Brokers reveal inside scoop on ANZ’s exclusive mortgage pilot | Australian Broker News

Investment Loans

Brokers reveal inside scoop on ANZ’s exclusive mortgage pilot

Why ANZ’s new mortgage product is not only for millionaires

Investment Loans

By

Ryan Johnson

Two brokers who trialled ANZ’s new pilot undertaking have revealed the scope of the mortgage product that’s restricted to Australia’s most profitable suburbs.

ANZ’s Low Risk LMI Waiver, which might’t be discovered on-line and is just obtainable to some brokers throughout Australia, provides lending as much as 95% with out lender’s mortgage insurance coverage (LMI) for patrons who meet the coverage’s eligibility necessities.

The coverage can be utilized on refinance or buy functions, for owner-occupied or funding properties with principal and curiosity (P&I) or curiosity solely (IO) repayments.

“This is arms down the perfect coverage I’ve ever seen – unimaginable. A 95% LVR product with no LMI is a game-changer,” mentioned Stevens.

“Typically, on the prime finish of the market you would want minimal 20% deposit plus prices to buy, however this coverage has fully modified the sport at simply 5%.”

What is the ANZ low danger LMI waiver?

Using analytics and credit score bureau info, ANZ’s Low Risk LMI Waiver was developed to determine prospects who’ve traditionally introduced as low danger primarily based on a wide range of components.

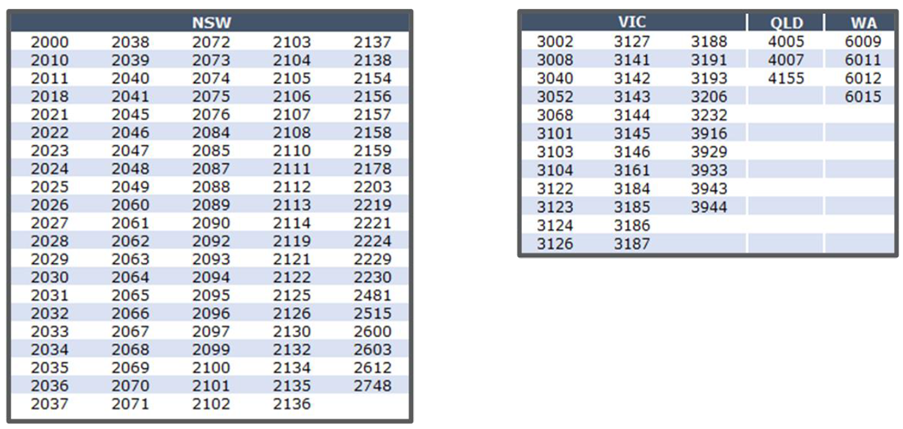

Stevens mentioned the eligible postcodes (145 places – 200 completely different suburbs) chosen have been primarily based on places which have held or elevated their worth over an extended time frame – a few of which embody Sydney’s Rose Bay, Melbourne’s Toorak and Canterbury, and City Beach in Perth.

The property provided have to be a normal residential safety – not a business property, SMSF, rural or agribusiness, twin earnings, boarding homes, NDIS, or different asset varieties – and it could’t contain functions involving guarantors, firms, or trusts.

ANZ’s excessive threshold, low deposit coverage

Sum, who’s Flint’s head of recommendation, has already put collectively $100 million price of proposals for this coverage “in the previous few weeks alone”.

There are two the explanation why Sum believes this to be “the primary coverage of its variety”.

Firstly, debtors often incur a premium on LMI when lending within the >90% LVR band. This successfully lowers the “true LVR” – the deposit you pay in whole.

“When you go above 90% LVR, mortgage insurance coverage is usually 3%-4%. So, what which means is that 95% LVR together with capitalised mortgage insurance coverage is mostly a base LVR of about 91% or 92%,” Sum mentioned.

Secondly, charges go up as properly.

“Typically, above-90% LVR loans charges are going to be within the seven-plus p.c vary,” mentioned Sum. “If a consumer have been to not use this coverage, we’d often advocate they might purchase at a base LVR at 88% the place LMI is perfect, and you’ll nonetheless get the below-90% charges.”

However, with this coverage, the true LVR is 95%. Customers can lower your expenses by not paying the upfront price of an LMI premium, permitting them to entry the market sooner.

Does this coverage assist the wealthy get richer?

A key concern with this program is the excessive minimal mortgage quantity – $2 million. This interprets to a required family earnings of at the very least $450,000 to qualify, successfully excluding a big portion of potential first-time homebuyers, notably these in decrease or middle-income brackets.

During a nationwide housing disaster, critics argue that merchandise aiming to carve out an exclusive marketplace for the wealthy exacerbate wealth inequality.

So, does the coverage favour the rich? No, based on Sum.

“Wealthy folks most likely wouldn’t want a 95% LVR mortgage – they have already got the fairness or money,” he mentioned. “Truly rich folks, even with sturdy incomes, may simply ask the financial institution of Mum and Dad for a deposit… and belief me, that occurs loads.”

“Instead, this coverage favours the formidable and aspiring, particularly these with out household help who can’t simply get an enormous reward for a deposit. It helps folks with sturdy incomes however restricted financial savings get into the market.”

The formidable and aspiring: A case examine

For instance, think about you might be in your mid-30s, your family earns a powerful earnings above $450,000, and also you want to purchase your first property on the $1.5 million mark at 88% LVR – lower than the typical home worth in Sydney.

You are aiming for a 12% deposit plus stamp obligation, which is round 5%. So, you want a 17% deposit – about $260,000.

“This is a major sum of money even for top earnings earners,” Sum mentioned.

Say you goal to save lots of this over 4 years saving $65,000 yearly. But once you return along with your deposit 4 years later, that $1.5 million property is now price $2 million. The market has outgrown your expectations.

“And that is the place this coverage helps,” mentioned Sum. “People’s earnings and financial savings might have grown over that four-year interval, however they nonetheless may not have that 17% deposit which has additionally modified over time.”

“This coverage makes up for that since you solely want that 5% deposit and 5% for stamp obligation.”

This is only one instance of how this coverage can be utilized. Here are some real-life conditions the place Flint Financial has helped debtors with this product:

Clients seeking to refinance and entry beforehand useless fairness to construct wealth via property quicker.

Individuals within the tech house not eager to liquidate shares – which means they’ll get the property they need and the upside within the share’s progress.

Foreign earnings expats wanting to buy higher INV properties with 75% much less deposit that beforehand required.

Families upsizing to bigger houses in higher places with considerably smaller deposits.

Cash-backed people eager to have a security internet of financial savings in an offset account with interest-only repayments, reasonably than utilizing every little thing for deposit.

Self-employed shoppers wanting to depart money in-company reasonably than pull it out for bigger deposits.

Limitations to the coverage

While the mortgage product has helped in a wide range of eventualities, it could have its drawbacks.

To meet the minimal mortgage quantity at 95% LVR, the acquisition worth must be at the very least $2.11 million to qualify for the $2 million-plus mortgage.

This may restrict choices for these looking for properties within the $1-2 million vary.

“I’ve had fairly a couple of chats with shoppers within the precise state of affairs – comparatively younger, on good incomes, and seeking to purchase their first house. But then they wish to purchase a property at $1.8 million,” Sum mentioned. “It results in a troublesome choice between utilizing extra deposit when shopping for at 88% LVR or utilizing much less deposit at the next worth level.”

Secondly, some debtors may miss out on being eligible due to the coverage’s excessive credit score requirements.

Young, financially profitable shoppers is perhaps serious about a “low danger” mortgage product. But regardless of sturdy earnings, their credit score rating prevents them from qualifying.

Credit scores are data-driven assessments by credit score bureaus that predict the chance of somebody defaulting on a mortgage (not repaying).

An extended credit score historical past with constant, accountable credit score use usually results in the next rating.

“Younger folks could also be doing every little thing proper financially and meet the earnings necessities however as a result of they solely have 5-10 years of credit score historical past, their rating is perhaps low,” Sum mentioned.

“Essentially, the system penalises financially accountable younger debtors who must borrow to get forward in a aggressive market.”

Mortgage product innovation

With banks dealing with a credit score crunch and internet curiosity margins slowly eroding, Australia’s main banks fiercely competed for market share final yr. This has since develop into generally known as the mortgage wars.

However, with rates of interest reaching their highest level in a very long time, the panorama has shifted. Banks are actually prioritising low-risk vanilla loans.

For banks that also wish to compete for enterprise, Sum mentioned they’ve two decisions: innovate or reduce charges.

“This product demonstrates that innovation in mortgages can nonetheless occur even when banks are being extra cautious,” Sum mentioned. “In my opinion, this product innovation is unbelievable and serves a wide range of shoppers. Kudos to ANZ.”

What do you consider ANZ’s new mortgage pilot product? Comment beneath.

Related Stories

Keep up with the most recent information and occasions

Join our mailing checklist, it’s free!