Are you excited about the age-old dilemma of whether or not or to not hire or get hold of a house this yr? Enable Evergreen Household Financial loans current you with an important perception to allow tutorial your conclusion with readability and self-worth.

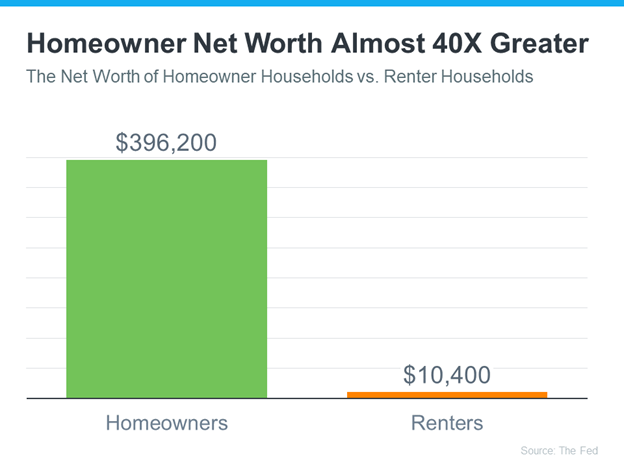

Every just a few many years, the Federal Reserve’s Study of Shopper Funds (SCF) reveals eye-opening variations in web worthy of in between property house owners and renters. The most up-to-date report means that the odd home-owner’s web price is sort of 40 cases larger than that of a renter. This substantial wealth gap is essentially due to to the equity householders make as their property appreciates and by the use of constant mortgage funds.

The Electrical energy of House Equity in Wealth Creating

Household equity is a substantial prosperity builder for quite a few properties, typically surpassing different belongings in contributing to a person’s internet price. This craze spans throughout varied earnings ranges. Homeownership is not only about buying a spot to dwell it’s a sturdy monetary tactic that fosters stability and prosperity preservation throughout generations.

At Evergreen Home Financial loans, we understand that the journey to homeownership is a essential step in prosperity developing. Our floor breaking mortgage gadgets are designed to make this path obtainable and worthwhile, particularly for very first-time purchasers.

Evergreen’s Modern Alternatives to Homeownership

We present tailored dwelling mortgage strategies to in form varied fiscal circumstances, supporting much more folks immediately changeover from leasing to proudly proudly owning.

Our CashUp Suite of Solutions are developed to provide purchasers a aggressive edge within the housing business, boosting their acquiring capacity.

For these folks searching to make their aspiration family, our Construction Loans provide the pliability and steerage essential to remodel visions into reality.

Navigating the Recent Real Estate Market with Evergreen

With fluctuating dwelling finance mortgage charges and a shifting stock panorama, navigating the intense property present market might be difficult. This is the place by Evergreen Residence Financial loans measures in. Our crew of devoted dwelling mortgage advisors will guidebook you by the possibilities available in trendy market, guaranteeing you uncover one of the best dwelling to get began making your wealth.

Conclusion: The Evergreen Advantage

Proudly proudly owning a family is greater than only a way of life choice it’s a important to unlocking your fiscal foreseeable future. With Evergreen Household Loans, embark on this journey with confidence. Our progressive items and customised assist are beneath to help you enhance your prosperity on account of homeownership, no matter your income quantity.

To perceive extra about how we might help in transforming your homeownership wishes right into a wealth-constructing actuality, be part of along with your neighborhood Evergreen Lender.

Resource: Holding Existing Matters

The home mortgage market is switching just because want premiums have enhanced far too speedy and a number of other organizations usually are not incomes enough income because of 1 dimension matches all pricing. All property finance mortgage firms

The home mortgage market is switching just because want premiums have enhanced far too speedy and a number of other organizations usually are not incomes enough income because of 1 dimension matches all pricing. All property finance mortgage firms

.png)