As a part of its give attention to easing value of dwelling pressures, the Australian authorities has introduced that every one 13.6 million taxpayers in Australia will obtain a tax reduce on July 1 by the already legislated stage 3 tax cuts. In addition to this, households, small companies and renters, amongst others, will profit from a vary of rebates aimed toward easing value of dwelling pressures. While it’s excellent news for Australian taxpayers, tax cuts might additionally affect borrowing energy, opening the doorways for first dwelling consumers and people trying to improve their dwelling.

A Boost from the Budget

Jim Chalmers, Treasurer, has revealed the Federal Budget 2024 contains a $300 vitality rebate for each Australian family, and a revamp of stage-three revenue tax cuts that may ship taxpayers a median of $36 a week from July.

“Just as each Australian taxpayer will get a tax reduce, each Australian family will get vitality worth reduction,” he advised parliament, noting that 1 million small companies may even profit from a $325 rebate.

The further revenue might translate into a enhance to borrowing energy, serving to extra first dwelling consumers get into the market sooner, and making mortgage repayments extra manageable.

2024 Federal Budget

Taxpayers

All taxpayers in Australia will obtain a tax reduce on July 1 by the already legislated stage 3 cuts.

Households

Every family in Australia will obtain $300 off their vitality invoice by a rebate.

Small companies

Around a million small companies will obtain $325 off their energy payments. The $20,000 immediate asset write-off scheme has additionally been prolonged, whereas 457 “nuisance tariffs” shall be abolished.

Renters

Commonwealth Rent Assistance shall be elevated by a additional 10 per cent, on high of a 15 per cent enhance final 12 months, benefiting practically 1 million households.

People on JobSeeker with restricted work capability

JobSeeker recipients in a position to work as much as 14 hours a week are actually eligible for the upper charge, a rise of $54.90 a fortnight. The change is predicted to profit 4700 individuals.

People who use medicines listed on the PBS

The most co-payment for prescriptions on the Pharmaceutical Benefits Scheme shall be frozen for a 12 months at $31.60.

For these on the aged care pension and concession card holders, that most co-payment shall be frozen for 5 years at $7.70 per prescription.

Pensioners

In addition to the five-year freeze for PBS medicines for individuals on the aged care pension, pensioners will profit from the deeming charge being frozen for an additional 12 months. By extending the freeze till the top of June subsequent 12 months, the federal government says 870,000 individuals, together with 450,000 age pensioners, shall be higher off.

Students

A change to pupil debt reindexation which has been backdated to final 12 months and can wipe about $3 billion off the nation’s collective HECS-HELP debt.

There’s additionally Commonwealth Prac Payment – as much as $319.50 per week for college kids throughout their scientific {and professional} placements in an try and fight “placement poverty” that may begin in mid-2025.

Parents

The authorities is spending $1.1 billion to pay superannuation on government-funded paid parental go away for fogeys of infants born or adopted on or after July 1, 2025.

Understanding Borrowing Power

Borrowing energy refers back to the quantity a lender is prepared to lend primarily based on components resembling measurement of deposit, family bills, and after-tax revenue. While tax cuts can present a great addition to revenue and doubtlessly enhance how a lot you possibly can borrow, there are another proactive steps you may take to enhance borrowing energy, together with:

Cut again on spending: Trimming down non-essential spending can release further funds to spice up your deposit which is able to enhance borrowing capability.

Reduce bank card limits: Lowering your bank card restrict – or cancelling bank cards you don’t use – can enhance borrowing energy, as a result of lenders assess the utmost credit score restrict relatively than the excellent steadiness.

Increase revenue: Finding methods to complement your revenue, resembling taking up a second job or negotiating a pay rise, can enhance borrowing energy.

Expert Advice From a Mortgage Broker

While on-line calculators – resembling this one – can present an estimate of your borrowing energy, getting tailor-made recommendation primarily based in your particular person circumstances is invaluable. Consult with a Mortgage Express dealer to get personalised recommendation primarily based in your monetary state of affairs. Work intently with an knowledgeable, resembling these at Mortgage Express, and get insights into your borrowing energy with a strategic plan that can assist you attain your private home possession targets.

While all care has been taken within the preparation of this publication, no guarantee is given as to the accuracy of the knowledge and no duty is taken by Finservice Pty Ltd (Mortgage Express) for any errors or omissions. This publication doesn’t represent personalised monetary recommendation. It is probably not related to particular person circumstances. Nothing on this publication is, or must be taken as, a proposal, invitation, or advice to purchase, promote, or retain any funding in or make any deposit with any individual. You ought to search skilled recommendation earlier than taking any motion in relation to the issues dealt inside this publication. A Disclosure Statement is on the market on request and freed from cost.

Finservice Pty Ltd (Mortgage Express) is authorised as a company credit score consultant (Corporate Credit Representative Number 397386) to have interaction in credit score actions on behalf of BLSSA Pty Ltd (Australian Credit Licence quantity 391237) ACN 123 600 000 | Full member of MFAA | Member of Australian Financial Complaints Authority (AFCA) | Member of Choice Aggregation Services.

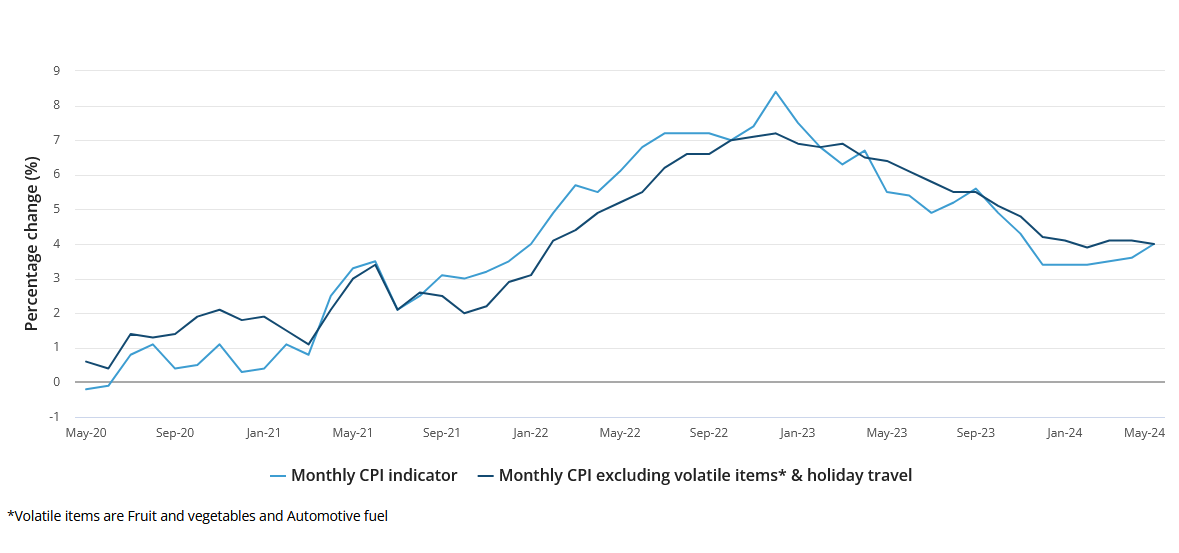

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator

Resource: Stomach muscular tissues May presumably 2024 CPI Indicator