This information tackles a massive query: Can you employ your crypto to help make investments in a residence? We’ll search on the guidelines, what banks consider, and the way to use your digital cash in the house-obtaining technique.

Let us dive into how crypto can take part in a portion in touchdown your dream residence.

Can You Use Crypto to Qualify for a Mortgage?

According to pointers from massive entities like Fannie Mae and Freddie Mac, cash obtained in the sort of cryptocurrencies shouldn’t be certified to qualify for a monetary mortgage.

Likewise, belongings held in cryptocurrencies should not ready to be thought of for the required financial reserves required for mortgage approval.

This stance is echoed by the FHA and VA, which don’t formally acknowledge cryptocurrency as a managed foreign exchange, thus not accepting it proper for down funds or closing costs.

On the opposite hand, there may be a silver lining if cryptocurrency is remodeled into U.S. kilos and deposited into a U.S. or condition-controlled economical establishment, it might probably then be seen as for down fee, closing prices, and monetary reserves, supplied there may be ample documentation to validate the transaction.

Documentation proving the conversion of crypto into U.S. bucks and the switch of those money into a managed financial establishment is vital.

Loan corporations will possible request proof of the primary cryptocurrency transaction, the commerce into bucks, and the deposit into the borrower’s checking account.

It actually can also be important to notice that when cryptocurrency itself might probably not straight qualify as an asset or income, the liquidated worth held in compliance with monetary guidelines can take pleasure in a pivotal operate in the house mortgage software plan of action.

As a consequence, whereas the direct use of crypto for mortgage qualification faces constraints, strategic conversion, and documentation could make crypto property a sensible side of your dwelling-shopping for journey.

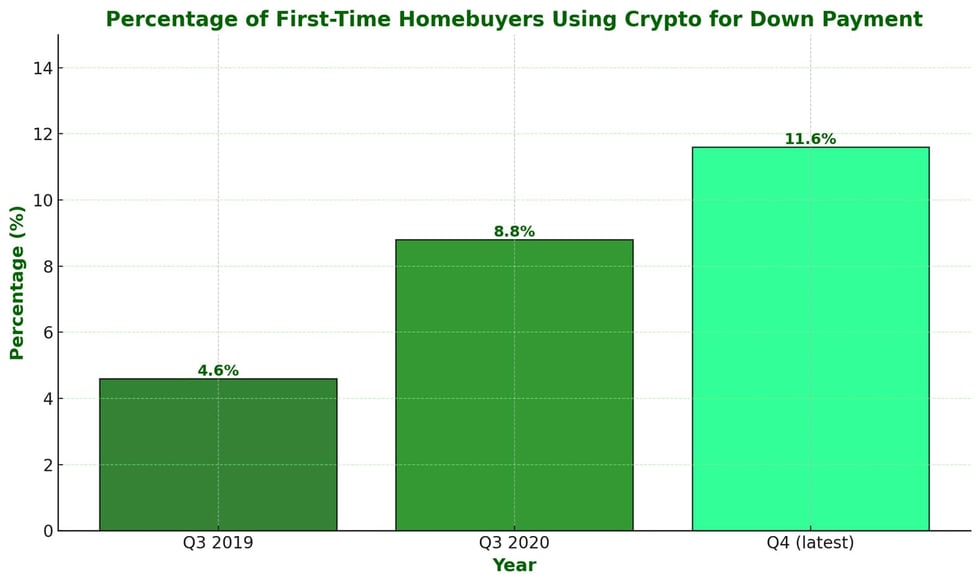

Data from Redfin.com

Expected Documentation for Applying Crypto in House mortgage Transactions

When using cryptocurrency for home mortgage transactions, lenders name for particular documentation. This makes certain that the digital property are transformed and held in accordance to regulatory benchmarks.

These paperwork are essential for the verification and acceptance of your crypto property in the private mortgage course of. Source: Fannie Mae

Documented proof of cryptocurrency remodeled to U.S. kilos.

Verification of funds held in a U.S. or condition-regulated financial institution.

Affirmation that assets are verified in U.S. bucks forward of financial institution mortgage closing.

Documentation proving the origin of the money from the borrower’s cryptocurrency account.

Regular Home finance mortgage Crypto Rules

If you are taking a look at making use of cryptocurrency belongings to qualify for a mortgage via Fannie Mae or Freddie Mac, there are distinctive suggestions and limits you want to be told of.

Each entities make it doable for cryptocurrencies to be seen as in the house mortgage method if they’ve been remodeled into U.S. {dollars} and are verifiably deposited into a U.S. or level out-regulated financial institution. This conversion should be documented completely.

The borrower may have to supply proof that the digital foreign money has been exchanged into U.S. {dollars}, and the assets have to be verified in U.S. bucks in advance of the mortgage closing.

This technique basically treats the liquidated cryptocurrency like another asset that the borrower would use in the path of their down fee, closing costs, or monetary reserves.

Any huge deposit into a borrower’s account that may come from cryptocurrency want to be sufficiently documented to display its origin. This includes supplying proof of the switch from the cryptocurrency account to a U.S. buck account.

