How have the dwelling financial institution loan charges moved? | Australian Broker News

News

How have the property financial institution loan charges moved?

Furthermore insights on RBA’s upcoming transfer

The previous week seen totally different alterations in the house loan premiums amongst Australian collectors, Canstar claimed.

3 collectors better 18 owner-occupier and dealer variable prices by an frequent of .13%, though two different loan suppliers slash 23 mounted expenses by a mean of .19%.

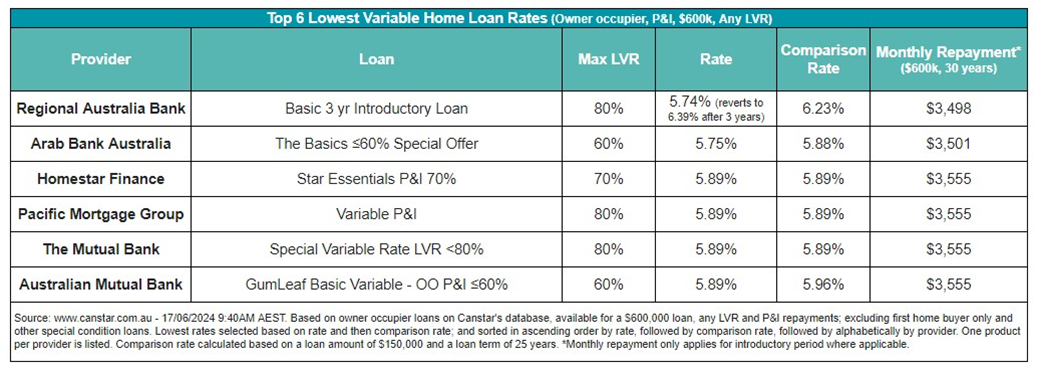

Even with these modifications, 26 prices carry on being beneath 5.75% on Canstar’s databases, in step with the earlier week.

The latest frequent variable fascination stage for owner-occupiers shelling out principal and fascination stands at 6.87%. In the meantime, the least expensive obtainable variable cost for any LVR is 5.74%, an introductory price offered by Regional Australia Financial establishment.

Canstar commentary on financial coverage

Steve Mickenbecker (pictured earlier talked about), Canstar’s group govt for financial suppliers and primary commentator, offered insights into the Reserve Bank’s forthcoming choices.

“A mixed bag of particulars seems possible to see the RBA depart the revenue price nonetheless left on preserve,” Mickenbecker defined. “March quarter inflation was up and the housing present market is once more booming, however financial development has stalled. The RBA will maintain out on no less than the June quarter Purchaser Value Index quantity proper earlier than relocating on the money price.”

“In awful info for debtors ANZ Bank has pushed out its projection for a initially onerous money quantity reduce to February 2025 in response to slower than predicted progress of inflation in the direction of the 2% to three% RBA consider band. The different huge banking establishments are sticking to November 2024 for now,” Mickenbecker talked about.

Implications of potential quantity cuts

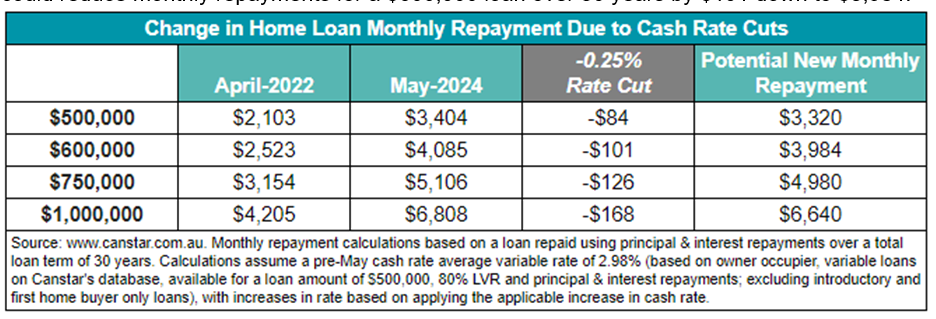

RBA managed the onerous money value at 4.35% as of Could 2024. Nonetheless, anticipations are excessive for a forthcoming stage slice, most likely resulting in a reduce in month to month repayments for debtors.

For instance, a .25% cut back might reduce down common month-to-month repayments on a $600,000 private loan over 30 a very long time by $101, bringing it all the way down to $3,984.

Get the hottest and freshest house loan information delivered correct into your inbox. Subscribe now to our FREE each day publication.

Connected Stories

Hold up with the most up-to-date information and conditions

Sign up for our mailing guidelines, it’s free!

The Federal Housing Finance Company is on the lookout for comment from the general public on strategies that the Federal Household Bank loan banks’ cost-effective housing applications might be made far more profitable and inspire greater participation.

The Federal Housing Finance Company is on the lookout for comment from the general public on strategies that the Federal Household Bank loan banks’ cost-effective housing applications might be made far more profitable and inspire greater participation.