What appeals to females to property finance loan broking? | Australian Broker News

Information

What attracts girls to home finance loan broking?

And what are the obstacles that cease way more from becoming a member of?

The home loan broking area, like so much of others, faces a problem in attracting and retaining a quite a few workforce.

Even although initiatives have been underway to deal with this, the present MFAA Variety, Equity, and Inclusion (DEI) Survey highlights the continued require to bridge the hole, particularly when it comes to feminine illustration.

“The rationale we focused on females initially is as a result of we’re shedding gals,” outlined prosper4gals founder Jane Counsel (pictured increased than), talking on the MFAA DEI Summit on May nicely 7 in Sydney.

“Women are 50% of our inhabitants but when we simply can not retain females on this enterprise, what hope do we’ve got for broader variety?”

The proportion of female brokers did enhance for the primary time in 18 months, in accordance to the most recent MFAA data unveiled in Oct, up 1.5 share particulars to 26.9% when put next to the sooner six months and 1.4 share factors as compared to the earlier yr.

Even so, Counsel identified this was nicely beneath the decide (31%) positioned when the exploration commenced in 2017.

“We are however shedding gals regardless of some terrific improvement we’ve got designed on this initiative,” acknowledged Counsel.

Counsel emphasised the worth of data equally the points of interest and “usually invisible boundaries” females take care of within the business.

What appeals to gals to broking?

Comprehending what attracts girls to home loan broking is important simply earlier than tackling the obstacles that preserve them from holding.

The MFAA DEI research found fairly a couple of components that enchantment to women of all ages, corresponding to:

Flexible doing the job: This will enable females to stability occupation with personal commitments.

Entrepreneurial alternatives: Lots of broking roles comprise jogging their have firms, fostering independence.

The nature of the operate: Assisting purchasers understand cash objectives will be personally satisfying.

Money prospects: Home finance loan broking offers stable incomes possible.

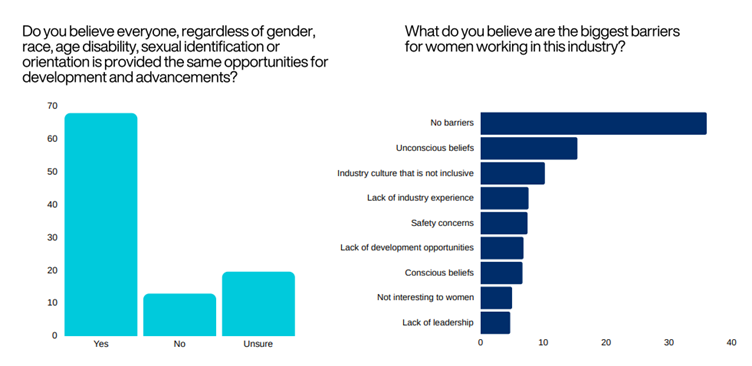

A sizeable half answered females confronted no boundaries at all.

“If I’m not dealing with discrimination and enduring these boundaries, is it really occurring if it’s not happening to me? Which is the sort of barrier we’re working with,” Counsel talked about.

“Fortunately, we’ve got 6 years of analysis and there may be been some common themes.”

Perception gaps and unconscious bias

The exploration found a significant disconnect in how grownup males and girls perceive the business. In the start, quite a few male brokers didn’t acknowledge the underrepresentation of women of all ages or the existence of boundaries.

In 2018, 22% of male MFAA customers thought-about that women had been being underrepresented, which enhanced to nearly 35% in 2022 and was a carry of 10% from the 2021 evaluation. Female ‘sure’ responses to this query have additionally elevated to 75% up from 56% in 2021.

“There’s been a massive change up to now six a number of years,” Counsel stated. “People are questioning their beliefs concerning the actuality of working on this market.”

Unconscious bias, the place by stereotypical beliefs affect behaviour, was acknowledged as one more hurdle.

“There is an unconscious perspective of what the standard dealer appears like,” Counsel mentioned. “We want to have to be aware of that and drawback people assumptions.”

Setting up a way more inclusive tradition

The third largest barrier for females on this enterprise was a non-inclusive custom, in accordance to the research.

“Culture is something. If we would like to alter {the marketplace}, we’ve got to start on the society,” Counsel talked about. “One of essentially the most vital objects we goal on on this market is volumes and cash outcomes earlier talked about the whole lot else.

“I get it. We are within the area that’s all about monetary viability, however is {that a} picture of custom that’s inclusive?”

The exploration additionally noticed that lady brokers are way more most certainly to winner selection and inclusion initiatives. This highlights the relevance of fostering an environment wherein all voices are listened to and valued.

“If we’re heading to shift the approach to life, variety and inclusion should be a precedence for anybody,” Counsel reported.

By addressing these troubles and making upon the nice explanation why lady brokers keep and are attracted to the enterprise within the very first location, the MFAA hopes to foster a extra welcoming and various pure setting, benefiting equally companies and clientele.

Related Tales

Keep up with the most recent data and conditions

Be a component of our mailing record, it’s free!