Brokers react to RBA cash rate pause | Australian Broker News

News

Brokers react to RBA cash rate pause

Brokers share what’s taking place on the bottom

As predicted by most economists, the Reserve Bank of Australia (RBA) opted to preserve the cash rate at 4.35% for the sixth time in a row at its June board assembly immediately.

This determination comes amidst ongoing considerations about inflation and a blended financial outlook whereas mortgage holders proceed to do it robust.

The Board stated inflation has been easing however has been doing so extra slowly than beforehand anticipated and it stays excessive.

“The Board expects that will probably be a while but earlier than inflation is sustainably within the goal vary. While latest knowledge have been blended, they’ve strengthened the necessity to stay vigilant to upside dangers to inflation,” the Board stated.

“The path of rates of interest that can greatest be sure that inflation returns to goal in an inexpensive timeframe stays unsure and the Board isn’t ruling something in or out. The Board will rely on the information and the evolving evaluation of dangers.”

Brokers react to pause

While a high-rate surroundings continues to put stress on mortgage holders, Aussie franchise brokers Matthew Rogers and Dipal Patel have been unsurprised by the RBA’s determination.

Rogers (pictured above far left), director of Aussie – Inner West in Sydney, stated the central financial institution aren’t going to make any “hasty choices” when it comes to the cash rate.

“We have been anticipating a maintain due to the inflation and low unemployment rate knowledge. We welcome the maintain given the present hardship we’re seeing within the financial system.,” Rogers stated.

“Inflation figures this 12 months have been blended they usually’ll proceed to watch this earlier than making a transfer.”

While inflation got here in barely greater than anticipated at 3.6% for the March quarter, nonetheless exceeding the Reserve Bank’s goal vary of two% to 3%, Dipal Patel, director of Aussie – Seven Hills, stated Australia is in a “significantly better place” in contrast of the beginning of final 12 months.

“Inflation is now half of what it was a 12 months in the past and hopefully reaching the goal by finish of this quarter,” stated Patel (pictured above centre left).

While a maintain in charges offers shoppers readability on their price range, mortgage dealer Chris Mushan stated in the event that they have been falling behind already the impact of the earlier rate rises has “a snowball impact”.

In March 2024, there have been almost $14.7 billion value of residential loans behind in repayments between 30 and 89 days. Arrears of 30-89 days late elevated 15% year-on-year, whereas arrears of 90+ days late have been up 17%, in accordance to Equifax.

“It’s robust,” stated Mushan (pictured above centre proper), director of ChapterTwo. “And in the event you couple the rate rises with shoppers who already had unsecured money owed and automobile loans, it’s changing into unmanageable.”

What are brokers seeing on the bottom?

With mortgage arrears on the rise after two years of steep hikes, it is no shock that Rogers has seen a number of his clients experiencing rate anxiousness.

Rogers stated whereas charges have been on maintain for some time now, and a few are getting used to the brand new regular, “many are close to breaking level”.

“Another determination to maintain charges isn’t the worst end result but it surely’s the unknown that feeds the rate anxiousness many are feeling.”

Gerard Hansen (pictured above far proper), director of FinVu Financial Services, has discovered his shoppers have gotten higher ready.

“All of my shoppers have been bracing themselves for this determination, with a view that rate cuts will occur later within the 12 months,” Hansen stated.

Hansen stated he had spoken to a number of retail shoppers who suggested him that “spending is down, and persons are holding onto their cash”.

“One restaurant proprietor consumer suggested that he would love to improve his supreme pizza value – however who’s prepared to pay an additional $10? Clients are driving the financial tightrope,” Hansen stated

Hansen stated his shoppers had additionally talked about the July 1 authorities stimulus that’s set to enhance the financial system.

“The normal fear is that we are going to spend extra, and the RBA’s response can be to decelerate the financial system additional by rising charges,” Hansen stated.

“One factor for certain – ever in my historical past of lending have shoppers been extra knowledgeable about financial measures together with inflation and rates of interest. My pizza store proprietor ought to run a podcast.”

Patel has urged her urged her shoppers to keep in mind that simply because the cash rate holds, doesn’t imply they need to maintain.

“It’s the most important monetary asset of their lifetime, and often reviewing it’s important – identical to you do another service resembling your utilities,” stated Patel who recommends checking in each six months.

“We’re additionally seeing out-of-cycle rate modifications, notably by a number of the small lenders. Just as a result of the cash rate is standing nonetheless, mortgage holders shouldn’t be,” she stated.

“That’s what brokers are right here for. I’ve had many a dialogue with clients who have been simply not conscious of how a lot they may save. A great dealer must also all the time be checking in with their clients – particularly in occasions like these.”

