding to apply for a brand new mortgage to perform renovations.

There are numerous elements that may have a bearing in your capability to refinance your property. These embrace:

The worth of your home

The measurement of your mortgage

Your compensation historical past

The extent of the renovation work

We have extra data in our information on remortgaging.

What to contemplate earlier than remortgaging to fund home enhancements

Here’s what you need to contemplate:

1. Your monetary scenario

Regardless of whether or not you’re looking to change to a brand new cope with your current lender or to transfer to one other financial institution, your monetary scenario can be reassessed.

Lenders will take a look at your earnings, employment standing, job safety, money owed and credit score historical past earlier than deciding whether or not to allow you to remortgage.

Borrowing more cash could be a large monetary dedication so even when you can afford to do that, be sure you take into consideration the influence on the remainder of your funds.

2. Your fee historical past in your current mortgage

If you’ve a observe report of late or missed funds, it might effectively lead to most lenders turning you down.

Lenders that do settle for debtors who’ve had mortgage fee points cost larger rates of interest.

If you don’t have a squeaky clear credit score report then you may want to attempt to rectify that earlier than borrowing more cash. We clarify how to do that in our information on credit score scores.

3. Affordability

If you improve your mortgage mortgage, your month-to-month funds are seemingly to rise.

Before agreeing to a remortgage in these circumstances, the lender will test your wage is excessive sufficient to afford the brand new funds after your different outgoings have been deducted.

Most lenders will enable you to borrow 4.5 instances your wage.

Consider your earnings and whether or not it’s seemingly you’ll find a way to borrow extra.

4. The scale of the renovation

To remortgage most lenders count on your home to be watertight and weather-proof with a working kitchen and toilet. In different phrases: they need your home to be liveable.

If you might be planning a demolish and rebuild undertaking, you will have to use specialist finance generally known as a bridging mortgage or get a specialist renovation mortgages. But keep in mind that the rates of interest on these two sorts of mortgage are seemingly to be larger than a run-of-the-mill mortgage.

5. Timing

Should I remortgage earlier than or after the home enchancment work? Most owners want to remortgageto perform homerepairs. This is in order that they’ll launch sufficient cash to pay for the work.

But if in case you have sufficient saved up, paying for your home enhancements upfront and remortgaging afterwards may work to your benefit. An increase in your property’s worth could effectively offer you entry to a less expensive rate of interest.

But remortgaging to renovate can generally be a nasty concept if in case you have to go away your present deal earlier than it expires.

This is since you could possibly be liable for an early-repayment cost, which may be between 1% and 5% of your excellent stability to remortgage earlier than your deal ends. You ought to subsequently contemplate checking whether or not you’ve any early compensation expenses

If you might be mid-deal and wish to increase extra finance, you may ask your current lender for a separate top-up mortgage. This is named an extra advance, which can sometimes be at a special charge to your primary mortgage.

We enable you weigh up the professionals and cons of remortgaging early.

6. How a lot fairness you’ve in your home

Homeowners with little fairness of their houses could discover that remortgaging just isn’t their best choice.

The larger your mortgage to worth, the dearer the rate of interest can be.

And if property costs fall, you run a larger threat of ending up in damaging fairness, the place your mortgage is price greater than your home.

Find out: Is now an excellent time to remortgage?

Explained in 60 seconds: Variable-rate mortgage

What is a variable-rate mortgage?

The professionals and cons of remortgaging for home enhancements

There are upsides and drawbacks of remortgaging that your want to contemplate.

Pros:

You can repair your month-to-month repayments for years, supplying you with peace of thoughts.

There is loads of selection from lenders.

Cons:

By spreading the price of home enhancements over your mortgage time period, you may pay again considerably extra curiosity than with different finance choices.

You could also be charged a mortgage-arrangement charge, in addition to valuation and authorized charges.

The software course of may be prolonged and a full evaluation of your monetary circumstances can be carried out.

If you need to remortgage earlier than your present deal expires then you may be hit with an costly early compensation cost.

Find out extra: How quickly can I remortgage?

Some owners remortgage to pay for home enhancements

When is it higher to use a secured mortgage to fund home enhancements?

Remortgaging isn’t the one method to pay for home enhancements. You may take out a secured mortgage as a substitute.

This is a mortgage secured in opposition to your property to increase more money for a particular motive akin to home renovation. It is one other mortgage from a model new lender and is named a second-charge mortgage.

Like common mortgages, second-charge mortgages include a most mortgage to worth, which is a mix of your primary mortgage debt and the second-charge mortgage you need to take out.

