Mortgage demand drops amid credit rating pressure | Australian Broker News

News

Mortgage loan demand from prospects drops amid credit historical past pressure

Credit historical past card demand from prospects rises

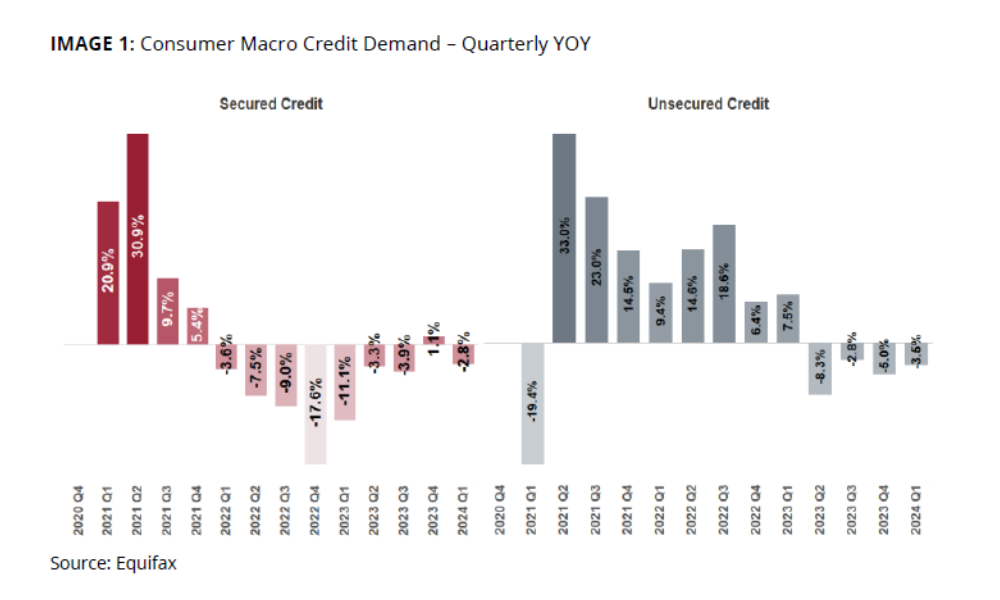

Home loan demand fell by 4.5% within the March quarter of 2024 versus the earlier yr, nonetheless troubles persist as the 2 the typical limitations and arrears on these monetary loans carry on to spice up, in accordance to Equifax.

“Over the earlier calendar 12 months, refinancing has been an important driver of mortgage want as individuals who ended up attaining the conclusion of their fixed-amount time frame sought out better offers,” reported Kevin James (pictured above), regular supervisor advisory and strategies at Equifax. “Many of those mortgage holders have now refinanced and this demand has dropped off.”

The most present Equifax Quarterly Shopper Credit historical past Insights confirmed that in Q1 2024, secured credit demand from prospects, largely from mortgages and car monetary loans, lowered by 2.8% when in comparison with the exact same interval in 2023.

Ongoing property finance loan rigidity

The Equifax report, which steps the quantity of credit rating functions for credit rating playing cards, customized loans, receive now pay later (BNPL), mortgages, and automobile loans, additionally discovered that no matter safe fascination charges, home loan nervousness is intensifying.

“While mortgage loan want has declined, the everyday prohibit for each new property finance loan account continued to enhance at a gradual tempo of seven% 12 months-on-calendar 12 months – reflecting rising family worth ranges,” James claimed.

“Additionally, we’ve considered increased residence loan stress this quarter no matter secure fascination costs residence loan arrears elevated throughout all teams. Arrears of 30-89 instances earlier due elevated 15% year-on-yr, while arrears of 90+ instances previous due to have been up 17%.”

Credit historical past automobiles and vehicles buck the sample

Although whole unsecured credit want noticed a lower of three.5%, want for credit rating playing cards surged by 13.2% when in comparison with the an identical interval final calendar 12 months. The enhance contrasts sharply with the declines observed in private monetary loans (-4.6%) and BNPL companies (-24.7%).

“We’ve observed a significant uplift in credit rating card want, with quite a few Australians reaching out for unsecured credit rating to ease cost of dwelling pressures,” James talked about. “We’re additionally seeing strong progress in credit rating card boundaries, up 29% calendar year-on-12 months, which signifies prospects are making use of for additional {dollars} on their playing cards.”

Rising arrears signaling amplified monetary pressure

The financial pressure on people is clear not solely within the want for increased credit historical past card limits but additionally within the rising arrears all through a wide range of credit historical past kinds. Private mortgage arrears have arrived at their greatest place as a result of 2020 and are predicted to peak within the second quarter as trip bills become thanks.

“While demand from prospects for particular person loans has dropped, arrears on this portfolio are rising,” James reported. “In actuality, private loan arrears of much more than 30 instances previous due to have hit their most level contemplating the truth that 2020. And we hope this growth to proceed – private mortgage arrears generally tend to peak in Q2, as festive season paying out turns into owing.”

To evaluate probably the most up-to-date figures with the earlier advantages, click on right here.

Get the perfect and freshest property finance loan info despatched correct into your inbox. Subscribe now to our FREE on a regular basis e-newsletter.

Continue to maintain up with the newest information and events

Sign up for our mailing report, it’s cost-free!