The cash rate crystal ball

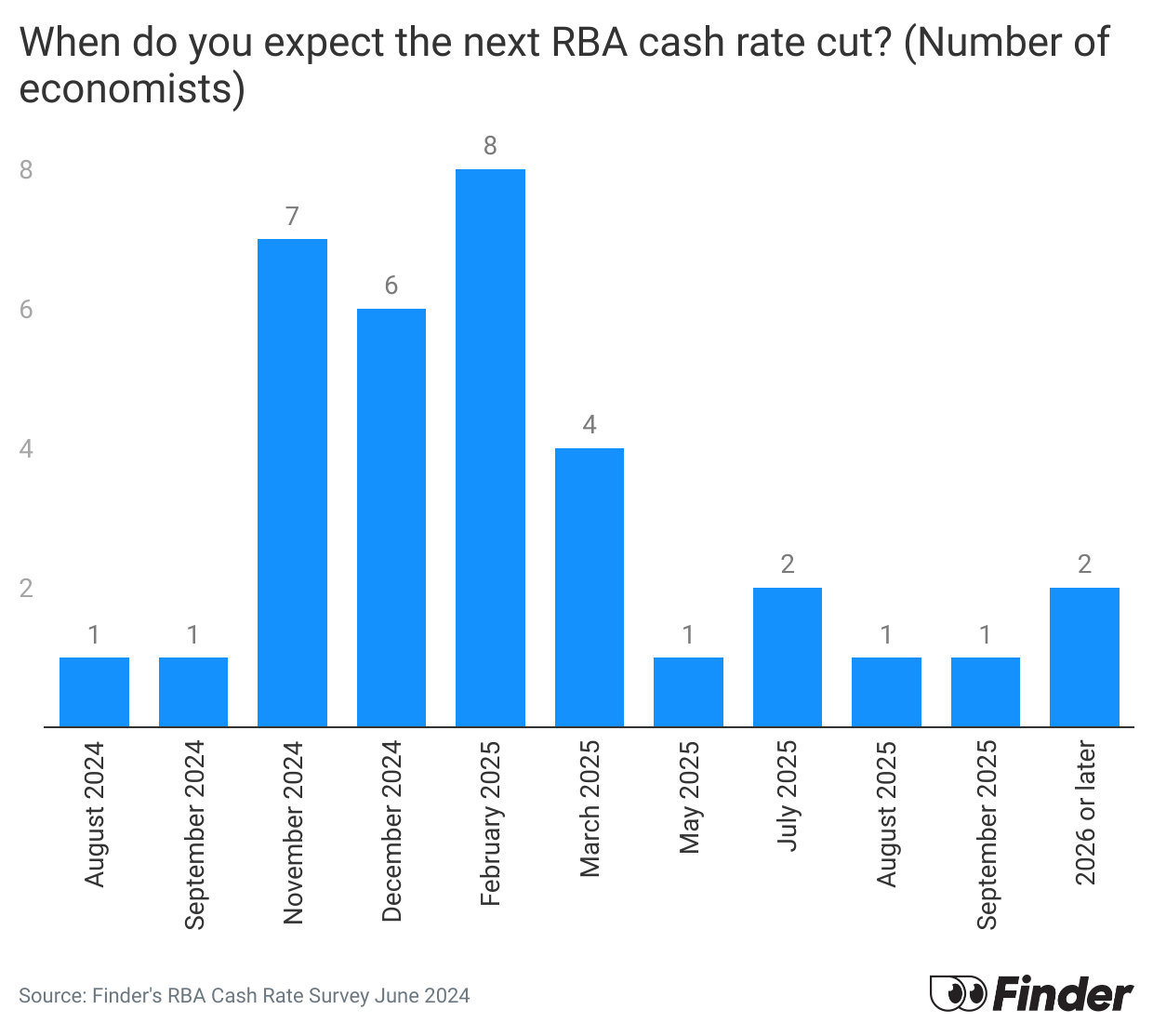

While brokers might not have a crystal ball, the final knowledge is that the long-awaited rate cuts anticipated to start in June or July have now been pushed to November and even later.

Rogers stated that 2025 has develop into extra life like.

While financial indicators are vital, a lot of the RBA’s decision-making will rely upon how the inflation knowledge will learn over the following two quarters.

One factor is for certain, in accordance to Mushan, one other rate hike would “crush lots of people”.

“Many individuals we’re speaking to are simply holding on with rate cuts beginning to be talked about within the media,” Mushan stated. “For some, its mild on the finish of tunnel they usually consider they will make it by.”

“If there was to be one other hike, I feel we’d see arrears rising and many individuals in search of help. We don’t suppose there can be one other, and we hope that there isn’t.”

What ought to advisers take note?

The brokers supplied some recommendation for his or her colleagues:

Provide balanced data: Understand the client’s wants and tailor compensation choices accordingly (fastened or variable) to meet their targets, in accordance to Rogers.

“You should guarantee it suits with their targets.”

Affordability is vital: Ensure a consumer’s general monetary state of affairs is reviewed, stated Mushan. Advisers ought to be cautious of suggesting further credit score if debtors are already struggling.

“Overall, making certain that your consumer is in a greater place than once they got here to you is vital.”

Individualised method: Every buyer’s state of affairs is exclusive, Patel identified. Brokers can supply personalised options, resembling negotiating with lenders, reviewing funds, or purchasing round for higher charges.

“Ultimately, no buyer is similar and it’s up to us to current them with choices.”

Related Stories

Keep up with the most recent information and occasions

Join our mailing listing, it’s free!