So the utmost quantity you might be allowed to borrow for your renovation work and the rate of interest will rely on how a lot fairness you’ve constructed up in your property.

The charge will have a tendency to be larger than your authentic mortgage however will probably be on a smaller debt due to the chance to the secured-loan supplier.

The authentic lender is first within the queue if the house owner will get into hassle maintaining with repayments and the property has to be repossessed and bought to clear the debt.

A secured mortgage could also be extra appropriate than a remortgage when you:

Are tied right into a mortgage deal and can be penalised for remortgaging via early-repayment expenses.

Have had credit score points previously. Secured-loan suppliers may be extra lenient over credit score blips than mortgage lenders as a result of they are going to be advancing a smaller amount of cash.

Have not too long ago modified your private circumstances. For instance, secured-providers lenders could also be versatile about current job adjustments as a result of the quantity superior is decrease and subsequently the chance is lowered too.

Remortgaging could also be higher if:

Your current mortgage deal is coming to an finish. You can remortgage penalty-free on to a less expensive rate of interest than with a secured mortgage.

The home has gone up in worth because you took out your mortgage, permitting you to launch fairness with out rising your mortgage to worth or rate of interest.

Find out extra: Should I pay off my mortgage or make investments?

What are my different choices for funding home enhancements?

If taking out a remortgage for home renovation work just isn’t for you, listed here are some options:

Further advance. If you might be tied right into a fixed-rate mortgage however don’t need to delay your renovation, lenders will contemplate providing you a top-up mortgage.

Taking a second mortgage. This can be helpful if you’re tied right into a mortgage deal – although count on to pay a better charge of curiosity.

Use a home enchancment mortgage. This is a private mortgage that’s not secured in opposition to your home. Interest charges may be larger than mortgage charges and the time period and mortgage measurement are sometimes capped at 5 years and £25,000. But the appliance course of is usually quite a bit faster than with a remortgage.

Use a bank card. A 0% buy card may be cheaper than borrowing on mortgage for home enhancements when you repay the debt inside the interest-free interval, which may be up to two years. We record the very best bank cards.

Saving up. Instead of incomes virtually no curiosity in your money financial savings, you may put money into your home. It’s not at all times smart to use all of your financial savings as you may want spare money for emergencies.

Should I launch fairness for home enhancements?

That will depend on your age and circumstances. If you launch fairness out of your home, you’ll improve the scale of the debt you’ve to pay off.

If you’re nearing retirement and contemplating rising the scale of your debt then you’ve to contemplate what occurs when you nonetheless have mortgage funds if you find yourself retired.

We clarify how to remortgage to launch fairness.

You may additionally contemplate fairness launch which is a specialist mortgage reserved for owners aged 55 and over.

You don’t have to pay month-to-month curiosity. Instead, the curiosity may be rolled up and added to your stability annually. The fairness launch mortgage is repaid from the sale of your home, often whenever you die or transfer into long-term care.

You may need to learn our information on fairness launch.

We even have an article weighing up the professionals and cons of remortgaging versus fairness launch.

How to scale back your home renovation prices

Renovating your home on a finances? Make certain you:

Set your spending restrict at first

Break down the prices of your undertaking into supplies and labour to be sure it’s sensible

Factor in an additional 10% in case it prices greater than anticipated

Get three quotes for every job

To preserve prices down, reuse a few of your current fittings if doable

Hunt for second-hand instruments and furnishings on websites akin to Gumtree, Freecycle or Facebook Marketplace

You may need to learn: “We’re renovating our Victorian home on a straitlaced finances”

All merchandise, manufacturers or properties talked about on this article are chosen by our writers and editors primarily based on first-hand expertise or buyer suggestions, and are of a normal that we imagine our readers count on. This article comprises hyperlinks from which we will earn income. This income helps us to help the content material of this web site and to proceed to put money into our award-winning journalism. For extra, see How we make our cash and our Editorial promise.

Important data

Some of the merchandise promoted are from our affiliate companions from whom we obtain compensation. While we goal to function among the greatest merchandise obtainable, we can not evaluation each product in the marketplace.

CBA’s new Digi Home Loan product now live | Australian Broker News

News

CBA’s new Digi Home Loan product now live

Reaffirms dedication to dealer channel

Commonwealth Bank (CBA) has clarified its stance on the dealer channel after formally launching its controversial digital house mortgage providing for new-to-bank mortgagors that’s solely obtainable on-line.

