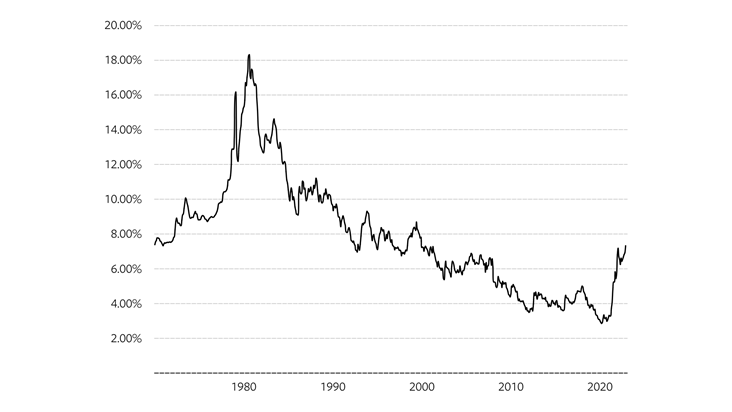

The newest weekly survey knowledge from Freddie Mac exhibits the 30-12 months fastened-fee property finance loan jumped 40 basis elements to an regular of 6.70% this week, the optimum stage due to the reality 2007.

The survey additionally implies a big dispersion in charges, indicating that homebuyers can protect lots of of kilos by searching close to with distinctive loan firms.

A calendar yr in the past right now, prices averaged 3.01%. “The uncertainty and volatility in financial markets is vastly impacting mortgage loan prices,” mentioned Sam Khater, Freddie Mac’s predominant economist. The index compiles solely purchase home loan prices described by loan suppliers throughout the earlier 3 days.

Inflation rose greater than envisioned in August as rising shelter and meals objects prices offset a fall in fuel value ranges. As a outcome, the Federal Reserve elevated the federal assets stage by 75 basis elements at its Federal Open up Industry Committee (FOMC) assembly in September.

An further 125 basis elements in hikes are nonetheless to arrive in 2022, with a federal money charge topping out correctly larger than 4%.

Treasury yields current higher charges in the fast expression, signaling a recession on the horizon. The 2-12 months observe, most intently tied to the Fed’s curiosity quantity strikes, improved 5 bps to 4.07% on Wednesday from the prior 7 days. The 10-year observe went from 3.51% to 3.72% in the actual time interval.

Effective natural language processing applied sciences extract deeper this implies from unstructured information to make a change in the lifetime of loads of would-be homebuyers who’re credit score rating invisible or haven’t had the means to get entry to economical housing finance.

On HousingWire’s Mortgage Fees Center, Black Knight’s Exceptional Blue OBMMI pricing engine calculated the 30-calendar yr conforming property finance loan charge at 6.643% on Wednesday, up from 6.124% the earlier week. Meanwhile, the 30-12 months fastened-amount jumbo was at 6.294% Wednesday, up from 5.821% the 7 days prior.

An LO in the Miami, Florida area defined to HousingWire that on a $400,000 dwelling receive, with 5% down, a 700 FICO ranking, his purchasers have gotten quoted 7% for typical loans and 6.125% on FHA and VA home loans.

“This might be a time of modifications,” he defined. “Many LOs will go away the market (specifically the varieties that solely do refis and solely promote fascination prices), others will switch most definitely from retail to wholesale. Loan suppliers will close and another people would require to merge merely due to the new liquidity guidelines which can be coming in 2023.”

Tension on demand from clients

Strain on charges has sharply lessened demand from clients for mortgage loans, in accordance to the Mortgage Bankers Association (MBA).

The market place composite index, a measure of property finance loan loan software amount, declined 3.7% for the week ending Sep. 23. The refinance index had a 11% drop from the prior week, and the spend money on index was marginally down .4%.

According to Freddie Mac, the 15-calendar yr fastened-price order home loan averaged 6.52%, up from final week’s 6.25%. Jumbo property finance loan loans (larger than $647,200) amplified to 6.01% from 5.79% in the similar time interval.

“Our research signifies that the assortment of weekly fee quotations for the 30-year preset-fee home loan has much more than doubled around the earlier calendar yr,” Khater claimed. “This implies that for the typical mortgage loan amount, a borrower who locked-in at the elevated finish of the vary would pay out quite a few hundred kilos greater than a borrower who locked-in at the cut back conclusion of the assortment.”

To encourage debtors to select out a home loan financial institution loan, some financial institution loan officers and creditors are highlighting how dwelling prices are additional very inexpensive now than final calendar yr – and the capability of a borrower to refinance the loan when charges lower but once more.

“There is additional inventory relative to demand from clients, and specials can be uncovered. It is transitioning to a buyers’ market, as 20% of sellers skilled a price ticket discount in August 2022, as opposed with 11% a yr again,” defined Loaded Weidel, CEO at Princeton Mortgage loan. “It’s now doable to purchase a family for $400,000 that may have purchased for $500,000 in 2021.”

According to Weidel, if a potential borrower acquired that dwelling in 2021 for $500,000 and place 20% down, the principal and curiosity, with prices at 3%, could be $1,686. Today, if the home could possibly be acquired at $400,000 and the curiosity stage was 7%, the cost could be $2,129.

The homebuyer can pay out way more $5,316 per yr due to to the variation in charges, however would provide help to save $100,000 buying the home these days as opposed to remaining yr.

“Eventually, charges will seem again once more down, and you can refinance the charge,” Weidell talked about. “If charges proceed to be at 7%, it might get 18 years for the higher cost of $5,316 per 12 months to chew up the $100,000 you saved searching for the home.”

However, dwelling prices aren’t slipping so radically in most marketplaces. Not nonetheless anyway.

“Some potential buyers are supplying very low ball options in the hope of getting their presents acknowledged,” one explicit mortgage loan dealer/operator in Southern California suggested HousingWire. “Still the vendor’s dedication is the important issue for regardless of whether or not to drop the price or not. The different difficulty is that many Realtors are nonetheless dreaming about proudly owning clients fight greater than the attributes and use that as a spot of sale – however irrespective of whether or not they succeed or not, that’s yet one more query.”

The Purchaser Monetary Safety Bureau introduced Wednesday that it was eradicating its Office setting of Supervision, Enforcement and Honest Lending, splitting that workplace’s duties amongst present places of work.

The Purchaser Monetary Safety Bureau introduced Wednesday that it was eradicating its Office setting of Supervision, Enforcement and Honest Lending, splitting that workplace’s duties amongst present places of work.