For Fannie Mae and Freddie Mac, it is not nearly exhibiting that the cash at the moment are in {dollars} it is usually about tracing the assets once more to their supply to assure legality and compliance with monetary legal guidelines.

This rigorous documentation process is supposed to mitigate the possibility affiliated with the volatility and potential for fraud that cryptocurrencies can current.

So although Fannie Mae and Freddie Mac don’t particularly understand cryptocurrencies as legitimate for earnings or asset qualification, they do current a structured manner for doable homebuyers to leverage their crypto holdings.

By changing your digital property into U.S. kilos and pursuing inflexible documentation suggestions, you possibly can even now use your funding determination in path of shopping for a property.

FHA or VA Personal mortgage Crypto Guidelines

For individuals in making use of their cryptocurrency holdings to support in the mortgage mortgage process as a results of FHA (Federal Housing Administration) or VA (Veterans Affairs) monetary loans, it really is significant to perceive the exact suggestions that govern these transactions.

As opposed to common monetary loans provided by Fannie Mae or Freddie Mac, FHA and VA have their one in all a form stance on cryptocurrencies, which proper impacts how doable homebuyers can use their digital belongings.

Equally the FHA and VA don’t acknowledge cryptocurrency as an appropriate sort of down fee or as a particularly usable asset in the house finance mortgage software system.

For the FHA and VA to take note of these assets as side of the borrower’s property, the remodeled foreign exchange want to be deposited in a checking account for at the very least 60 days earlier than the mortgage mortgage software.

This time interval permits the money to be seen as “seasoned,” indicating they’re taken care of as customary, certified borrower money.

This seasoning time period is mirrored in a 60-working day unusual concord, which collectors will overview to set up the borrower’s fiscal safety and means to add to the down fee and shutting prices.

It is critical to retain crystal clear and full documentation of the conversion from cryptocurrency to U.S. kilos, which incorporates transaction receipts, financial institution statements, and any correspondence with cryptocurrency exchanges.

This documentation can be essential in proving the origin of the funds and their eligibility beneath FHA and VA pointers.

So, while direct use of cryptocurrency property shouldn’t be permitted under VA and FHA private mortgage methods, changing these belongings to U.S. bucks and correctly seasoning them in a lender account offers a sensible route for homebuyers.

Often Questioned Questions

Here are solutions to typical points centered on what homebuyers often search for regarding making use of cryptocurrency in mortgage transactions.

Can I take advantage of cryptocurrency immediately for a down fee on a family?

No, cryptocurrency by itself merely can’t be straight utilized for a down fee. Even so, whether it is actually remodeled to U.S. {dollars} and deposited into a managed financial institution, it might be seen as.

Is cryptocurrency thought to be an asset by residence mortgage mortgage suppliers?

Cryptocurrency shouldn’t be immediately thought to be an certified asset for mortgage mortgage packages. Transformed cryptocurrency into U.S. kilos held in a financial institution could be seen as.

How do Fannie Mae and Freddie Mac see cryptocurrency in home mortgage functions?

Fannie Mae and Freddie Mac don’t take cryptocurrency straight as earnings or an asset. Converted crypto to U.S. {dollars} with right documentation is required.

What documentation is required to use cryptocurrency for home mortgage transactions?

Documentation consists of proof of conversion to U.S. {dollars}, verification of those funds in a regulated institution, and proof of the supply of those funds.

Can FHA or VA loans settle for cryptocurrency?

Equally FHA and VA don’t work out cryptocurrency proper for down funds or as an asset however will take into consideration transformed cryptocurrency in U.S. {dollars} with appropriate seasoning and documentation.

How lengthy do cryptocurrency assets want to have to be seasoned in advance of they’re thought to be legitimate for a mortgage mortgage?

Cash from transformed cryptocurrency ought to sometimes be seasoned in a monetary establishment account for on the very least 60 occasions to be thought to be for mortgage packages.

Do mortgage corporations contain proof of cryptocurrency conversion?

Certainly, mortgage corporations want documented proof of the cryptocurrency conversion to U.S. bucks and the deposit into a managed financial institution.

Can I take advantage of cryptocurrency earnings as proof of income for a mortgage mortgage?

Revenue been given in cryptocurrency shouldn’t be appropriate. Earnings want to be remodeled to U.S. bucks and correctly documented to be regarded.

How do USDA loans watch cryptocurrency?

USDA monetary loans presently shouldn’t have a distinctive plan with regards to cryptocurrency, indicating the acceptance of remodeled crypto money might depend on the lender’s strategies.

Are there any unique standards for huge deposits from cryptocurrency?

Of course, for massive deposits originating from cryptocurrency, mortgage corporations will discover in depth documentation to guarantee the legitimacy and supply of the money.

Bottom Line

Working with crypto for a mortgage is about recognizing the procedures and buying the perfect paperwork. You are unable to use crypto straight, however in case you convert it into U.S. kilos very first, you’re on the suitable observe.

Make certain to doc all of the issues accurately. It could be all about establishing and altering your crypto neatly.

If you’re aiming to get a property in Florida and wish to use your crypto, take a look at MakeFloridaYourHome, we are able to help data you by all of it.

.png)