Federal Reserve Chair Jerome Powell informed the House Financial Services Committee that the central financial institution is on equal footing with different financial institution regulatory businesses in Washington.

Federal Reserve Chair Jerome Powell informed the House Financial Services Committee that the central financial institution is on equal footing with different financial institution regulatory businesses in Washington.

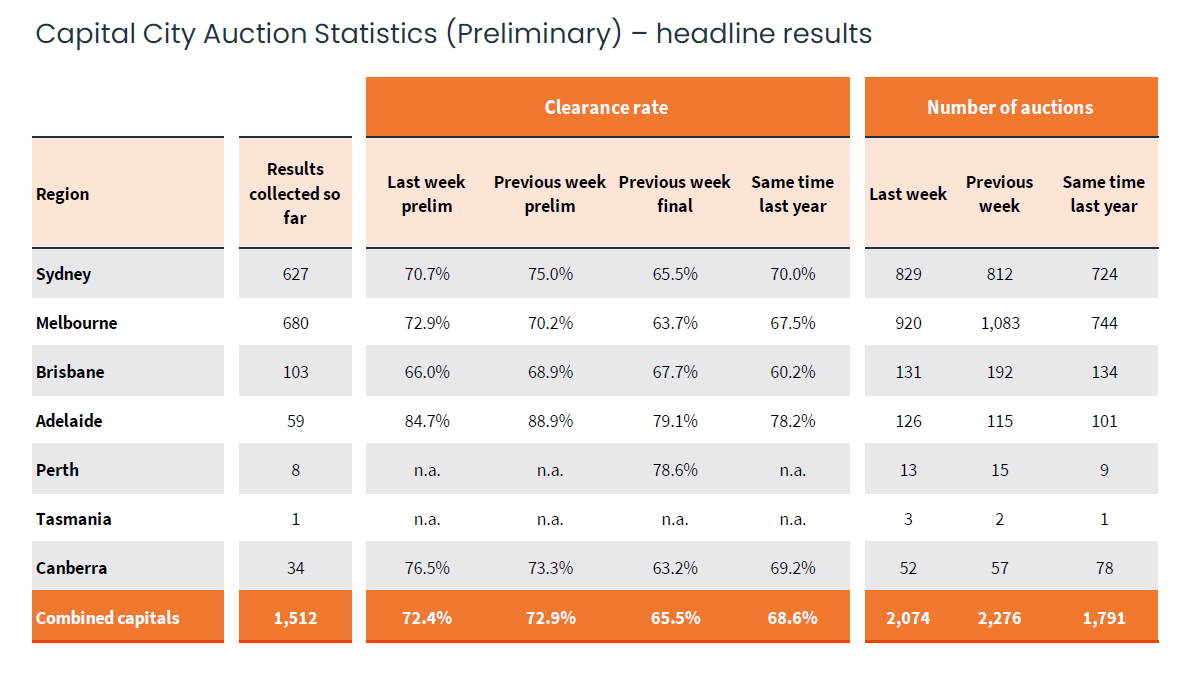

Al Drago/Bloomberg

The Federal Reserve is “able to go” ahead with a new capital proposal for banks, but it surely can not pressure different regulators to maneuver on the problem, Fed Chair Jerome Powell informed Congress on Wednesday.

In his second look on Capitol Hill this week, Powell informed the House Financial Services Committee that the Fed doesn’t have supremacy over the Federal Deposit Insurance Corp. or the Office of the Comptroller of the Currency on regulatory issues and it’ll not try to strong-arm the opposite two businesses on revisions to their joint Basel III endgame proposal.

“I might say it is strictly collaborative,” he stated. “And I might say that our discussions with the FDIC, which [Fed] Vice Chair [Michael] Barr has truly been conducting, and the OCC, they have been very productive to this point. So … we have continued to work our means via this, and I imagine we’ll get, pretty quickly, to a decision of the remaining course of situation.”

Powell’s newest remarks come in the future after he declared the Fed’s curiosity in re-proposing the so-called Basel III endgame package deal to permit the general public a chance to remark on the “broad and materials adjustments” which were made to it in latest months.

