The full monetary panorama, corresponding to house finance loan costs, has modified this 7 days, organising with the Fed’s talking elements on Wednesday. The honey badger labor market place is nonetheless going robust as we acquired one other stable work alternatives report Friday, which pushed bond yields elevated at initially. Nevertheless, the approach the working day completed confirmed that rework is coming.

We now have a far better technique of what the Federal Reserve needs to do with their Fed price hikes, and we now have a entire lot of particulars that demonstrates that the financial local weather will search completely different 12 months from now. This shall be important to imagine about heading into 2023, in specific if the labor market place does what the Federal Reserve wishes it to do, which is gradual down a lot of to develop a occupation decline recession.

This week, Fed Chairman Powell talked about how the Fed doesn’t need to above-hike the general financial system, which might then energy them to cut back costs sooner afterward. It affirms my notion that a nice deal of their aggressive talking factors over the earlier 12 months had been geared toward sustaining fiscal problems as tight as possible proper up till they obtained to their impartial fed cash price.

The Fed didn’t need mortgage loan charges to go lowered or the stock sector to rally. Now it seems that a 5% fed cash price is strictly the place they need to go. Can they get there with a slower price of mountaineering prices? We shall see. The labor current market has been a single of the two pillars they’re standing on for his or her aggressive price hikes in 2022, so let’s seem at the process data proper now.

From BLS: Complete nonfarm payroll work enhanced by 263,000 in November, and the unemployment price was unchanged at 3.7 p.c, the U.S. Bureau of Labor Data claimed now. Noteworthy place positive factors occurred in leisure, hospitality, effectively being care, and authorities. Employment declined in retail commerce and transportation, and warehousing.

Underneath is a breakdown of the unemployment quantity tied to the training diploma for these 25 many years and older. We observed a noticeable lower in the unemployment value for all those that hardly completed vital college, whereas different academic attainment teams noticed their unemployment prices rise a bit.

Considerably lower than a substantial school diploma: 4.4%%. (prior 6.3%)Higher college graduate and no school: 3.9%Some faculty or affiliate diploma: 3.2%Bachelor’s diploma or higher: 2.%

Remember, individuals who get hit the hardest in every and each financial downturn are folks with no a substantial college training. This is why we like the financial local weather to have a tighter labor market place, so people of all academic backgrounds will be utilized.

On April 7, 2020, I wrote the America is Back once more restoration mannequin for HousingWire, which I then retired on Dec. 9, 2020, as the restoration was on secure footing based mostly on my get the job completed. It took a while to get well all the jobs misplaced to COVID-19, however little or no like what we skilled after the terrific economical recession of 2008. Suitable on program, we obtained all the careers again that we dropped to COVID-19 by September 2022, and occupation openings had been over 10 million.

Now that these employment have been recovered, we should bear in mind that the work ranges are nonetheless poor for the cause that we might have much extra males and girls performing if COVID-19 hardly occurred. So, really feel of it as actively enjoying seize up with these occupation positive factors. In extra of time, we’ll return to our slower and common occupation positive factors if we will keep away from a recession. Don’t neglect, we skilled the longest financial and work progress in historic previous earlier than COVID-19 hit us with a tremendous rapidly restoration correct proper after.

Some of the weak level in the work alternatives report is in components the place by we now have seen headlines of layoffs coming. As you possibly can see down beneath, layoffs in retail commerce, transportation, and warehousing have been talked about in the media, and we’re lastly viewing all these positions being shed in all these sectors.

The unemployment price is cut back than the headline info exhibits when you solely rely folks ages 20 and up, the unemployment price is 3.4% for males and 3.3% for females. We not often concentrate on this knowledge line, but when the Fed mentions needing a bigger unemployment cost, they aren’t contemplating children 1st.

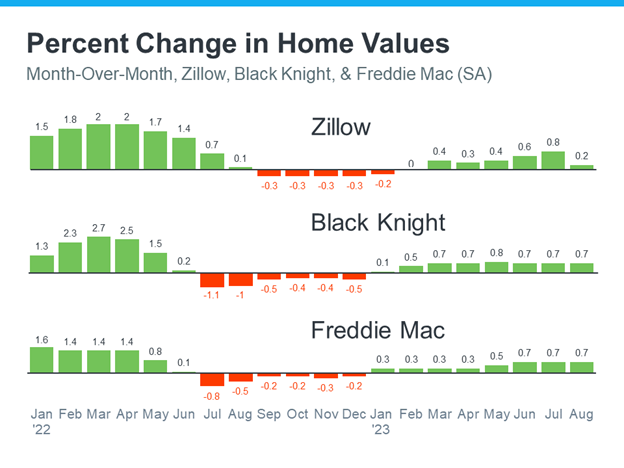

We noticed a intriguing bond trade response proper now quickly after the positions report arrived out. Ideal following the report, bond yields shot up, which was horrible for property finance loan prices as prices did go a little bit higher. As I create this report, nonetheless, bond yields have retraced the elevated levels and have absent lower in yields for the day, which is a constructive for house loan prices.

When I talked about the Fed pivot in a latest HousingWire Each day podcast, I outlined that the bond market would get in advance of the Federal Reserve pivot. As usually, the Fed shall be late to the exercise.

The Federal Reserve frequently talks about boosting costs centered on the good labor market. After the labor market place breaks, the Fed conversing factors about being intense to battle inflation won’t topic a nice deal as Americans shall be getting rid of positions. I think about they know this as very effectively and at that place the Federal Reserve will pivot its language, however the marketplaces shall be properly in advance of them.

Since I’ve all six recession purple flags up now, I’m sustaining a watch on jobless statements information 1st since as quickly because it breaks higher, the occupation-reduction recession has began. This is one thing we now have seen in every particular person financial expansion-to-economic downturn cycle.

I simply currently wrote about what I have to need to see to keep away from the brief-phrase work decline recession. On Thursday, jobless guarantees data fell once more quickly after rising in the prior 7 days to 241,000 and at the moment are right down to 225,000. My essential degree listed right here is 323,000 on the four-7 days relocating common for the Fed pivoting, which signifies one thing distinct to each particular person.

Overall, this was a nice work alternatives report. Wage enlargement is a little bit scorching right here, however I imagine that we now have some one particular-offs in the knowledge that gave it a improve in this report.

Some folks take a look at the home survey knowledge displaying additional weak spot in the labor markets. For these folks, at this stage of the monetary enlargement, with all my financial downturn pink flags up, jobless guarantees are the most important information line we now have. In the rock, paper, scissors match, I’d select jobless claims above the positions particulars and work openings, which fell in the most up-to-date report

A serious progress this week is that the Fed is telling the basic public they’re conscious of about-mountaineering costs. The bond market and house loan prices have fallen a great amount because of the reality the weaker CPI print in November: mortgage loan prices have been down 1% since then.

However, the bond market’s response at present, even following the improved-than-expected employment report, is the real story of the week. A quantity of months in the past, a good work alternatives report would have pushed the 10-calendar yr produce up much elevated and it might have closed the working day elevated, which might be undesirable for mortgage costs.

These days, however, bond yields completed the day down they may not even preserve the positive factors quickly after the stronger-than-expected jobs report. This is a very huge deal from my perspective. Today’s profession report and the bond sector response to it could possibly be an inflection stage the place the bond market is commencing to pivot in advance of the Federal Reserve. The concern is, when will the Federal Reserve be half of the celebration?