Millions fear credit rejection | Australian Broker News

News

Millions fear credit rejection

Fear stops Aussies in search of credit

New analysis from Finder, Australia’s most visited comparability website, revealed that tens of millions of Australians are avoiding credit functions resulting from fear of rejection.

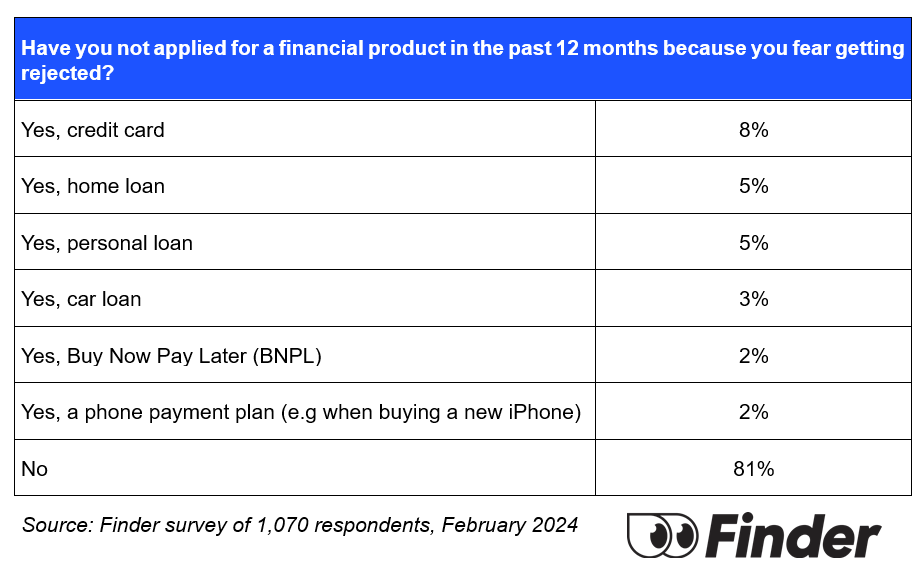

A survey of 1,070 respondents discovered that 19% of Australians, almost 4 million folks, haven’t utilized for a monetary product previously 12 months as a result of they have been fearful about being knocked again.

Credit software nervousness

Sarah Megginson (pictured above), cash knowledgeable at Finder, defined the priority.

“As cash has gotten costlier to borrow, many lenders have change into extra scrupulous about who they’ll lend it to and it’s making folks nervous,” Megginson mentioned.

“If you don’t assume you’d meet the factors imposed by lenders to safe the entry to funding you want, you’re clever to steer clear.”

Impact on monetary merchandise

The survey discovered that 8% – 1.6 million folks – hadn’t adopted by means of on a credit card software, whereas 5% had prevented private mortgage functions.

Other monetary merchandise, together with residence loans (5%), automobile loans (3%), and cellphone cost plans (2%), have been additionally bypassed resulting from fear of rejection.

Improving approval probabilities

Megginson recommended steps to enhance credit approval probabilities.

“Avoid issues like payday loans, credit card money advances, and BNPL transactions, as lenders see these kinds of habits as a ‘crimson flag’ that you simply’re not capable of stay inside your means,” she mentioned.

Megginso additionally encourages checking your credit rating earlier than making use of for a mortgage or product.

“A great credit rating will open up higher monetary alternatives, corresponding to quicker mortgage approvals, decrease rates of interest, and simpler rental processes,” Megginson mentioned.

Cost-of-living disaster

Megginson highlighted the broader impression of the cost-of-living disaster.

“Households in all revenue brackets are feeling the pinch and it’s a vicious cycle,” he mentioned. “Those who want the credit can’t entry it and people who can be authorised for the credit don’t want it as a lot.”

Advice for mortgage holders

For mortgage holders, Megginson advisable looking for higher mortgage charges.

“For many households, the largest hit comes from the mortgage, so begin there. Even a modest discount of 0.25% can translate into substantial financial savings,” she mentioned.

Getting again on observe

Megginson additionally advises making a plan of motion for these fighting family prices.

“If you’ve reached your restrict on a credit card, devise a plan to start paying it down,” she mentioned. “If you might be eligible for a 0% steadiness switch card, this might provide you with some respiration room, or you could possibly name your current credit card supplier and ask them to maneuver you to a card with a decrease rate of interest.”

For additional help, she recommended contacting the federal government’s free National Debt Helpline on 1800 007 007.

Get the most popular and freshest mortgage information delivered proper into your inbox. Subscribe now to our FREE each day e-newsletter.

Related Stories

Keep up with the most recent information and occasions

Join our mailing listing, it’s free!