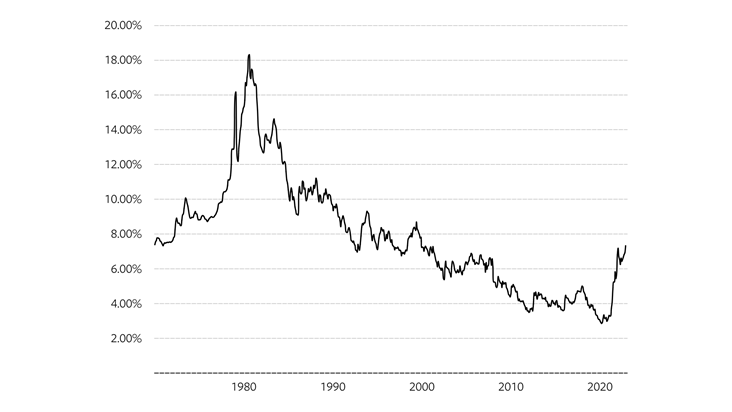

Thursday, the Bureau of Labor Statistics reported the identical craze that each one Americans have seen as of late: the inflation fee of progress is rampant and doesn’t exhibit any signal of easing up attributable to the Russian Invasion of Ukraine. The Consumer Price tag Index for all Urban People “elevated .8 % in February on a seasonally altered foundation after climbing .6 p.c in January…. More than the final 12 months, the all objects index elevated 7.9 per cent previous to seasonal adjustment.”

As you possibly can see under, the CPI inflation cost of progress chart seems to be like many monetary charts in the course of this COVID-19 restoration and progress: a parabolic-type transfer deviated from present historic norms. Our financial system is working heat, and the labor market is receiving hotter.

Throughout the COVID-19 restoration section, I predicted that occupation openings would crack round 10 million. This 7 days, we simply broke to an all-time substantial in job openings with near 11.3 million.

What does that essentially imply? Wage development is heading to kick up!

Early in 2021, I instructed the Washington Put up that rental inflation was about to only take off and can select the shopper price index up extra rapidly and really final for a longer interval. For me, it is typically about demographics equal demand. Wages are rising, which signifies rent is about to get elevated.

Shelter inflation, the most main part of CPI, is producing its vital thrust as folks wish to reside someplace and that shelter worth is a precedence about most factors. Rent inflation on a yr-more than-year foundation has been extraordinary in chosen cities, averaging in extra of double digits.

Now we are able to see that staying a renter has been problematic as a result of hire inflation is getting off, gas prices are taking off, and even though wages are up, the common merchandise clients expend money on have gone up in the most notable vogue in the newest background.

In some situations, seeing this number of rental inflation can encourage customers to get a home for the cause that leasing a dwelling is not as low price as an resolution any longer. Nonetheless, in case you’re a youthful renter and looking out to acquire a dwelling a handful of years away, this could make price financial savings for a down cost a lot far more of a downside. On better of all that, attributable to the truth stock is at all-time lows, it is been more durable and tougher for to begin with-time homebuyers to earn some bids just because they by no means have extra cash to offer into the bidding method.

As at all times, the marginal homebuyer will get hit with greater costs and larger family costs. Now, single home renters are paying out far more for his or her shelter, creating the property-shopping for course of far more difficult financially.

What can Us residents do to hedge them selves from this? In reality, remaining a property proprietor round the earlier 10 years has set clients up correctly all by this burst of inflation!

How is that?

Housing is the price ticket of shelter to your potential to very personal the debt it’s not an funding. This has been my line for a ten years now. Shelter worth is the key driver of why you possibly can presumably wish to possess a dwelling. The reward of changing into a home-owner is that with a 30-yr mounted mortgage fee, that home mortgage cost is set for the on a regular basis residing of the monetary mortgage. Sure, your property tax or protection might go up, however the property finance mortgage cost is regularly preset.

What has occurred about the a very long time is that American householders have refinanced time and time over again to the place their shelter worth acquired lowered and cut back as their wages rose above time.

We can see this in the info. It has not at all seemed much better in heritage with the current refinance progress we noticed all through the COVID-19 restoration, since house mortgage debt is the most main shopper private debt we now have in The usa.

This would suggest that household private debt funds are at poor levels as completely. Which they’re, as we are able to see below.

In the remaining 10 a very long time, the vital distinction is that we made American Property finance mortgage Credit card debt Fantastic Again by producing it uninteresting. Whilst wages rise, extended-term preset bank card debt cost stays the identical. It doesn’t get any significantly better than that. So how does this make staying a home proprietor a hedge towards inflation?

As the worth of residing rises, wage progress has to match it, particularly in a fairly restricted labor sector. Providers can no prolonged pay for to not maximize wages to entice workforce to work and retain personnel. Wages are heading up!

What doesn’t go up? Your property finance mortgage cost as a home-owner. So, you possibly can reward from rising wages although the most sizeable cost stays the actual. Why do I proceed to maintain stressing that the homeownership benefit is a preset decrease monetary debt cost versus growing wages? While renters sense pressured about rental inflation and larger gasoline worth ranges, owners not at all want to stress about their sub-3% home mortgage worth escalating vs . the 7.9% inflation worth of growth.

Some women and men who’re astonished by all this inflation we now have had in extra of the earlier calendar yr at the moment are asking how the U.S. financial system can keep pushing collectively. Not each single home is the an identical. If you’re a renter, your rents have gone up and that may take absent out of your disposable earnings and helps make it more durable to assist save for a down cost as correctly. If you might be a property proprietor, the inflation price ticket is not as undesirable, contemplating the truth that you’re benefiting from mounting wages. That offsets the worth of residing and you might be innocent in your own home with that mounted merchandise.

This is good for a property proprietor, but it surely contributes to a bigger sized downside: The home-owner is executing a minimal means too properly and will properly don’t have any inspiration to go. Why would everybody wish to surrender a sub-3% mortgage mortgage payment and these a stable good onerous money move besides they’re buying something that may make their cost a nice deal cheaper? Persons go all the time for a number of distinctive explanations. Having stated that, let’s be life like right here: housing stock has been slipping since 2014 and 2022 isn’t wanting any significantly better.

Also, traders which have purchased homes for rental generate are taking pleasure in the actuality that wages are mounting just because it gives them a rationale to lift the rent. In a lowered fascination-fee environment, rental produce is a excellent useful resource of money move.

We haven’t needed to supply with substantial inflation quantities for fairly a few many years, and again once more in the late Seventies, property finance mortgage charges have been a complete lot greater, so it is not an apples-to-apples comparability anymore. This is a model title new ball online game with how advantageous it has been to be a home-owner in The usa. It is not incredible info if you’re involved about stock buying lowered, as I’m.

I usually make pleasing of my housing crash addict pals who’ve been incorrect for a 10 years. Even so, now I inform them: you might be implying educated house homeowners who’ve glorious {dollars} stream will, for some clarification, present their houses at a 40%, 50% or 60% discounted simply to lease a dwelling at a bigger cost than what would have been the state of affairs for a lot of a very long time.

Human beings by no means run that means. On the different hand, there is a draw back to deal with homeowners getting this type of good financials: they don’t have a trigger to surrender a good factor. This is simply a completely different clarification I maintain saying this is the unhealthiest housing sector article-2010. As you possibly can see greater than with the FICO scores of house homeowners, their earnings stream seems to be great and from this burst of inflation, proudly owning a property is a good hedge.

My concern has typically been with stock going lower and decrease in the a very long time 2020-2024. Now, with householders in search of so good on paper, we now have entered uncharted territory the place mortgage charges for up to date owners are at the least costly levels at any time recorded in background, stock phases are at the least costly ranges at any time and now the price of dwelling from a rise in inflation has taken off in an excessive means. The main downside I see under is that this could make the housing inventory scenario considerably worse as house homeowners now have even extra incentive to in no way go away their households.