The mortgage charge pendulum swings but but once more

By Didier Malagies

•

18 Apr, 2024

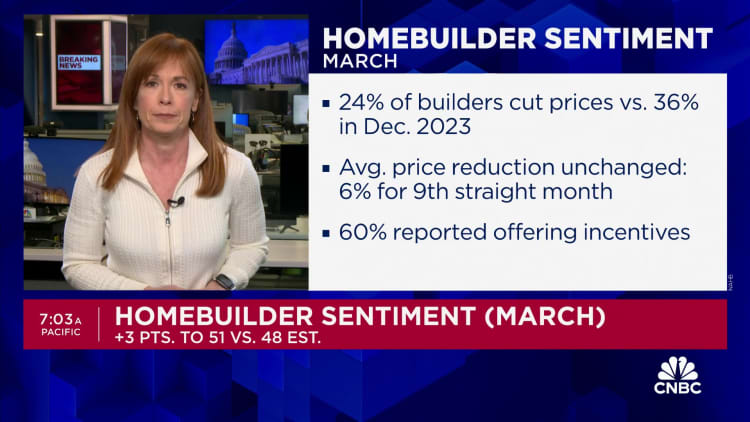

Hope 2024 to be mildly a lot better than 2023 with home mortgage prices falling within the subsequent half of the 12 months, housing business consultants opined in their forecasts on the end of the calendar 12 months. Cuts to the Federal cash cost (and subsequently to house mortgage premiums) are imminent, merchants enthused quickly after December’s convention of the Federal Open Sector Committee during which committee associates predicted a number of degree cuts in 2024. Some authorities forecasted as many as 6 quantity cuts within the 12 months centered on this info. Price cuts are even now coming, simply not in March , merchants and market place gurus reasoned way more these days because the monetary state continued to function scorching. And now on the heels of experiences of a lot better than predicted positions progress and stickier than anticipated inflation , the market’s shift from optimism to pessimism above cost cuts is total. Some even expect value hikes simply earlier than charge cuts. The pessimism is clear in property finance mortgage costs. Freddie Mac‘s weekly Major Mortgage mortgage Market Survey is climbing once more towards 7%. HousingWire’s House mortgage Price Centre , which depends on info from Polly, is presently beforehand talked about 7.2%. Rates had been as minimal as 6.91% for Polly and 6.64% for Freddie as not too way back as February. On Tuesday, they arrived at 7.50% on Mortgage News Daily, a superior for this 12 months. Mortgage expenses preserve principal electrical energy within the housing area most significantly, greater prices exacerbate the present affordability disaster by walloping the getting vitality of would-be prospects and discouraging some would-be sellers – these individuals with low, fastened-charge mortgages – from itemizing their properties, a drain on on the market inventories. All this leaves housing gurus the second as soon as once more preventing for his or her share of shrinking pies – as we’ve got noticed with a short time in the past launched house finance mortgage data and RealTrends Verified’s brokerage knowledge , in addition to additional dives on the brokerage landscapes in Jacksonville and San Diego . It is unsurprising, then, that true property shares have suffered contemplating the truth that the FOMC’s March convention and the fashionable profession and inflation experiences. That consists of the nation’s high rated homebuilders (DR Horton and Lennar), home mortgage originators (United Wholesale Mortgage and Rocket Mortgage), brokerages (Anyplace and Compass) and residential lookup portals (Zillow and CoStar, which owns Residences.com). There are different dynamics at have interaction in for a few of these organizations, nevertheless. The brokerages are additionally contending with the rule variations included in a proposed settlement by the National Affiliation of Realtors some consumers additionally assume all these rule enhancements edge CoStar on the expenditure of Zillow . UWM, in the meantime, is contending with a scathing investigative report by a hedge-fund-affiliated info group whose hedge fund shorted UWM and went prolonged on Rocket it’s also working with pending litigation . UWM denies the allegations produced within the report. Higher house finance mortgage charges, a lot much less house mortgage applications and far much less house gross sales are sadly not the one outcomes housing gurus may see from a further extended superior-charge ecosystem. There are additionally spillover outcomes from different industries, particularly workplace severe property. Regional banks – which usually have been main family house mortgage originators – went giant on business true property loans as bigger banking establishments scaled again once more on this house in present a number of years. That enhanced their publicity to downtown enterprise towers, which have seen an exodus of tenants and a bottoming out of appraised values simply as a doc $2.2 trillion in enterprise real property debt arrives due in regards to the future variety of yrs. That ties up capital that might in every other case stream to family house loans and in some situations stresses banks like New York Group Lender, mum or dad of Flagstar Lender — the seventh-largest financial institution originator of family mortgages, fifth-most vital sub-servicer of property finance mortgage monetary loans and the 2nd-largest home mortgage warehouse monetary establishment within the state. Homebuilders, as effectively, expertise the consequences of extended giant premiums. Although homebuilder assurance is proceed to up considerably contemplating that closing fall, new housing begins are slowing . The dim potential purchasers for homebuyers have turned some traders to the nascent make-to-rent sector , principally a wager that superior charges are proper right here to maintain for prolonged sufficient that will-be prospects at the moment are would-be renters.

.png)