The Digi Home Loan product, obtainable to eligible owners trying to refinance from one other monetary establishment, gives rates of interest ranging from 6.15% p.a at a most LVR of 80% for eligible clients (Owner Occupied, Principal and Interest repayments).

Customers with Homeowner standing as a part of CBA’s loyalty program Yello, will qualify for a month-to-month cashback on their Digi Home Loan beginning at $10 monthly. Additionally, eligible clients will obtain a loyalty cashback that will increase over time and kicks into motion after the primary anniversary of the mortgage.

Given the method is digital and accomplished by way of the CommBank app or InternetBank, clients can anticipate to obtain conditional approval “in a matter of minutes,” based on Commonwealth Bank of Australia’s government common supervisor house shopping for, Dr Michael Baumann (pictured above).

“We developed the Digi Home Loan as we all know there’s a rising variety of clients in search of a self-managed, digital house lending expertise,” stated Baumann.

“We are dedicated to creating a set of merchandise that meets our clients’ wants by way of all the channels obtainable to us – be it our community of lenders, mortgage dealer companions, or by way of our telephone or digital channels.”

Does CBA’s Digi Home Loan product undercut its Unloan providing?

Available to clients straight, the Digi Home Loan product is the primary CBA-branded providing that doesn’t function by means of its dealer channel or its digital department, Unloan.

While some might query whether or not this may undercut each channels, Baumann insisted every channel addresses totally different buyer wants.

“Over the previous few years – particularly since COVID – we’ve got witnessed a continued shift within the proportion of consumers who really feel comfy doing issues digitally and doing issues themselves,” Baumann stated.

“Through Unloan, we will present these clients who’re comfy utilizing digital applied sciences for his or her house mortgage wants with a competitively priced house lending resolution.”

Baumann stated the Unloan proposition is focused at clients with primary house lending wants, who’re in search of a house mortgage supplier that doesn’t present full-service banking wants.

“For these clients who’re comfy self-serving and utilising digital channels for his or her house lending wants and nonetheless desire a holistic banking relationship, our new Digi Home Loan is effectively positioned to satisfy their wants given the breadth of choices the CBA yellow model offers.”

“We will proceed to put money into our house mortgage proposition throughout our vary of manufacturers and channels, to satisfy clients the place they’re, and in the way in which they like.”

Is CBA turning its again on the dealer channel?

CBA’s choice to launch one other direct product comes after a 12 months of shifting priorities for the key lender.

In July 2023, the CBA CEO Matt Comyn stated that brokers stay an vital a part of help for its clients after ending its cashback gives within the months earlier than because the mortgage wars fizzled out.

By November, CBA had said it will give attention to its proprietary channel throughout its quarterly outcomes and in February CBA chief monetary officer Alan Docherty stated the financial institution would “not take part in unprofitable mortgage lending”.

CBA stands out among the many main banks for having a decrease proportion of loans coming by means of brokers. The financial institution’s broker-originated loans have dropped from 48% to 43%, whereas Westpac (65%), NAB (65%), and ANZ (61%) all rely rather more closely on brokers.

Despite this Baumann stated the “dealer channel stays an integral half” of the enterprise.

“As Australia’s largest lender with the very best quantity of dealer originated loans, we stay dedicated to this channel – which is obvious from the continuing investments we’ve got made and proceed to make,” Baumann stated.

“We know mortgage brokers are taking care of their clients and guiding them by means of the complexities of shopping for property and acquiring finance. We stay dedicated to the dealer channel as you possibly can see from our vital investments into folks in addition to broker-technology.”

What’s in retailer for the dealer channel?

Baumann pointed to current examples together with the launch of Your Applications and enhancements to Your Loans, in addition to the financial institution’s dedication to ongoing studying and improvement alternatives by means of our Broker Training Hub.

“We have additionally made enhancements to our accreditation standards to make it simpler for new brokers to turn out to be accredited with us. We proceed to make operational enhancements, together with the current improve of our Home Loan Pricing Tool in addition to the implementation of a self-employed deal desk,” he stated.

“And, we’re repeatedly reviewing and streamlining our lending insurance policies. We will shortly be launching additional tech enhancements that we hope will ship higher enterprise efficiencies for our dealer companions.”

Baumann stated driving innovation for its clients – together with the supply of distinct and differentiated buyer experiences – is core to CBA’s technique.

“For these clients who worth face-to-face help within the house mortgage journey, they’ll and can proceed to profit from the personalised house mortgage service that comes by way of our community of CommBank lenders or mortgage brokers.”

What do you consider CBA’s new Digi Home Loan? Comment beneath.