![]()

Barclays and HSBC have each of these produced fee reductions on discover merchandise and options, efficient from tomorrow (5 July).

Barclays has decreased costs on its residential options similar to the present dwelling finance loan purchaser (EMC) reward 75% private loan-to-benefit (LTV) two-yr repair, which has been slash by .25% from 4.90% to 4.75%. This will include a product value of £999, minimal financial institution loan £5k and highest mortgage £2m.

Other reductions within the residential assortment incorporate:

• 5.65% EMC Reward two-yr mounted £999 product price, 85% LTV, min monetary loan £5k, max financial institution loan £2m, will cut back to 5.22%

• 5.83% EMC Reward two-year preset £0 answer fee, 85% LTV, min loan £5k, max mortgage £2m, will decrease to 5.43%

In the lender’s acquire-to-permit (BTL) selection, the EMC reward 65% LTV two-yr preset will probably be minimize from 5.50% to 5.30%. This comes with no product value, naked minimal loan of £5k and biggest monetary loan of £1m.

Further extra BTL reductions include:

• 5.20% EMC Reward BTL two-12 months fastened £1,795 services or products fee, 75% LTV, Min monetary loan £5k, Max financial institution loan £1m, will cut back to 5.00%

• 5.15% EMC Reward BTL two-yr set £1,795 merchandise price, 65% LTV, Min financial institution loan £5k, Max mortgage £1m, will decrease to 4.95%

Meanwhile, HSBC has declared cuts throughout quite a few ranges. These contain current family shopper switching, present family purchaser borrowing extra, residential to begin with-time client (FTB)/family shift and the equal electrical energy profitable variation.

Variations may also be created on residential remortgage, residential remortgage cashback, remortgage electrical energy economical ranges and worldwide residential dwelling loans.

The lender has launched a cashback incentive offering on its Uk family FTB merchandise and options at 60%, 70% and 75% LTV.

In addition, it has enhanced the cashback incentive providing on its United kingdom residential FTB vitality efficient Houses choice (A&B EPC rated attributes) at 60%, 70% and 75% LTV.

The strikes arrive as sonia two-yr swap fees fell to 4.480% on 2 July from 4.612% on 3 June, although five-calendar 12 months prices had been down to 3.983% from 4.053% above the exact same interval.

Commenting on the modifications, SPF Non-public Customers predominant govt Mark Harris says: ‘With the huge 5 collectors – Barclays, HSBC, Santander, Halifax and NatWest – lowering their mortgage loan costs this week, loan providers proceed to jostle for small enterprise as they ramp up the summer time months gross sales.”

“Those lenders who haven’t but repriced are attainable to adjust to match, as prolonged as firm ranges allow.

“Even although Swap charges, which underpin the pricing of fastened-amount mortgages, aren’t demonstrating a dependable downwards craze, the need to crank out much more small enterprise appears to be motivating lenders to tweak their costs.

“It’s implausible information for debtors, a lot of whom are having difficulties with affordability simply after successive price rises and then holds. Expectations of a price discount in August are greater.”

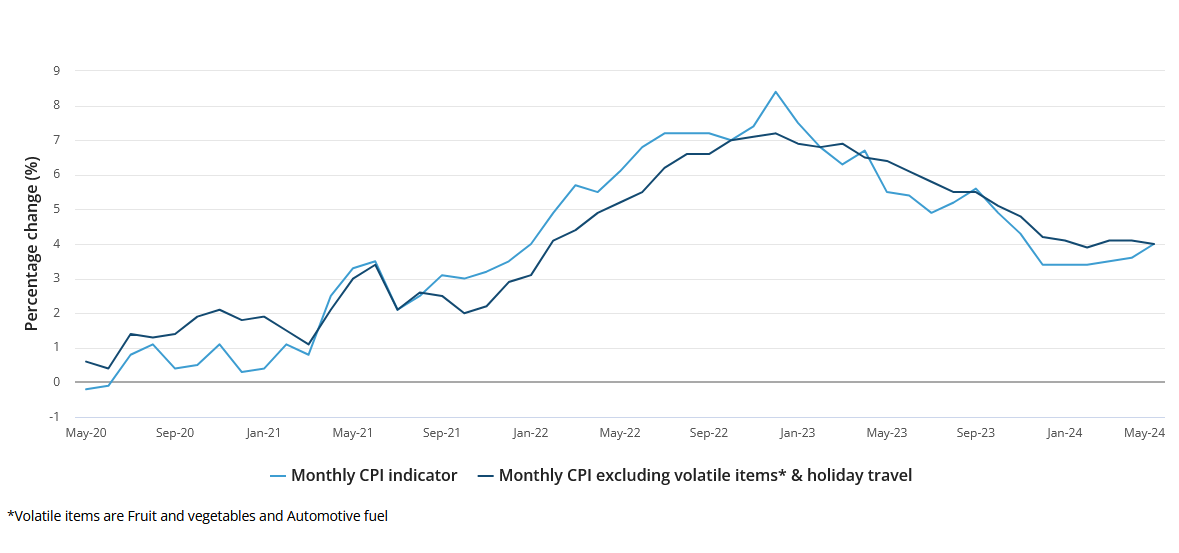

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator