Aussie mortgage holders struggling | Australian Broker News

News

Aussie mortgage holders struggling

One in 5 go interest-only

More than half 1,000,000 Australian mortgage holders have switched to interest-only funds to keep away from delinquency, based on new analysis by Finder.

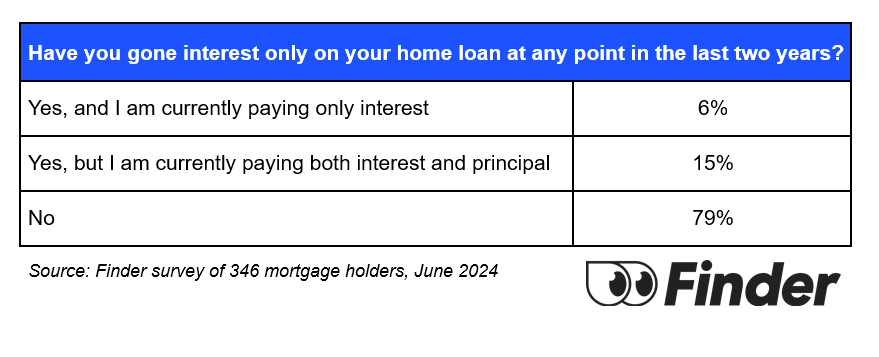

A survey of 1,062 respondents, together with 346 mortgage holders, discovered that 21% have gone interest-only over the previous two years. This change equates to 693,000 folks paying the naked minimal on their loans.

Preventing delinquency

The analysis indicated that 6% of debtors, or 198,000 folks, are presently on interest-only loans to keep away from falling behind on repayments.

“Millions of Aussie households are in survival mode. Such a big portion of individuals’s earnings are allotted to their mortgage and spare money has been extinguished,” stated Richard Whitten (pictured above), Finder’s house loans knowledgeable.

Rising defaults

Mortgage defaults have been rising.

Finder’s evaluation of APRA information confirmed $14.6 billion value of house loans have been 30-89 days overdue in March, up 65% from $8.8bn in December 2022.

Overdue mortgages now account for 0.9% of all excellent house mortgage debt, up from 0.62% in December 2022.

“Banks have a accountability to assist prospects experiencing monetary stress, so put disgrace apart and communicate up if you’re in that place,” he stated.

Competitive charges and financial savings

Whitten recommends debtors guarantee they’ve a aggressive rate of interest.

“You needs to be in search of an rate of interest beginning with a ‘5’ or a low ‘6’ – in any other case you’re paying an excessive amount of,” he stated.

Whitten additionally urged conducting a mortgage audit firstly of the monetary yr to seek out higher offers

Managing interest-only loans

To handle interest-only loans, Whitten suggested:

Know when the interval ends: Check along with your lender and put together for elevated repayments.

Build a financial savings buffer: Save additional money to satisfy increased repayments when the interval ends.

Review spending: Monitor month-to-month revenue and bills to remain on monitor with repayments and establish areas to chop again.

Get the most popular and freshest mortgage information delivered proper into your inbox. Subscribe now to our FREE day by day e-newsletter.

Related Stories

Keep up with the most recent information and occasions

Join our mailing listing, it’s free!