During Wednesday’s three-hour listening to, Powell declined to say what’s holding up negotiations between the Fed, FDIC and OCC over how one can proceed.

“I do not need to say that we’re at odds,” he stated. “I simply need to say we’re working via this situation collectively.”

He additionally refused to lift the curtain on adjustments the Fed has already made to the proposal, noting that “nothing is agreed till all the pieces is agreed.”

Powell did notice that not all adjustments made to the unique proposal — which was put forth final summer time and attracted all kinds of public feedback, the overwhelming majority of which have been in opposition — can be included within the re-proposal.

“We’re targeted on one huge space, however there are establishments which have made feedback all throughout the spectrum, and we’re studying all of these fastidiously. We’re not going to republish all of these,” he stated. “Some of these, we will simply make adjustments and transfer ahead on.”

Powell additionally amended a few of his statements from yesterday’s hearings. Instead of noting the “strongly held view of the board” on the matter of re-proposal, he referred to “the robust view of quite a lot of board members.” He additionally clarified that whereas the capital rule may very well be finalized as quickly as the primary quarter of subsequent yr, that was one in all a “vary” of potential timelines.

Despite his perception {that a} re-proposal is acceptable and in step with previous actions by regulators, Powell didn’t rule out the potential of shifting to finalize the rule with out searching for extra public enter. But, if that choice is on the desk, committee members let Powell know that utilizing it will draw a swift backlash.

“Broad and materials adjustments to the Basel III endgame necessitate a full re-proposal. Full cease,” stated Rep. Patrick McHenry, R-N.C., who chairs the Financial Services Committee. “Failure to take action will lead to an instantaneous Congressional Review Act vote out of this House of Representatives as rapidly as we will probably course of it.”

When pressed for his views on the present stage of capital inside the banking system, Powell informed the committee it was “about proper,” however famous that figuring out the optimum quantity of capital isn’t a precise science. He stated his most important objective in finalizing the capital reforms is to place the U.S. on even footing with different giant international locations and banking jurisdictions world wide.

Powell added the adverse public response to the preliminary Basel III endgame proposal — accounting for properly over 90% of the general suggestions, by some estimations — is one thing that ought to be addressed.

“Broad assist, empirically, would imply an excellent strong vote on the Fed board. I’ve tried to not be particular about what which means,” he stated. “But it additionally means broad assist among the many broader neighborhood of commenters on all sides.”

He additionally made clear that the Fed doesn’t intend to pursue some other regulatory reform gadgets — corresponding to new long-term debt necessities and liquidity requirements — till adjustments to the capital proposal are agreed upon and put forth to the general public.

Powell stated the Fed is committing sources to bettering the infrastructure underlying its last-resort lending facility, the low cost window, including that the present person interface is “drained.”

Another matter of repeated curiosity from legislators — each within the House Financial Services Committee on Wednesday and within the Senate Banking Committee on Tuesday — was govt compensation at banks. Specifically, lawmakers needed to know why the Fed didn’t be part of the FDIC, OCC and Federal Housing Finance Agency in proposing new restrictions on incentive-based compensation for financial institution leaders in May. The National Credit Union Administration and the Securities and Exchange Commission have pledged to take comparable steps within the close to future.

Section 956 of the Dodd-Frank Act of 2010 required the monetary regulators to develop insurance policies on compensation to make sure executives weren’t incentivized to take extreme dangers. The proven fact that the Fed has gone so lengthy with out assembly this mandate has annoyed some members of Congress for years, however the situation has taken on renewed relevance within the wake of the failure of Silicon Valley Bank and different giant regional banks final yr.

Powell, who previously has stated he want to higher perceive the problem the regulators are searching for to unravel, testified that the Fed is continuous to discover the subject. At a number of factors this week, he pointed to steering the Fed issued concerning govt compensation in 2010 and famous that the company’s examiners strictly supervise banks to make sure they adhere to those requirements. He stated the Fed’s job isn’t completed, however implied on Wednesday that it might have met its authorized obligations.

“Section [956] requires a rule or steering, by the best way,” Powell stated after an alternate with Rep. Nydia Velazquez, D-N.Y. “It doesn’t require a rule.”