New house listings present quicker | Australian Broker Information

News

New dwelling listings market extra quickly

Buyer self-assurance drives quick income

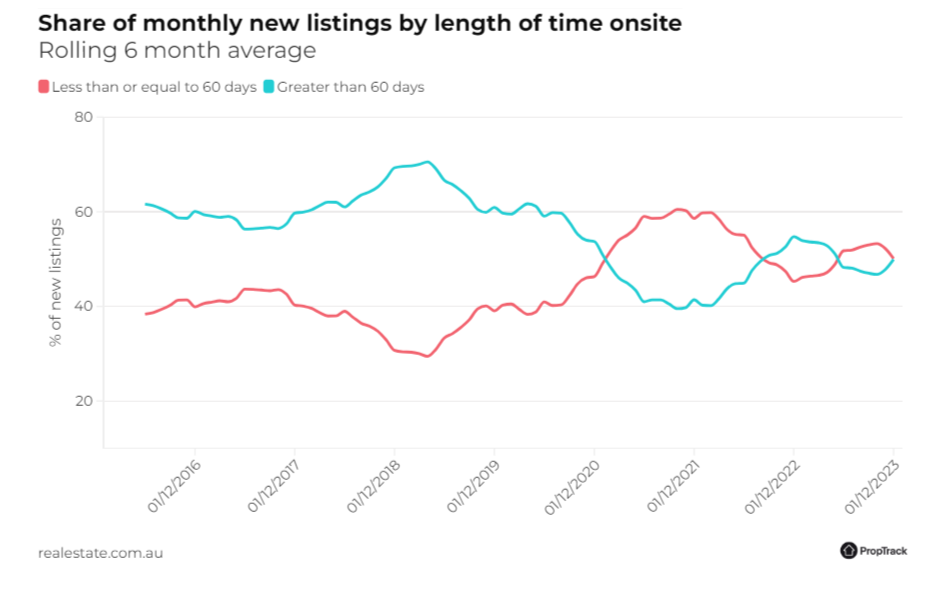

New dwelling listings are providing extra shortly, notably in funds metropolitan areas, as increasing purchaser confidence and an absence of latest listings journey down the time houses expend on {the marketplace}, new PropTrack evaluation confirmed.

“The velocity at which listings are purchased fluctuates over time, lowering when sector circumstances are sturdy and escalating when the sector is in a stoop,” defined Karen Dellow (pictured earlier talked about), senior knowledge analyst at REA Group.

Pandemic’s impression on product sales pace

Prior to the pandemic, most new listings purchased in 60 instances or much more. Nonetheless, by the top of 2020, increased residence demand led to further new listings getting bought inside 60 instances than folks increased than 60 days. This craze reversed in the middle of 2022 resulting from rate of interest rises dampening shopper demand from prospects.

Existing market tendencies

Now, with stronger shopper sentiment and a continued scarcity of latest listings, houses are remaining snapped up speedier.

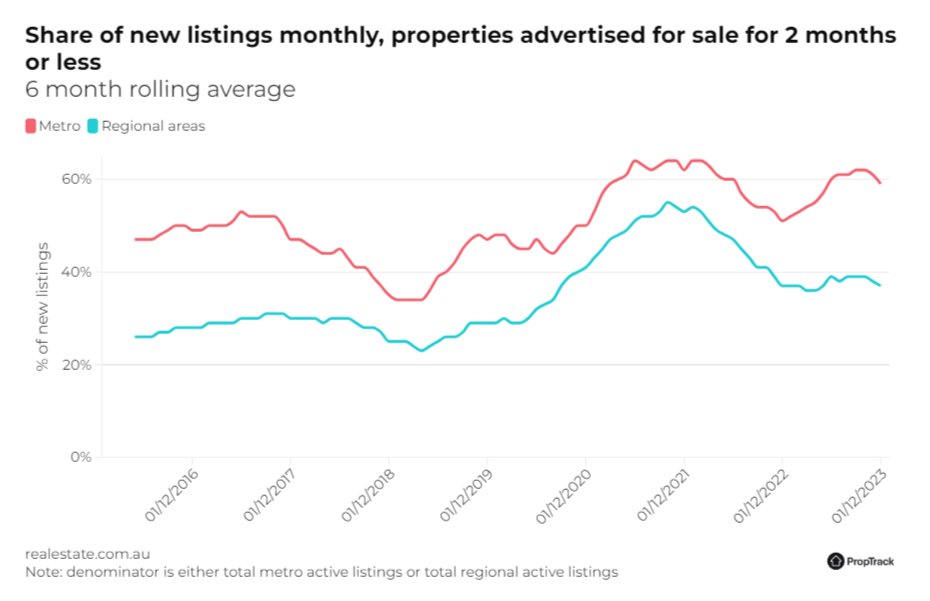

“New listings in metro locations are getting snapped up the speediest,” Dellow talked about, with metro listings averaging 58% purchased in simply 60 days in 2023, versus 38% for regional listings.

Sizzling markets

Adelaide is at the moment the most well-liked market place, with 66% of latest listings marketed inside 60 instances in December 2023, a 37% enhance from December 2022. Perth and Brisbane additionally noticed substantial boosts, each escalating by 37% greater than the equivalent time interval.

Extended-phrase listings

Even with the transient turnover of latest listings, rather more than 60% of whole listings on the internet each month have been onsite for 90 instances or further.

“If a property is not going to promote inside 60 days of staying outlined, the chance of promoting following 60 instances decreases significantly,” Dellow reported.

For sellers, the speedy sale of homes is reassuring, notably in money metropolitan areas.

“But the small print shows how important it’s to supply a property in simply 60 days in any other case the chance of promoting diminishes in extra of time,” Dellow claimed.

To study the PropTrack analysis in whole, merely click on listed right here.

Get the most well liked and freshest mortgage mortgage information despatched acceptable into your inbox. Subscribe now to our FREE day-to-day e-newsletter.

Related Tales

Keep up with the latest data and conditions

Be a part of our mailing itemizing, it is freed from cost!